Good results – https://www.bseindia.com/xml-data/corpfiling/AttachLive/6e2ee3df-a731-4cc2-9c8a-11dd4d78e060.pdf

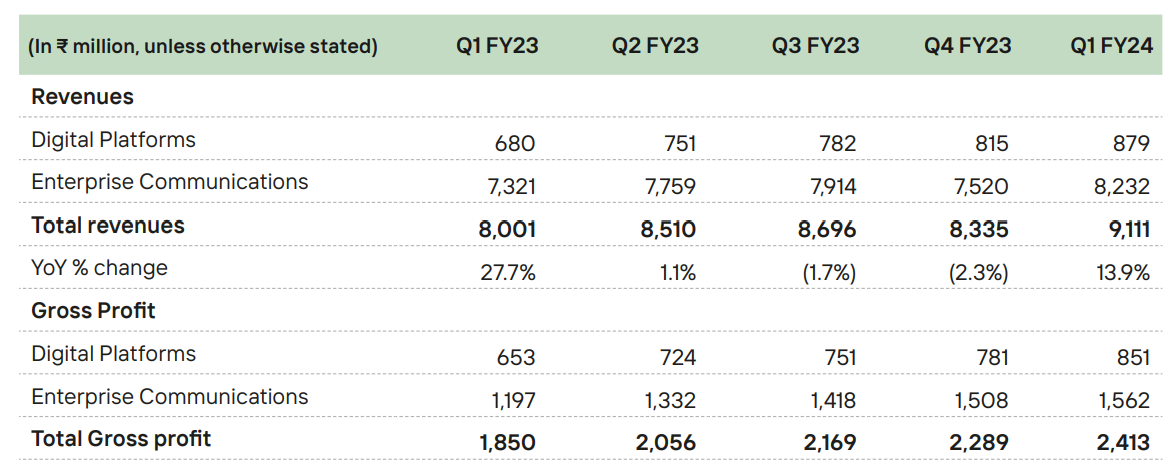

PAT up 35% YoY and 12.5% QoQ. EBITDAM 20% for the second quarter running, so hopefully margin only goes up from here.

A few points from investor documents:

- Looks like Tanla has entered into some kind of a deal with Amazon for domestic biz – could be an NLD tie-up?

- Tanla is hinting that NLD rates may be revised upwards in Q2 after 3 years. If this guidance is correct it can be a big booster for profitability. But with Tanla, I will believe it when I see it.

- Expects commercial agreements for Wisely ATP to be signed with 3 leading private banks in early Q2.

- Enterprise GMs have contracted 100bps QoQ from 20% in Q4 to 19% in Q1. This means while pricing environment and competitive pressures maybe easing as per management, they are certainly not out of the woods here and this needs continuous monitoring. For reference, enterprise GMs in Q4 FY22 (prior to the significant business hit in Q1 FY23) were 22.7% and they had bottomed in Q1 FY23 at around 16.5%. So Tanla is still some way off from recovering to peak margins in enterprise biz.

-

Enterprise revenue growth pushed by higher share of Whatsapp communications (170% YoY growth) and ILD price hikes (As far as I am aware, ILD price hike had happened in H1, so why impact in Q1 of the next year?)

-

ValueFirst India nos to start getting consolidated from Q2 and VF Middle East nos to start getting consolidated from Q3.

-

36Cr investment in platforms (14Cr development and 22Cr in improvement) in Q1. This is very vague, would be nice to have specific details of which platform component this investment went into and what were the improvements. Otherwise, customer discounts on these platforms via volume based deals could also qualify as “investments”. This expense has been capitalized.

-

21Cr investments towards GTM and customer success – this looks like discounts or promotional items – should explain the 100bps slide in GMs sequentially, In related items, receivable days have expanded from 62 in Q4 to 76 in Q1 (These are all signs Tanla is aggressive in the market to gain market share and at the same time the demand environment may not be back to full health yet, push sales needed)

-

CFO is 129Cr and CFO/EBITDA is at a healthy 70%+ mark for the Q.

Things are finally looking up for Tanla (as reflected in price action) with several triggers

- Possible NLD price increase

- Wisely ATP rollout

- VF consolidation which will be EPS accretive from Q2

Some additional, unsolicited views having been invested in this stock for 2+ years now: In times of bullishness, the management tends to get over-enthusiastic, so I’d take management guidance with some moderation. Also, in my view, this is a business that should have a fair value PE multiple of 25-30x in normal times (While their ROCE and cash generation are fantastic and probably deserve a higher PE multiple, they are still one geo dependent and 70% of their GMs come from a pretty competitive and partly commoditized enterprise biz. In addition, they have a rocky history so market needs several years of steady performance to re-rate this stock). Of course bull markets and narratives can stretch that valuation number, but I’d have 25-30x PE multiple as my anchor.

| Subscribe To Our Free Newsletter |