A word of caution for all investors. A few months back I discussed KSolves with an IT veteran ex-Mphasis and ex-Cap Gemini. He was involved in salesforce implementation for Cap Gemini. He warned me about Ksolves. Not that the company is not genuine.

It just does plain vanilla Salesforce implementation. During Covid there was a boom in cloud services. Every company in the world which did not have an online presence had to have one. So there was a boom in AWS, Google Cloud, Azure, Salesforce etc.

So IT companies were throwing money to hire people implementing cloud services. Post the deluge of work the cloud work has normalized and decreasing. So they are firing people.

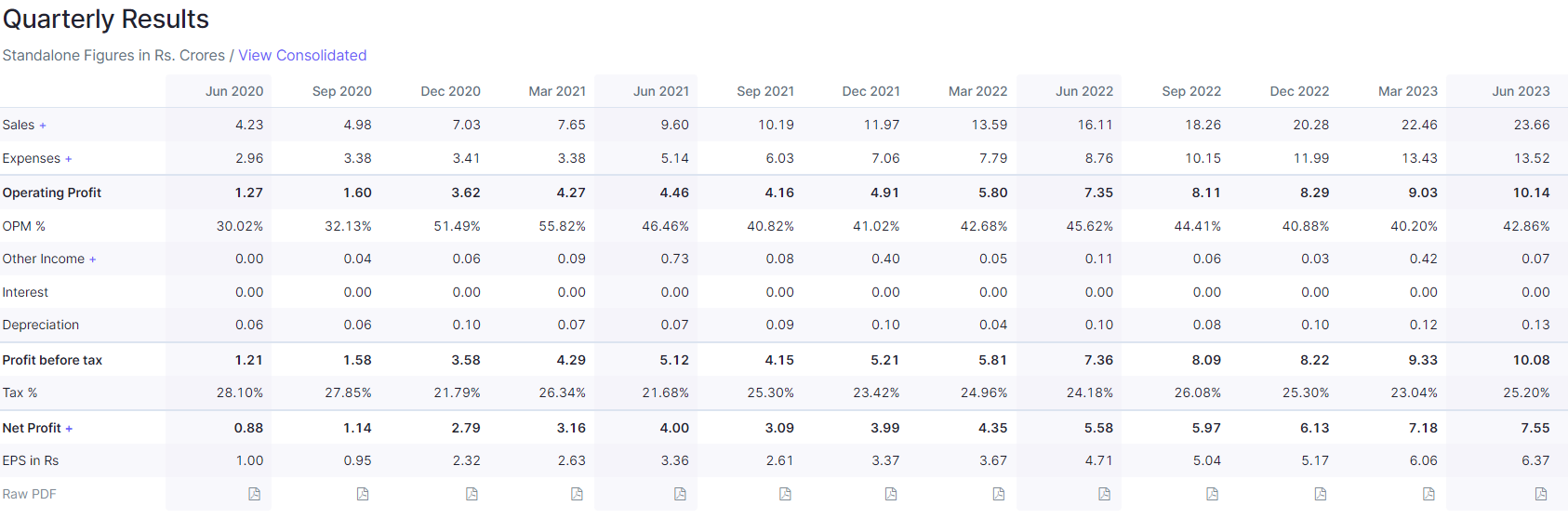

Ksolves is a tiny company, hence the revenues will disappear later as the base is small. The ramp up of revenues over last 3 year is not sustainable. It will come down over the next 3 years. The first sign of slowdown you have seen in the tepid QoQ growth over the last 3 quarters. Don’t get mislead by the YoY numbers. This is not a YoY comparison company.

This was a one time opportunity and that is why dividend payouts are so high. The promoters are aware the revenues wont be there in 3 to 4 years. So they are cleaning the coffers the right way by paying themselves and minority investors dividends (all clean and above board) -dividend payout ratio of 74%, 44% and 52% over the past 3 years. In the meantime whenever there is chance promoters will sell down stake to buyers who think this is the next big thing.

Let me draw 2 more parallels for you to understand.

