Pardon for redundancies when compared to Dada’s note at the start of this thread:

IPO-OFS, 9.57+ Cr. shares | Main Promoter, Tata Motors Ltd offering 8.1 cr. shares for sale | Total Equity Shares – 40.57 Cr. with FV INR 2 | I think that the Promoter’s shareholding % will reduce to 56.7% from 76.4% after IPO.

Primary Business:

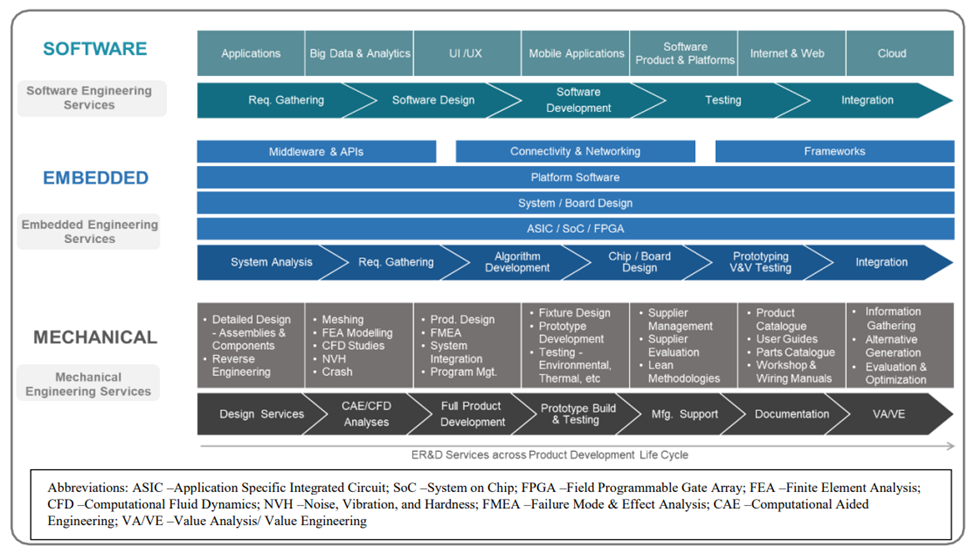

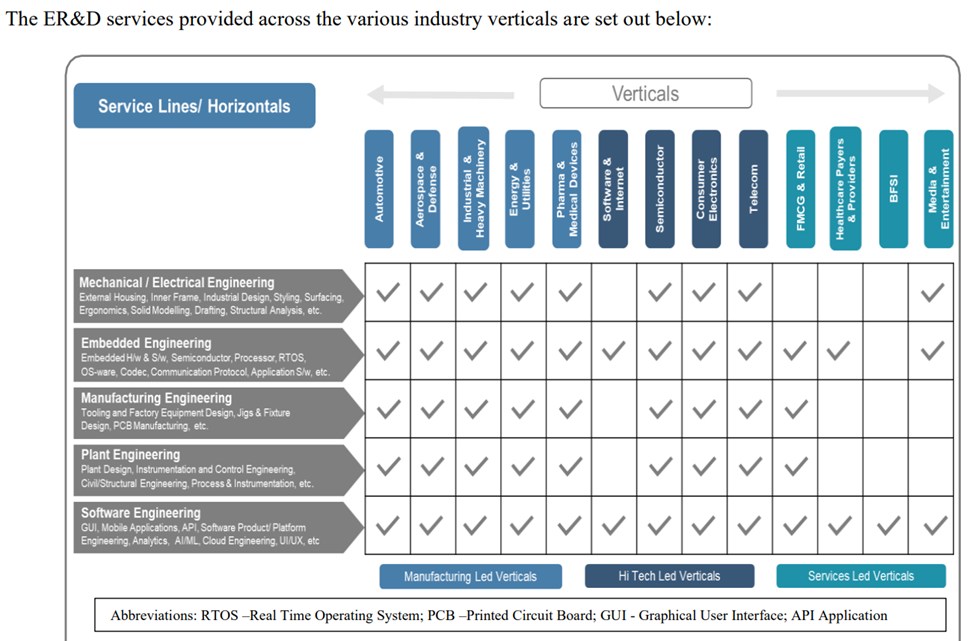

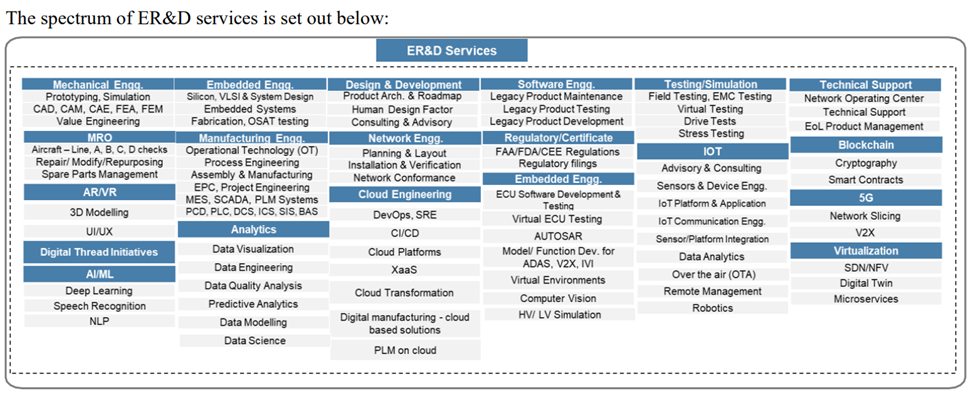

Engineering, research, and development (“ER&D”) services – product development and digital solutions, including turnkey solutions, to global original equipment manufacturers (OEMs) and their Tier 1 suppliers. ER&D services is defined as the set of services offered to enterprises on activities which involve the process of designing