KEY TAKE AWAYS FROM Q1 FY24 of PCBL ( and my insights)

-

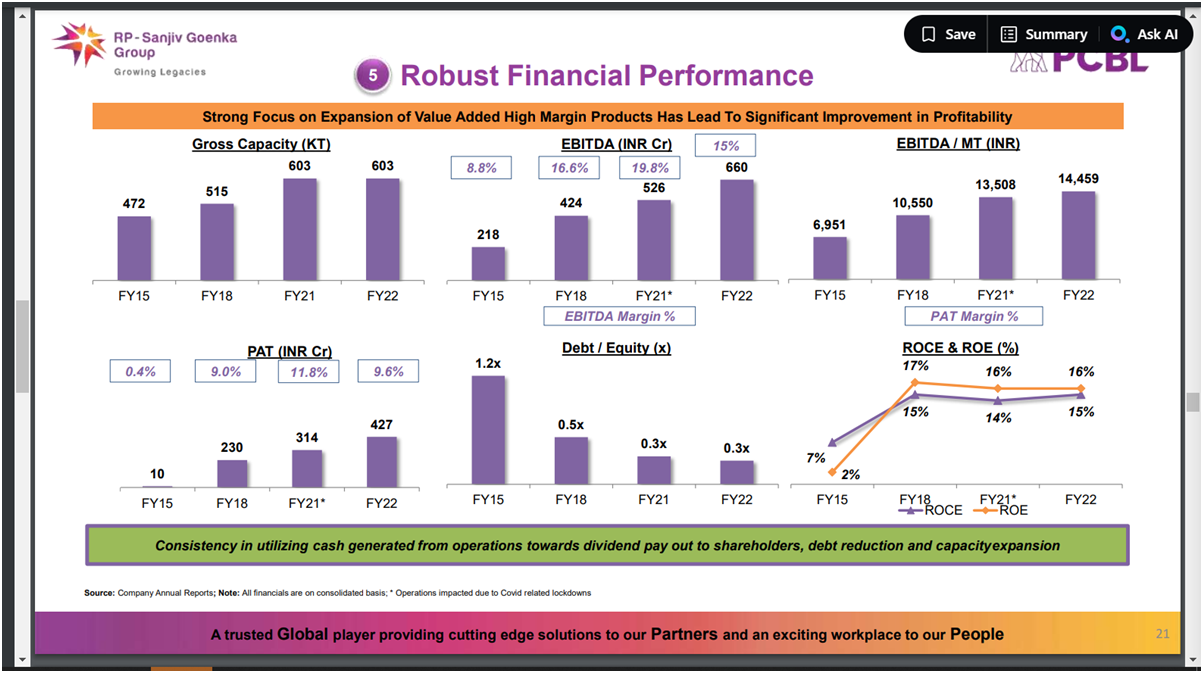

Company has been able to increase revenue and margins.

Yet QoQ PAT is down because of a change in tax from 22% to29% (due to end of tax subsidy on profit from power generated which was there for last 15 years.) -

Company has been gradually improving its product mix hence yielding better margins

Speciality Chemicals which until a few years back was 4% in FY2018 is now risen to 8% and performance chemical too share too have increased. Thus the Carbon Black, a commodity product share in overall revenue share has decreased.

-

China and Russia are no threat to Indian markets in the near term.

Despite some imports from the above countries in India, India on a net-net basis is an exporter of CB to the tune of 1L tonnes of CB. -

Company is focused on producing better grades of conductive chemicals for batteries. Company has an R&D team working on various specialty chemicals.

-

Company mentioned having a mechanism to avoid and absorb small shocks in crude prices to avoid inventory loss or gains. They have long contracts for supply of Carbon Black.

6)Regarding capex the Tamilnadu facility,its ready and until April was operating at 45% capacity ( which happens to breakeven production capacity). Production batches and its quality would stabilize in this quarter. Thus it would start contributing and increase the bottom line in coming quarters. Demand is firm.

Brownfield expansion of the Speciality product line of 20K tonnes in Mundra has also got commissioned.

Tamilnadu unit production would help to cater the domestic players ( tyre manufacturers) in the state.

-

Sanctions on Russia ( which exports CB to EU countries) will open some opportunities for exports for CB manufacturers in India.

-

Company sees the need for capex in the coming few years. They do have sufficient land for the next capex at Tamilnadu and Mundra, despite the capex announced or started by other players in India.

It takes approx 2 years for a greenfield capex. -

Company stays cautious about global demand and expects domestic demand to be firm.

-

Post the Tamilnadu plant going onstream with near to full capacity utilization, the tax rate again likely to drop from 29%/31% levels to 22% about levels.Can expect a tax rate of 25% for next quarter.

The way I connect dots

A) Since Russia would be imposed by more sanctions to export CB to EU countries, global demand can remain firm. Russia exporting to India is not feasible due to logistic costs and CB landing prices from CHINA to India being much higher, both Russia and China don’t seem to be a threat for the domestic or export business of PCBL.

The current tailwind in the tyre industry augurs well for the domestic demand of CB.

B) Increased efforts on R&D and improving product mix, plus long contracts for CB to tyre companies, should help PCBL for sustained and relatively stable OPMs.

C) The conductive speciality chemical of high grade and purity, looks a good optionality trigger.

The company do produce battery chemical of lower grade which is used in Lead Acid batteries.

D) Tax rate going down from 29% to 25% itself will impact positively the bottom line looks very much possible in next quarter.

E) The stabilization of production from the new TN plant and sales to companies would enhance the revenues and PAT in coming quarters in a gradual manner.

F) Debt declined further by 50cr in this quarter

The only spoiler could be,if any sharp & sudden movement in crude prices.

Secondly if any global slowdown due to maco risks.

Disc : I am invested

This is my first post on VALUEPICKR

| Subscribe To Our Free Newsletter |