Investment Thesis on Aavas Financier – July 14, 2023

AAVAS Financier

July 14, 2023

Company background

Aavas Financier is an affordable housing finance company (avg ticket size >10 Lakhs) with an impeccable record – 5-year CAGR of 27.22%… Reasons for growth have been steady expansion, deep understanding of borrowers (state-specific) and heavy investment in tech for all functions (evaluating credit worthiness, customer exp, collections etc). Technology investments enabled to bring down loans processing time (Turn Around Time) at a record 10 days, with a target of 3-4 days once technology changes are fully implemented (2024) while maintaining asset quality by containing gross NPAs at sub 1% throughout its life.

Investor presentation Q4 FY23

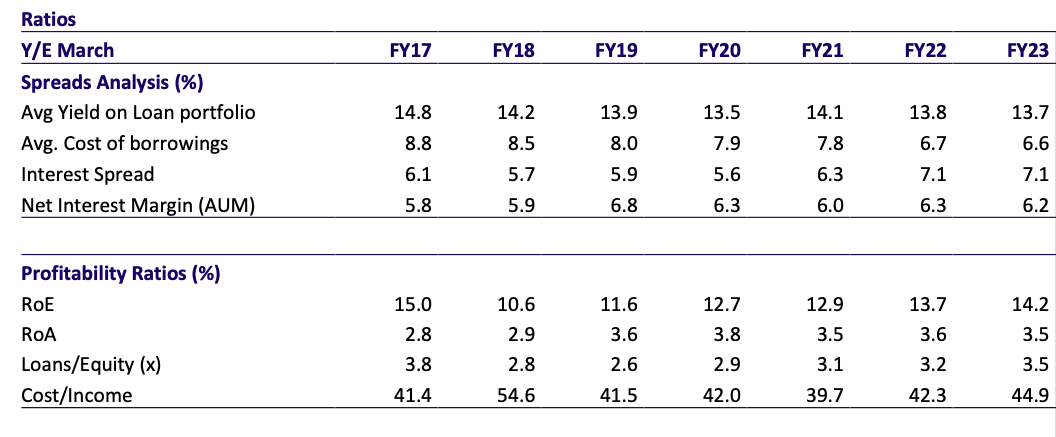

Moat: Ability to raise capital from diverse and cheap sources that are difficult to crack for competitors ( eg. world bank, long term bonds) so Cost of capital is 7.61% while making loans at 13.12% interest (passing on reduced cost of capital unlike peers). Most competitors raise funds at higher prices (eg using expensive short term NCDs or CPs)

Investor presentation Q4 FY23

Business model

Aavas started with home state Rajasthan lending to small salaried(40%) and self-employed (60%) people like govt. Employees, cab drivers, kirana store owner etc in T2, T3, T4 cities. It maintains its product mix of 70% housing loans and non-housing loans at 30% with a strong in-sourcing loans (no DSA) and strong legal, underwriting team. It expands prudently by launching in a state, deepening presence and then moving onto new one.

Since opex costs are high in T3-T5 cities and there are few customers meeting creditworthiness of banks, once penetrated competition in geographies is reduced from banks and other housing finance companies.

Size of opportunity

Access to credit is still extremely but from 2004 to now, percentage of house mortgages has only grown from 4-5% to 10-12% of GDP, while the same is 60-70% in developed markets

“Deepak Parekh : Mortgage-to-GDP ratio in India is 11%, compared to 18% in China and 52% in the United States”

Drivers of growth of affordable housing sector

- Long term:

- Rising urbanisation and people coming out of poverty

- Increased access to credit on back of UPI, Jan Dhan accounts and Aadhar

- Short Term

- Election Year

- Interest rate normalisation

Investment Thesis

Due to bluechip quality execution, Aavas has commanded a median PE of almost 60 since November 2018 when it was listed. Current PE is under 30 due to 2 reasons

- Resignation of Founder CEO – Mr Sushil Agarwal

- Promoters may trim stake

However, it was planned and new CEO Sachin Bhinder was working closely with outgoing CEO for 3 months and has been with Aavas for 3 years.