and developing a device, equipment, assembly, platform, or application such that it may be produced as a product for sale through software development or a manufacturing process. The ER&D services are broadly broken down into software, embedded, and mechanical engineering services as shown below:

-

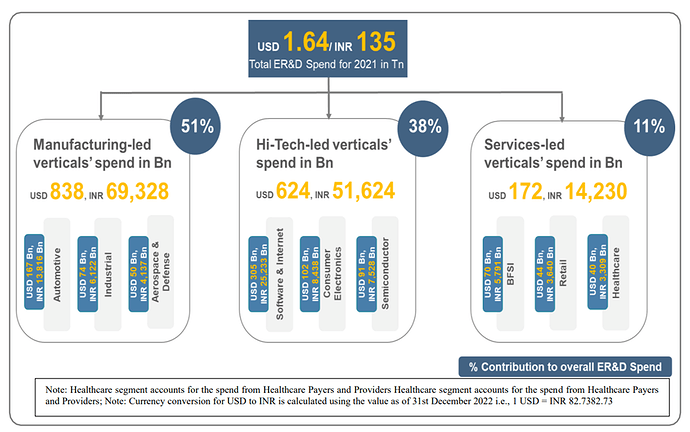

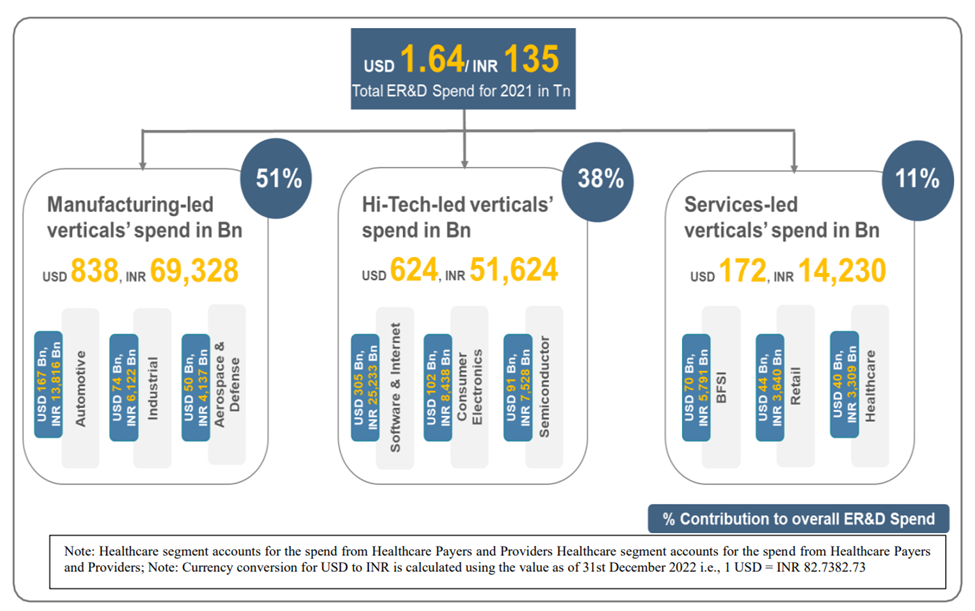

Manufacturing-led verticals (automotive, industrial, aerospace, defense, etc.): Account for more than half of the global ER&D spending. In terms of the expenditure, the automotive sector is the largest manufacturing ER&D vertical, and the second largest ER&D vertical overall, accounting for approximately 10% of global ER&D spend for 2021. [Tata Technologies’ focus area, just my understanding].

