Interesting slides from the PPT.

-

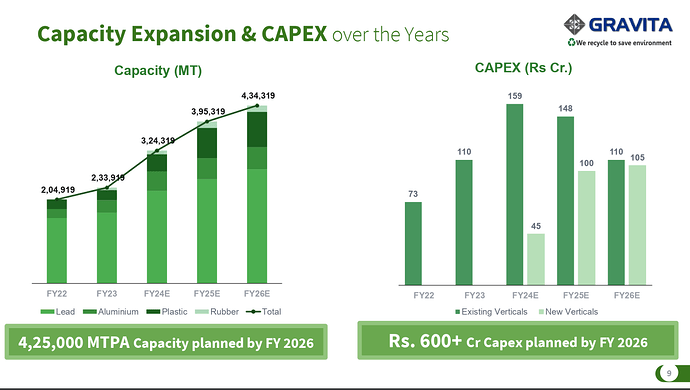

Capacity to almost double by FY26E: From 2,33,915 MT to 4,34,319 MT

-

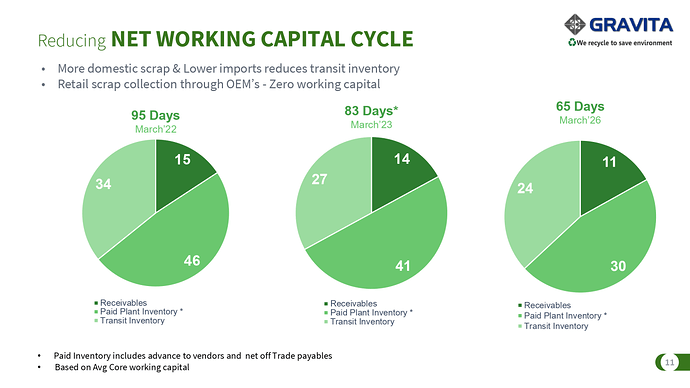

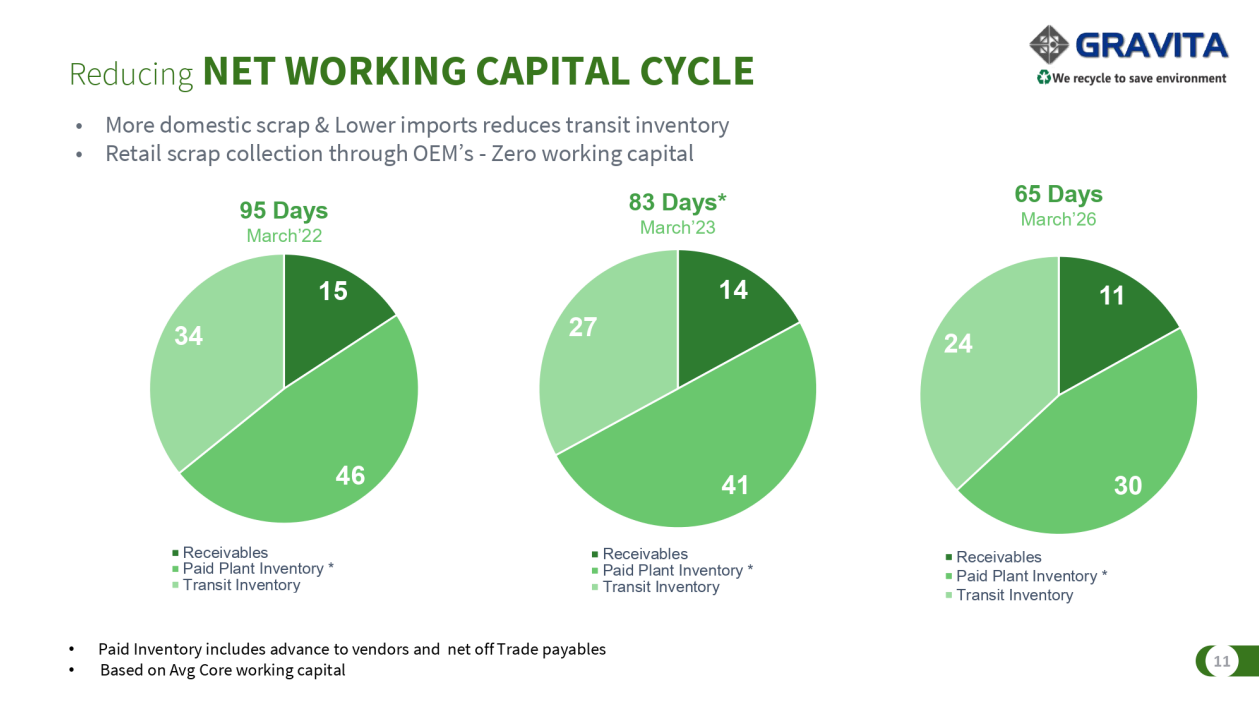

Working capital cycle to reduce from 83 days to 65 days by FY26. Therefore improving the cash flows.

-

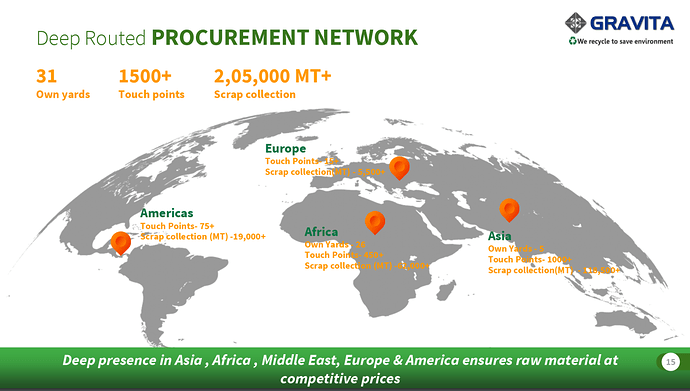

MOAT?

Apart from the ones mentioned by company. I believe the procurement network of the company and the global & pan india operations setup is a bigger barrier to entry and will be challenging for any new player