My two cents on the current situation of this once multi-bagger:

Revenue hit an upper cap of 1000-1100 Cr in 2015 and the company has struggled to breach that mark in the last 8 years. Noticeably, 2015 was also the year when the tide turned for the stock price. There are sectors where companies grow to a limit and hit a ceiling revenue because of externalities and fragmented market structure. This seems to be one such sector.

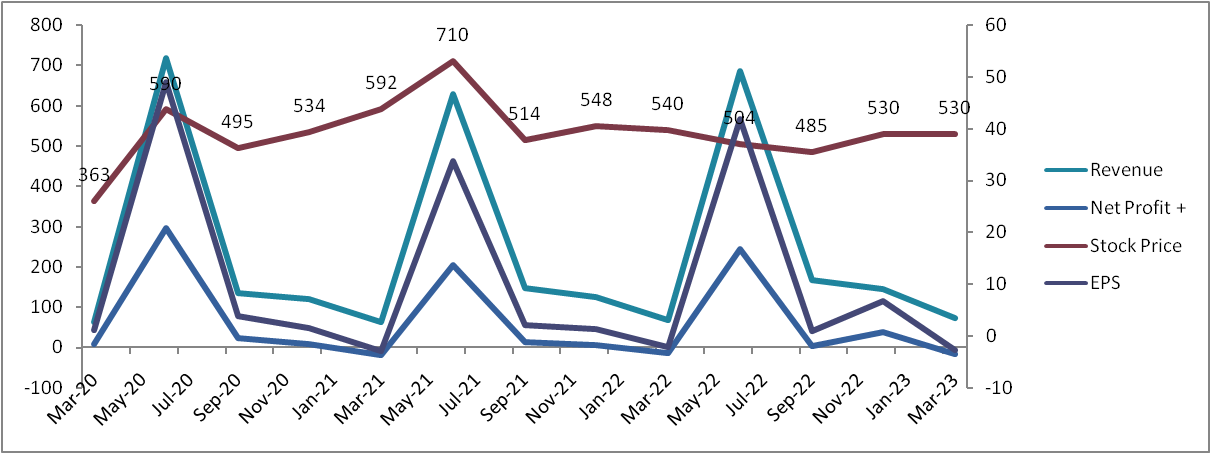

Cyclicity: Cotton seeds are still the largest contributing segment and due to its cyclicity of demand, there is cyclicity in Revenue, Profitability, EPS and hence in the stock price. This has been mentioned in this thread earlier by @Shresth_Toshniwal . Below chart shows Qtrly Revenue, Net Profit, EPS & Stock Price since March-20. This can be charted for earlier periods as well.

The company is changing its segment revenue mix to focus more on non-cotton segment (Rice & Vegetable seeds), yet there are too many externalities which it cannot control, viz: monsoon variation, govt. policies, illegal BT-Cotton in market, etc.

Disc: Not invested.

| Subscribe To Our Free Newsletter |