-

Hi Tech-led verticals (Software & Internet, Semiconductor, Telecom, etc.): Hi Tech-led verticals currently account for 38% of the global ER&D spend. Software and internet is the largest ER&D vertical, accounting for approximately 19% of global ER&D spend and is among the fastest growing verticals. [Tata Elxi’s focus area, just my understanding]

-

Services-led verticals (BFSI, Healthcare Payers & Providers, Media & Entertainment, etc.): Services-led verticals account for 11% of global ER&D spend, primarily driven by digital engineering investments. Though they currently make up the smallest portion of the ER&D spend pie, they are the fastest growing category. [TCS focus area is all the verticals for End-to-End solutions on IT front, in my opinion]

Opportunity Size:

- From Tata Technologies perspective, the automotive outsourced ER&D market is pegged at $16-18 billion, the aerospace outsourced ER&D market currently stands at approximately $7 billion, and the Transportation & Construction Heavy Machinery (“TCHM”) service provider outsourced ER&D market is currently pegged at $2-3 billion.

- From industry perspective, The ER&D spend outsourced to third party service providers reached $85-$90 billion in 2021 and is anticipated to grow at a 10-12% CAGR between 2021 and 2025.

Lines of Business:

1. Services offerings:

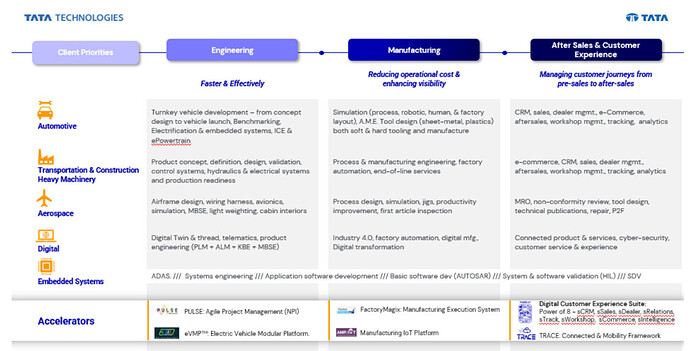

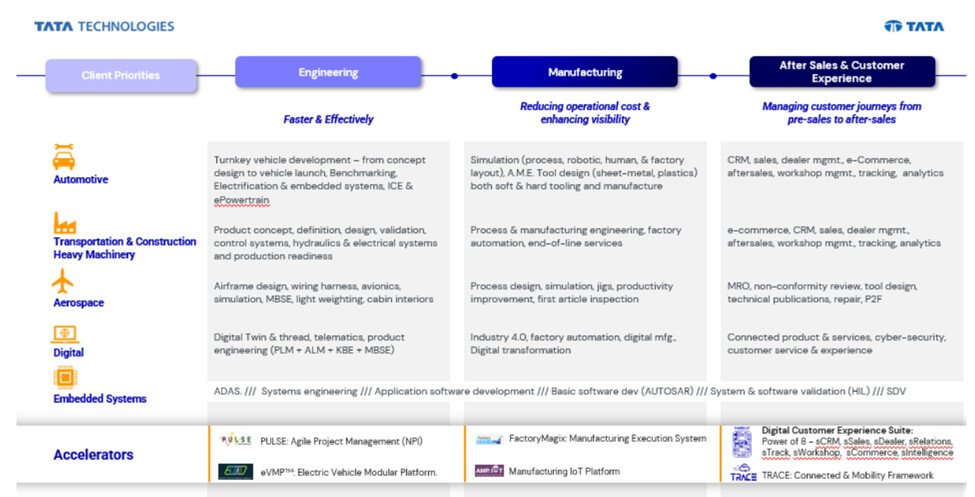

- Providing outsourced engineering services for manufacturing clients and leveraging digital technology to optimize the way in which a manufacturing company conceives, develops, manufactures, and services new products. We service our clients using our global sales network comprising 18 global delivery centers in North America, Europe and Asia Pacific, leveraging our balanced on-shore/offshore global delivery model. From shared services to components, subsystems, and systems, to full vehicle turnkey projects, we deliver complex engineering programs and expert domain services to our clients, leveraging a global resource pool throughout the product realization lifecycle. We also specialize in ‘digital thread’ which enables solutions across processes and enterprises. These enterprise solutions help OEMs address challenges of process effectiveness across their value chain from product development to customer experience and accelerate the digital transformation journey.