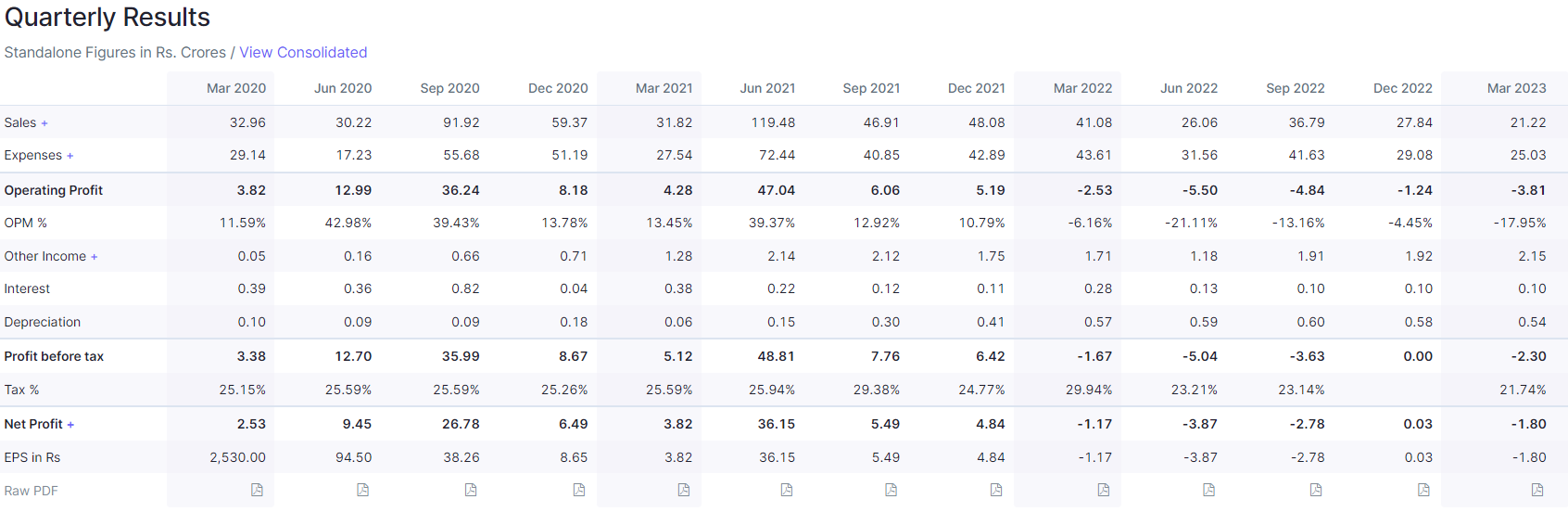

- Nureca which was selling oximeters imported from China. See the numbers below. With Covid behind us the numbers the revenues have shrunk

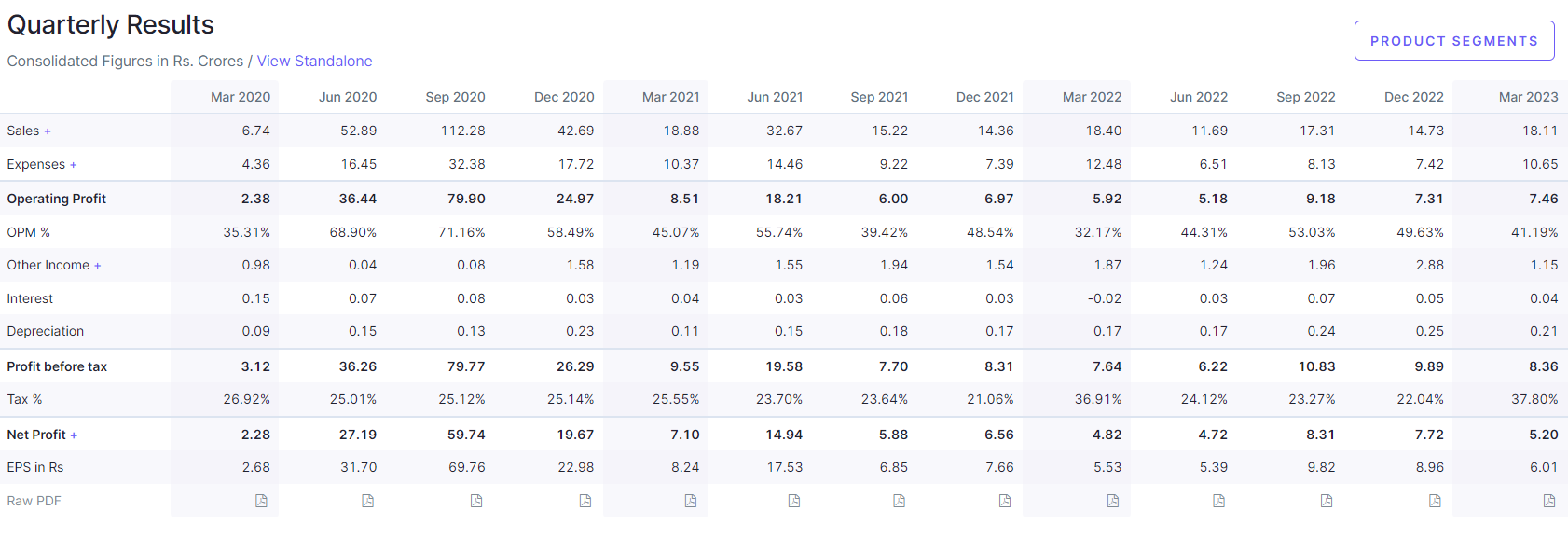

- See Kilpest. Once the price of RTPCR tests collapsed as more players came in and Covid was behind us the revenues shrank.

So net net the terminal value of this stock is perhaps 0 unless they come up with a new sustainable business.

| Subscribe To Our Free Newsletter |