Hi there, thanks for your kind words! I am glad you found my notes helpful.

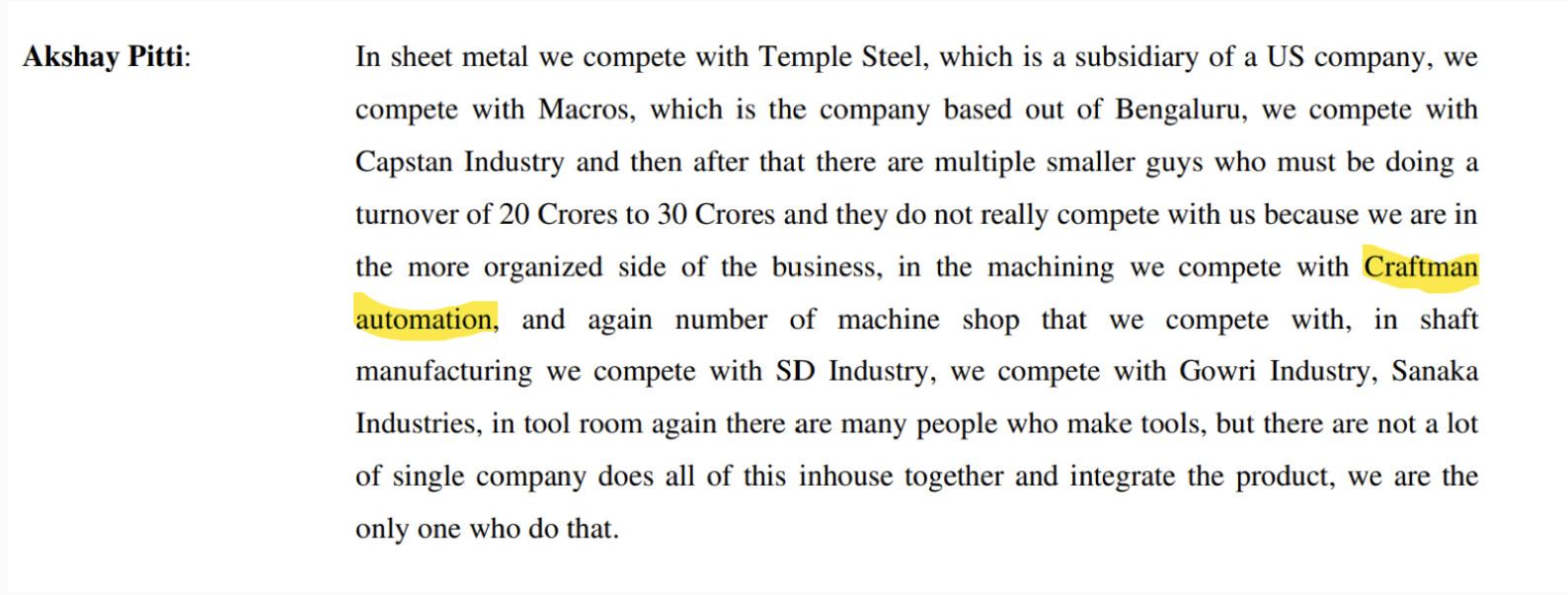

This industry is highly fragmented, but Pitti is indeed a market leader in the organized lamination and machining. Currently, they have 8% market share as the management notified in the last concall, but they aspire to take it to 10-12% in coming years as they increase add more capacity (72000 tonne max volume, total market size is 500,000 tonne). Pitti competes with a lot of player in a few parts of the value chain (like sheet metal, machining, tool shop), but according to the management, no competitor does the complete value addition. Next competitor is half the size of Pitti. Please refer to the following concall snippet for understanding the competitive landscape.

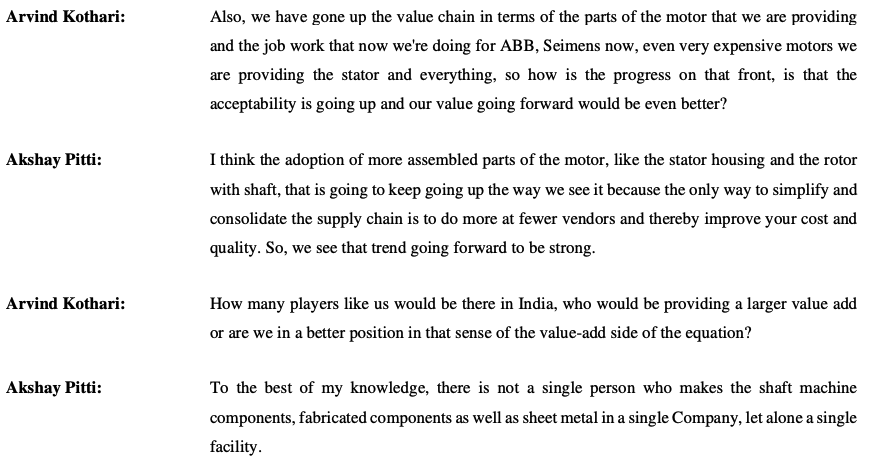

Management also claims that is there is not a single facility in India that makes shaft machine components, fabricated components and sheet metal (value chain of the motor assy). Trend is customers are moving towards suppliers that are moving up the value chain like Pitti because they want to simplify and consolidate the supply chain.