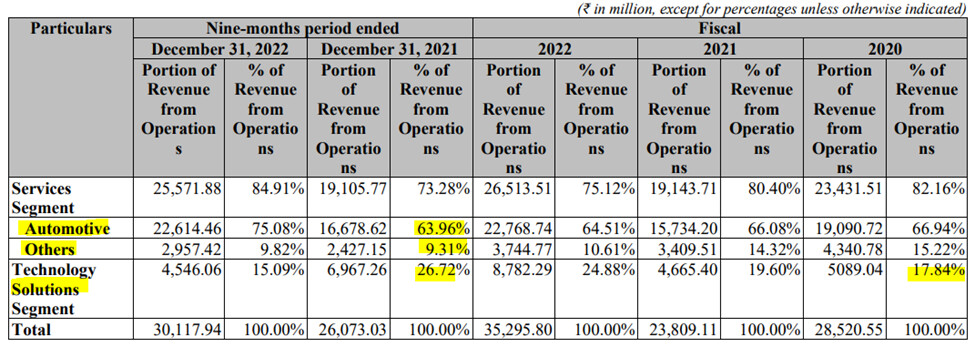

- We provide engineering services to clients primarily in the automotive vertical, as well as aerospace, TCHM and our other adjacent verticals. Automotive is our largest industry vertical which contributed 65 %, 66 %, and 67% to our revenue from operations for Fiscal 2022, Fiscal 2021, Fiscal 2020. We are currently engaged with six out of the top 10 and 11 out of the top 20 automotive ER&D spenders (across OEMs and tier 1 suppliers) and four out of the 10 prominent new energy ER&D spenders.

- We have capabilities in areas such as product engineering (new product development from concept to realization), value engineering (benchmarking, should costing and enabling design), manufacturing (lean and digital manufacturing, integrating digital thread with the manufacturing value chain), sales and after sales (omnichannel client experience and product lifecycle extension, effective maintenance, repair and operations). In addition, we offer multiple bespoke solutions such as pre-studies for concept vehicles, virtual simulation, body engineering, battery management systems, battery swap systems, ePowertrain, embedded infotainment, vertical integration of value chain, smart manufacturing, digital thread enablement, telematics and digital sales and marketing, data management systems (DMS) and service management. We also specialize in delivering turnkey full vehicle solutions, a competency developed over a period of 10 years, that has been facilitated by a global footprint that positions delivery centers close to our key and focused clients. With our turnkey full vehicle solutions, we primarily focus on the development of the digital product and the management of the test, validation and launch processes. While the building of protype parts/vehicles and physical testing is typically managed by the OEM, we also have such capabilities and have an established network of global partners to facilitate these requirements.Our full-service offerings are depicted below:

2. Technology Solutions offering:

-

Products business comprising of the reselling of specific software that manufacturing companies deploy to conceive, develop, build and service new products. The revenue from our Products business for Fiscal 2022, Fiscal 2021, and Fiscal ₹432 Cr., ₹424 Cr., and ₹486 Cr. respectively, representing 49 %, 91 %, and 96 % of our revenue attributable to the Technology Solutions segment.

-

Education business where we work with colleges, universities, private enterprises and State Governments to equip the next generation of engineers and technicians with relevant skills that are required by the global manufacturing industry. Our Education business focuses on addressing academia and corporate skilling requirements by leveraging our manufacturing domain knowledge and the iGetIT offering. iGetIT is based on the blended learning methodology that offers self-paced courses on more than 2,000 mechanical computer aided design (MCAD), PLM and niche skill sets.

-

The revenue from our Education business for Fiscal 2022, Fiscal 2021, and Fiscal was ₹446 Cr., ₹43 Cr., and ₹23 Cr. respectively, representing 51 %, 9 %, and 4 % of our revenue attributable to the technology solutions segment.

-

Assist our clients to identify and deploy technologies and solutions that are used to manufacture, service and realize better products, as well as train people who need to enable the development of these competitive products. Our long-standing relationship with third-party software vendor partners (such as Dassault Systemes and Siemens Industry Software Inc. among others) on PLM, MES and ERP allow us to select and implement full solutions (including systems integration) for our clients. We are an important sales channel for our third-party software vendor partners, given our understanding of client requirements along with our offering of presale and post-sale support to the client. In addition, we enter into partnerships that also focus on PLM, MES and ERP, IOT, Industry 4.0 and data and digital customer experience.

The table below sets forth our industry verticals and their percentage contribution to our revenue from operations for the periods indicated:

Pricing Model and Contractual Terms:

Our suite of offerings helps us to target clients across the value chain, from basic resourcing and technical documentation services to high-end turnkey and full vehicle program services and digital enterprise solutions, such as IoT and digital twin. We generate a large portion of our revenue from our Services business through which we offer a range of engagement models, from basic staffing services offered as a time-and-material based pricing to outcome-based deliverables engagement (offered as part of and falling in the category of our fixed-bid services) where pay-out is linked mainly to the outcomes delivered.

