Ugro recently released their Annual Report. A few observations from the report.

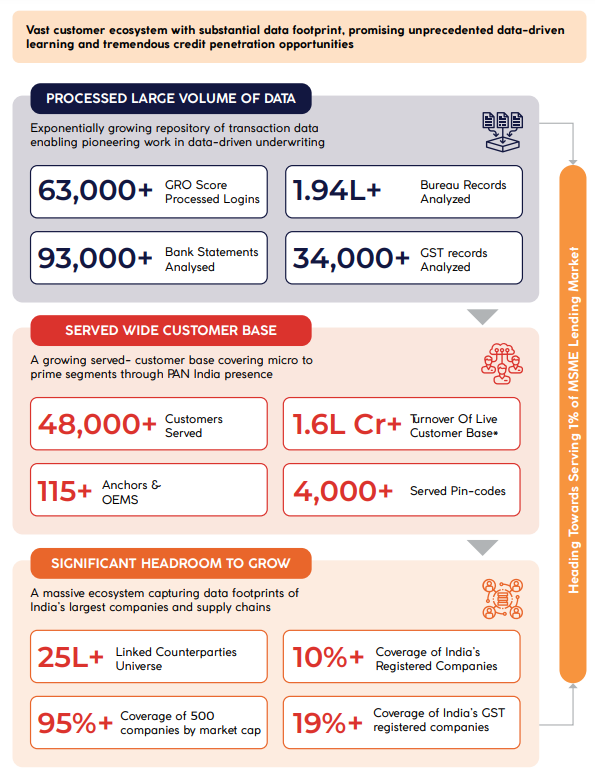

They’ve processed 34k GST records, 93k bank statements and 1.94L+ bureau records. These are still small numbers in the context of the overall MSME universe in India. As the amount of data crunched increases, the hope is their credit underwriting models become more robust.

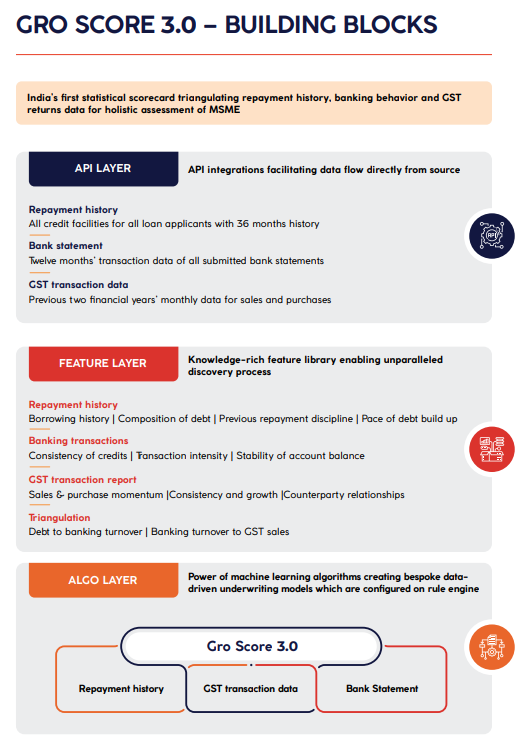

Some insights into the data and feature layers of their Gro Score 3.0 Algorithm. Data science domain experts on this forum may like to take a look at this snapshot and the one above and provide their comments if any.

Below are some aspects that need management questioning IMO.

As per the graphic, 59% of machinery finance is to the Hospitality sector. What kind of machines might hotels be buying?

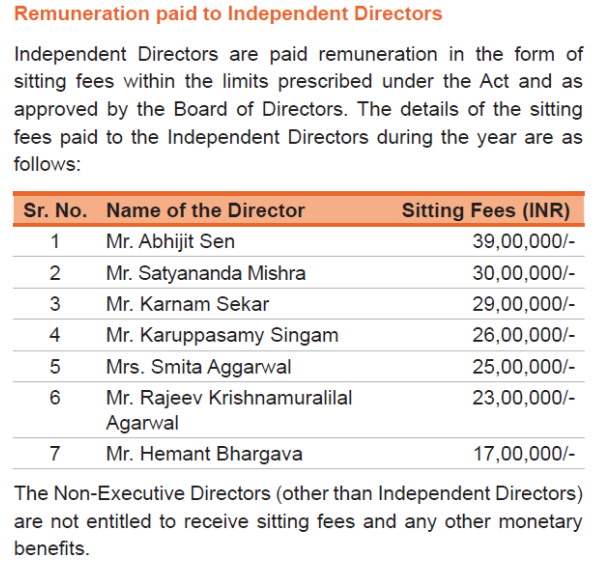

Sitting fees paid to the independent directors are very high compared to what is normally paid by other companies. The company has always maintained it wants to be a Board driven organization. Are these fees being paid to attract reputable independent directors who would otherwise not be interested in advising a small company like Ugro? Similar sums were paid last year as well.