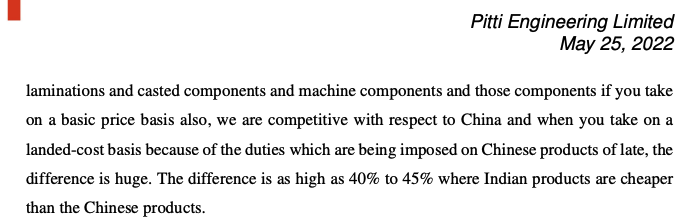

Management also says that lamination and casted components used in motors made in India are 40-45% cheaper than China

Tempel Steel: Second largest in India (18000 tons current capacity in FY23)

Magcore, Capston: All in the range of 8000-10000 tons.

As far as the moats are concerned, Pitti management claims to have the following competitive advantages:

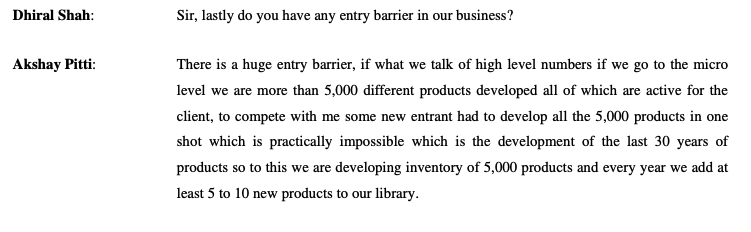

- High library of products used in the value chain. Company claims to have 5000 products active for the clients and adding 5-10 new products every year. Any new entrant has to develop 5000 or more products to keep up.

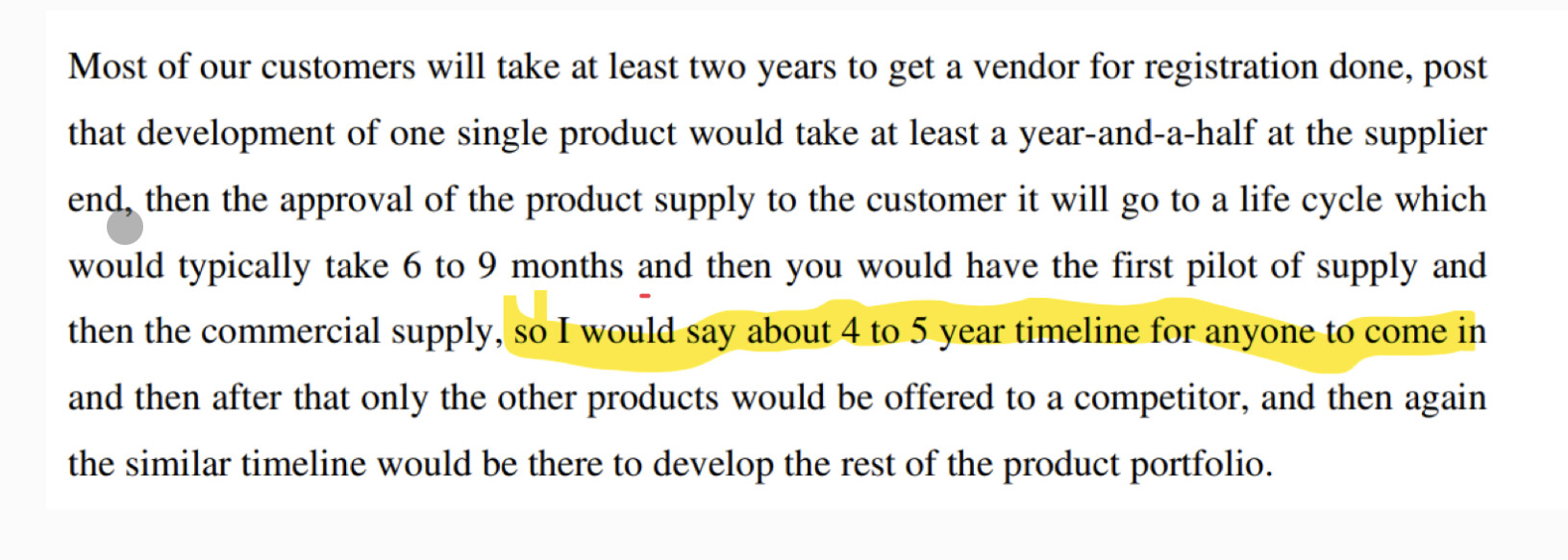

- Lengthy Approval Process by the clients: Takes 4-5 years for the clients to get a new vendor approved that too per product basis.

-

Company has their own tool shop, their machine shop, mfg facility. One stop shop for all the operations to create finished goods. This helps in achieving good quality, better cost, less issues with dealing multiple vendors for the clients. A new player has to do all the value chain operations under one roof which is quite cost intensive.

-

Economies of scale: All other players are pretty small in terms of volume. Second player is at 18k tons capacity while Pitti is at 32000, planning to go to 58k (80% of 72k tonne volume)

Hope this helps!

Disc: Invested, so I have vested interest in this company.

| Subscribe To Our Free Newsletter |