Proprietary Platforms and Intellectual Property:

- Our service offerings are well supported by advanced proprietary platforms across the value chain, including the following:

- Product Development: eVMP, a scalable and flexible electric vehicle accelerator platform for new energy vehicle companies or OEMs, providing rapid configurations as per client specifications to help enable reduced NPI cycle time and quicker launch timelines and PULSE, an agile program management tool with six modules for end-to-end ER&D process tracking.

- Manufacturing: FactoryMagix is a manufacturing execution systems solution that enables real-time data visibility providing improvement in overall equipment effectiveness. AMP.IOT is an IOT platform for improving traceability and efficiency in manufacturing operations, enabling plant monitoring and setting up a command center.

- Customer Experience: Power of 8 is a client lifecycle management platform in the automotive industry which helps to digitize the bulk of client engagements and has led to improved digital lead conversions. TRACE is an IoT-led connected vehicle platform for fleet management and telematics, deployed in thousands of vehicles while the REMO mobility platform helps in connectivity of enterprise systems on-the-go through preconfigured services, with over 200,000 satisfied users.

Global Delivery Model:

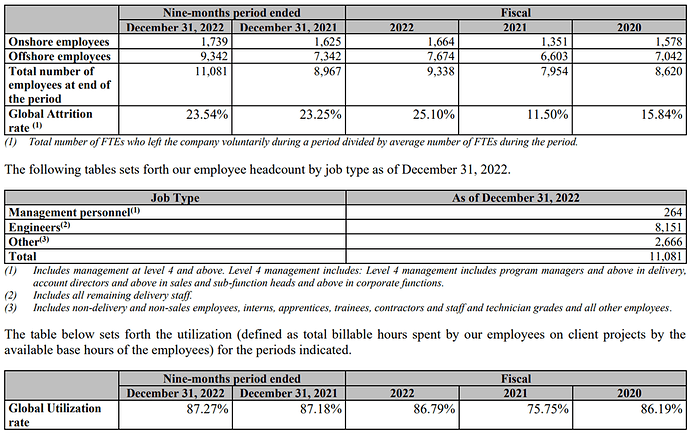

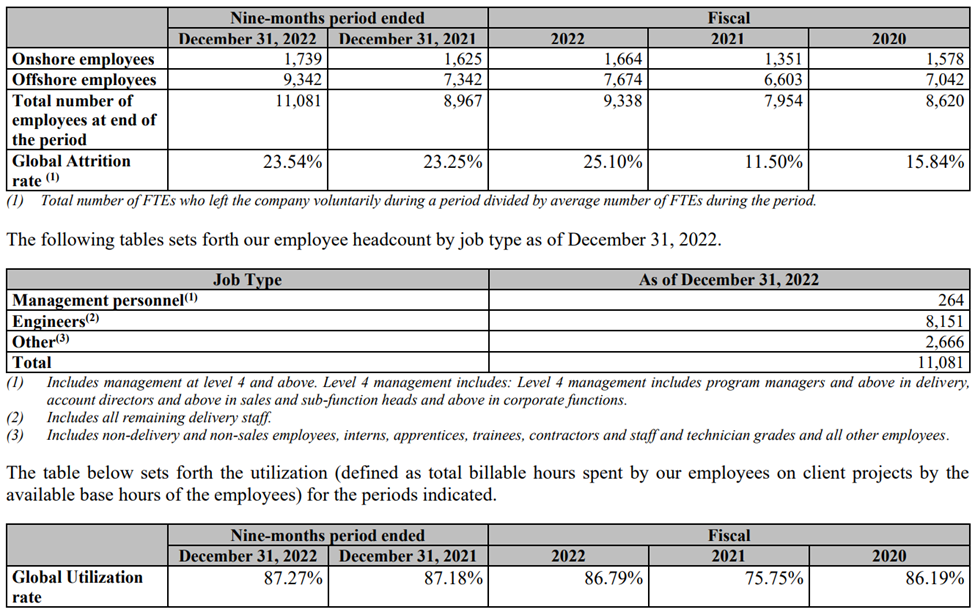

- We service our clients using our global sales and delivery network comprising 18 global delivery centers in North America, Europe and Asia Pacific. At each of our global delivery centers we employ a majority of local nationals which allows us to maintain a responsive local presence near our clients. We have a local presence in all the key automotive ER&D markets globally with approximately 1,300 employees in Europe, approximately 330 employees in North America, approximately 300 employees in Asia Pacific, excluding India, and 9,000 employees in India, each as of December 31, 2022.