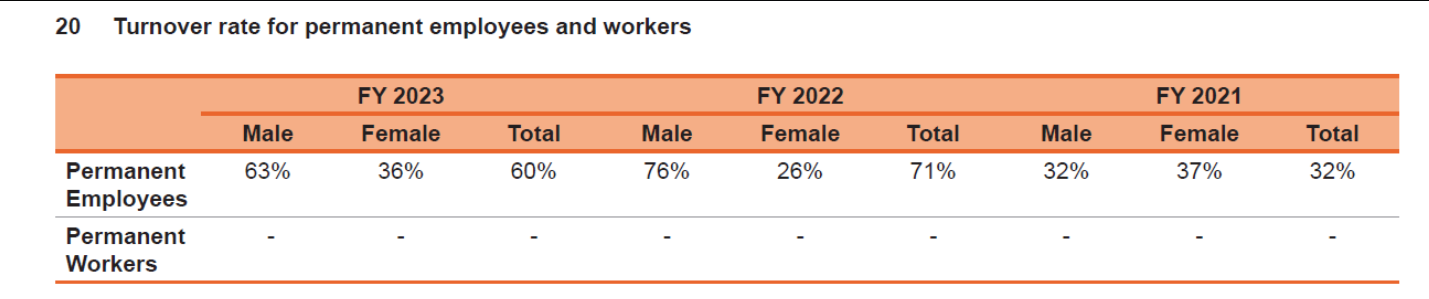

The employee turnover rate for FY23 was 60%, down from 71% in FY22. In FY21 the number was 30%. I assume most of this is front end sales force turnover. Does anybody know comparable turnover data for other relatively newly established NBFCs? We can benchmark this number.

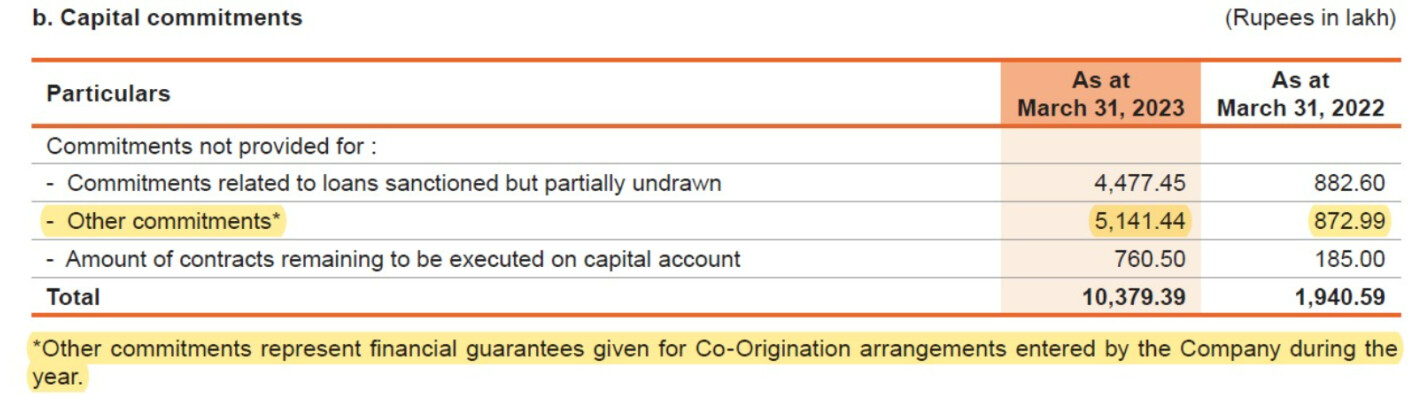

They have ~51Cr worth of contingent liabilities earmarked as financial guarantees given for co-origination arrangements. This means this 51Cr is FLDG guarantee provided by Ugro to its co-lending partners for its co-origination book (Co-lending doesn’t need any FLDG, co-origination does). They have a co-origination book worth 488Cr as of FY23, so the FLDG guarantee stands at ~10% of the co-originated amount. That’s a higher % than earlier understood (Earlier understanding was that this would not be more than 3-4% of co-originated amounts)

New CFO (Kishore Lodha) seems to be on 3x+ salary of the earlier CFO (Amit Gupta). MD’s salary has also increased by 58% YoY.

Disc: Invested and biased.

| Subscribe To Our Free Newsletter |