to replicate easily. Requires years of good relationships with OEM’s and speciality knowledge which takes years to build.

-

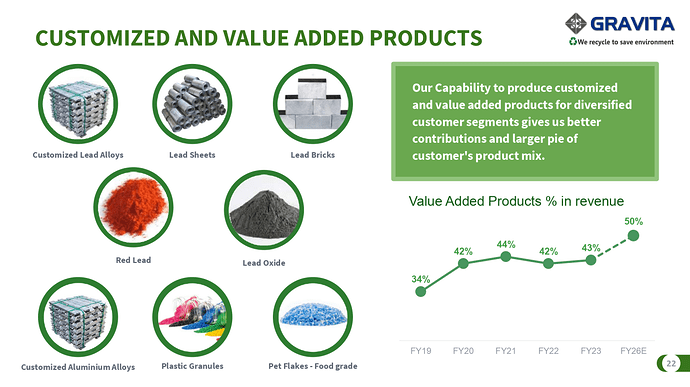

Value added products to increase from current 43% to 50% by FY26E. This should significantly improve the operating profit margins.

-

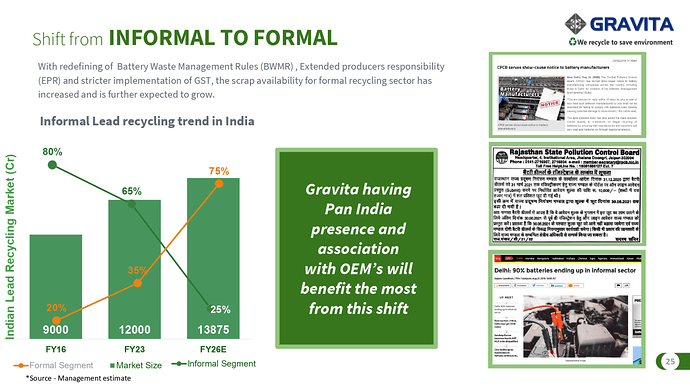

Sector tailwinds due to government policies and rules involving Battery Waste Management & stricter implementation of GST. Formal recycling sector to grow from current 35% to 75% by FY26E.

Disclaimer: Invested

| Subscribe To Our Free Newsletter |