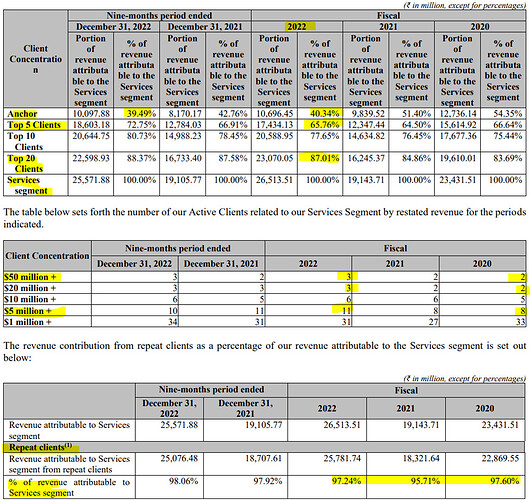

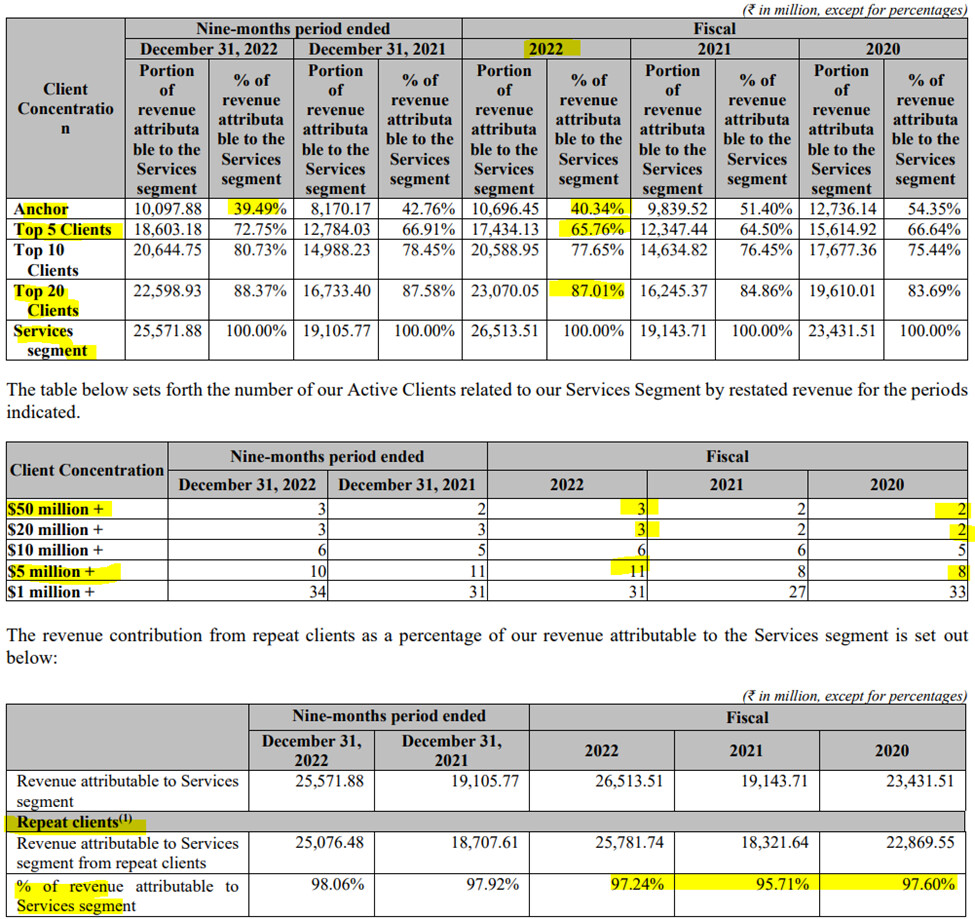

- The table below sets forth our key client concentration, in terms of our revenue from sale of Services for the periods indicated.

Risk Factors:

- A material portion of our revenues from top 5 clients – (JLR and Tata Motors together, the “Anchor Clients”) and VinFast, a Southeast Asian electric vehicle OEM and one of the Top 5 Clients, across multiple full vehicle turnkey models.

- 80+% of the Services segment revenue from AUTOMOTIVE industry

- High attrition rate, ~25% in FY22

- Increasing % of fixed price contracts compared to time-and-material contracts –Ratio at 53%:47% in FY22 from 45%:56% in FY20

- 70% revenue in foreign Currencies

- Lumpiness in revenue: Due to completion of vehicle programs and delay in the start of new programs as evident in FY18.

- Various other risks in example form:

- For instance, the contract with one of our clients in the aerospace industry provides for our Company’s uncapped indemnity for breach of its obligations under the agreement.