Moreover, in the May ‘2023 concall- “no major attrition is expected, despite the founder’s resignation. 71% of employees have been with the company for 3+ years. MD&CEO also clarified that promoters have not sold shares in last 2 years and do not intend sell any stake in the near term too.”

I believe this is a great opportunity to buy a growing company at relatively cheaper valuations given the growth rate.

Moreover, investments in tech will compound over time increasing the speed and size of loan book (following growth of Bajaj Finance).

Shareholding pattern (Investor presentation – Q4 FY23)

Recent Block deals

Anti-thesis

- Profitability and size (scale challenges): It has a loan book size of 1.4L cr, growing at 25% CAGR is going to get more and more difficult.

- RoA has been high using low Debt to Equity ratio (3-4) which reduces cost of borrowing, pushing up profitability. Therefore maintaining a high Price to Book multiple would be difficult.

- Borrowing cost is expected to rise in the next 2 quarters due to older contracts coming up for repricing and rate hikes globally.

- Repeat business is rare due to few products (MSME loans will be started soon) and people introduced to capital may turn to banks after building credit history (business transfer risk).

Story in Charts

Investor presentation Q4 FY23

25 May 2023 Motilal Oswal Report

Points of interest

-

It added 25 branches in Q4FY23 taking the total branch network to 346 as of Mar’23

-

Write-off is just Rs0.25bn in 2021-23’s disbursement of Rs220bn.

-

RoA 3.51%

-

High Profitability (ROA) must be taken considering low leverage (Debt to Equity)

-

ECL Provision 0.71% of AUM

Guidance:

May 2023 Concall guidance

- Company is guiding for a growth rate of 20%-25%, with deeper growth in existing geographies and moderated growth in new territories.

- Home loan and non-home loan mix is not different than in Q4 of last year, with a focus on MSME and LAP portfolio.

- Margins have come down slightly due to increased cost of borrowing and time required to pass on increased rates to new assets, but company is confident in maintaining 5%+ spread.

- The company plans to remain between 30-35% non-home loans and 70% home loans.

- 90% of branches break-even in the first 12 months

- Continue to open 30-35 branches every year and will add 2 more states in the next

2 years - Planning to cover entire country in the next 15-20 years

ICICI report Highlights

MARGINS

- Increased prime lending rate by 160bps during FY23 and further increase of

40bps with effect from Apr 05, 2023.

o This led to increase in tenure for roughly 90% of AUM.

o In case of a customer having rate of 12%, rate hike led to increase of

Rs500-1000 EMI per month.

o Average EMI per month is Rs12,000. For non-HL, the incremental lending

rate is 13-15%, and HL is 10.5% to 12%.

-

NHB borrowing was Rs30bn out of which Rs20bn are fixed rated and have a 7

years’ tenure with a borrowing rate of <5%. For bank borrowing, MCLR rate is reset every 6 months. One reset has already happened; it might come again for reset after 6 months. So there will be some impact on borrowing cost in next two quarters. -

Marginal decrease in spread during Q4FY23 due to funding cost increase and lag for rate pass. Overall basis, the company remains confident about maintaining spread of >5%. In competition terms, the company is not seeing much competition in geographies it is operating as home loan penetration is not more than 2-3%.

-

On the asset side, >50% of the assets gets repriced immediately because of floating nature. For fixed rated assets, rates get repriced after 3 years. However, there is perfect match with how it moves on the liability side as well. Interest rate hikes take time on the new business. PLR gets repriced immediately for floating contracts.

GROWTH

- Its model is to first enter the market, learning about the market and then grow in that market.

- New geographies just entered are Karnataka and UP. Every 2-3 years, company identifies new geographies to grow.

- In new states, strategy continues to be targeting Tier 3 and below cities with focus on self-construction product.

- In rural areas, branches are low opex model. Rs20-25k rent, 4-5 employees. Within 6 months, 90% of branches have break-even. Today most 1-year-old branches are giving RoE of >12% and 3 years old branches are giving >20% RoE.

Reports for further reading:

Investor Presentation May 3, 2023

Questions

- Why such a large decentralised underwriting team in spite of tech investments?

- What is the growth at state-level?

| Subscribe To Our Free Newsletter |