- For instance, after our operations in Mexico did not meet our desired growth expectations, we ceased operations in Mexico and begun the voluntary liquidation of our Mexican subsidiary, Tata Technologies de Mexico, S.A. de C.V., in March 2020.

- For instance, there have been delays in the past in payment of dues and repatriation of funds by foreign subsidiaries under the terms of the Reserve Bank of India, Master Direction – Export of Goods and Services, 2016.

- For instance, certain of our clients, which are nascent companies in the automotive segment and who rely on us for a large majority of their engineering services requirements, could subsequently build up their captive R&D capabilities and accordingly reduce their dependence on our services.

- For instance, recent restrictions on the issuance of employment visas imposed by the United States mean that we are unable to obtain new visas for our employees to work in the United States as of the date of this Draft Red Herring Prospectus. If the immigration laws in such countries change and make it more difficult for us to obtain non-immigrant visas for our employees, our ability to compete for and provide services to our clients in such countries could be impaired.

- For instance, we rely on a European OEM software manufacturer for certain software, products, and services with respect to our education and training services in India and the United States.

Contingent Liabilities:

Miniscule

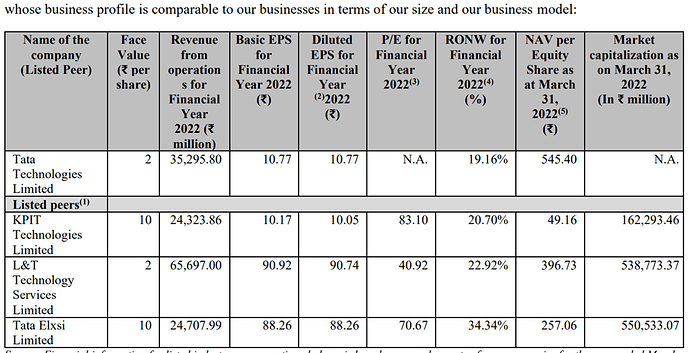

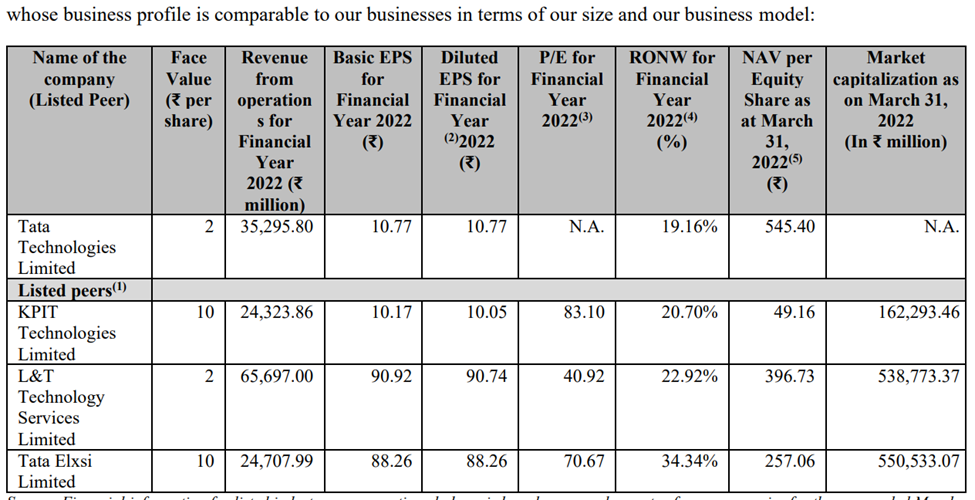

Competitors:

- Key competitors in the ER&D service market include pure play Indian ER&D service providers such as L&T Technology Services, KPIT Technologies and Tata Elxsi, IT service providers such as Tata Consulting Services (“TCS”), Wipro and Tech Mahindra, global ER&D service providers such as Bertrandt, Magna Steyr and EDAG and in-house ER&D departments of the clients

- Global footprint with balanced talent presence across offshore and onshore locations, deep domain knowledge, technological and process knowledge and capabilities, scale capacity, ability to undertake turnkey projects and our long-standing client relationships are our key differentiator to compete effectively.

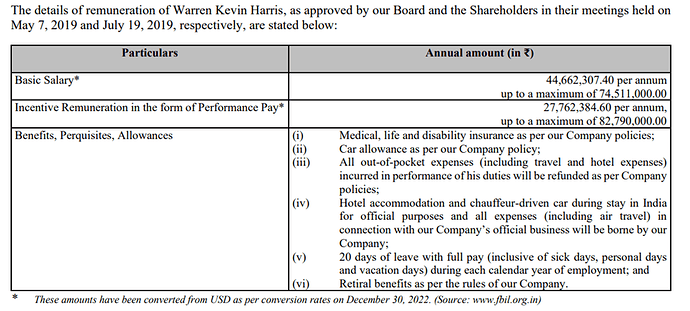

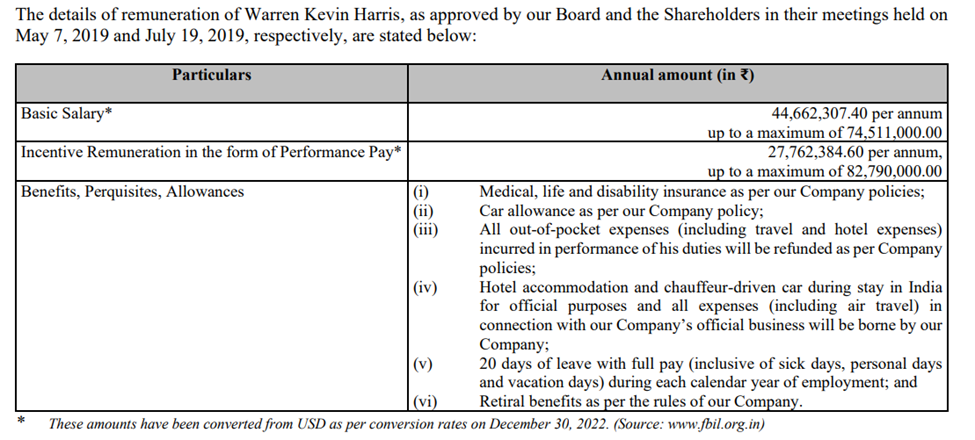

CEO and MD: Warren Kevin Harris

- Associated with our Company since October 1, 2005.

- Remuneration:

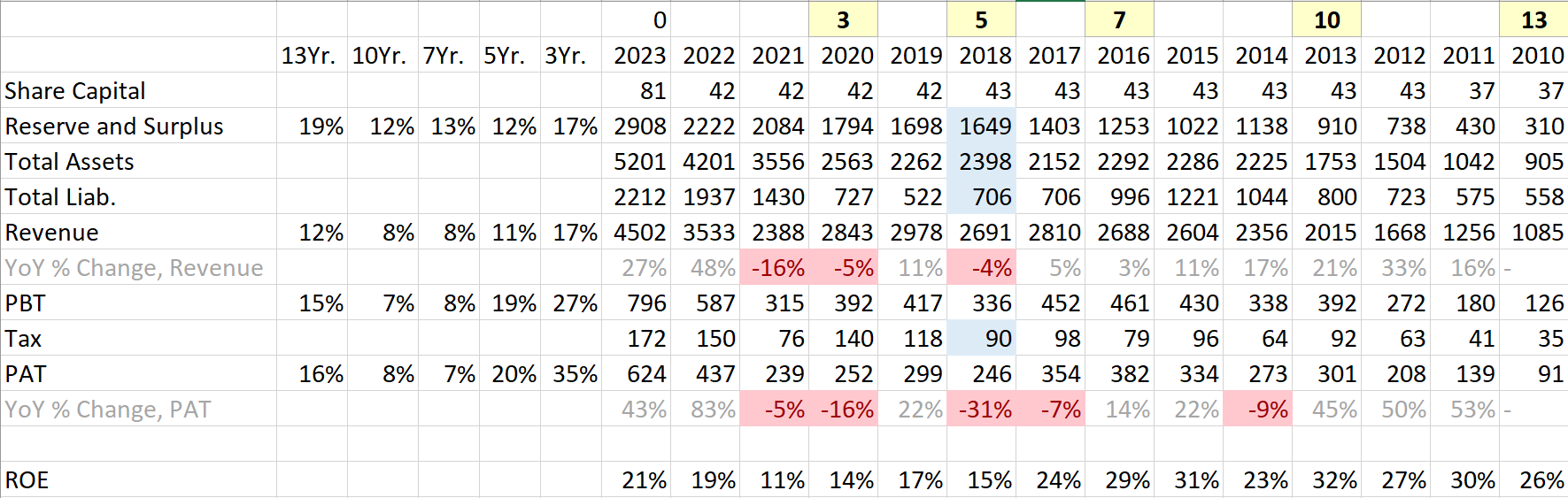

Summary of Financial KPIs:

Historical data from Tata Motor’s AR [In the AR, data of Year 2018 is same as the data of Year 2017. I have adjusted the data to the best of my abilities]:

| Subscribe To Our Free Newsletter |