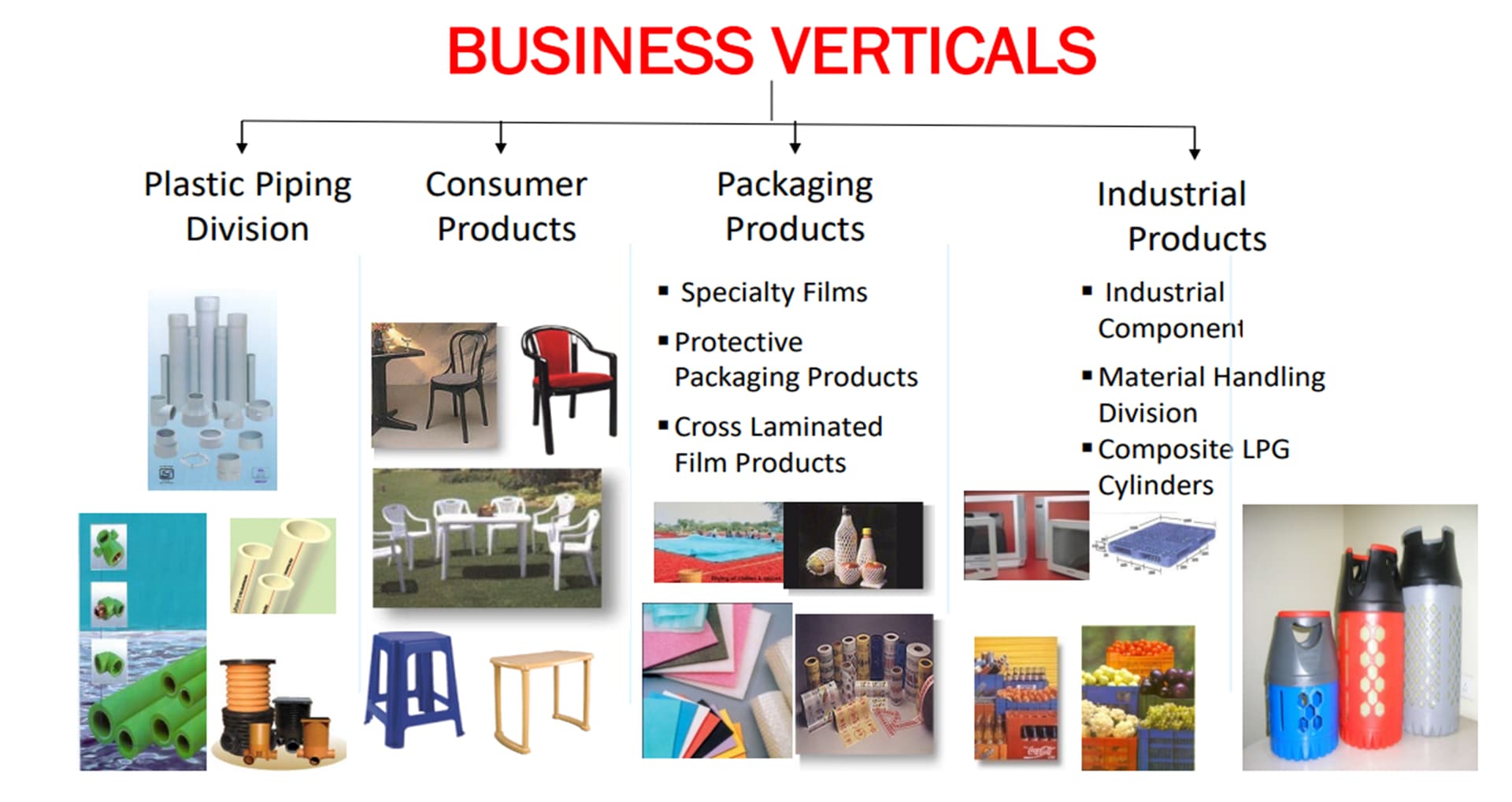

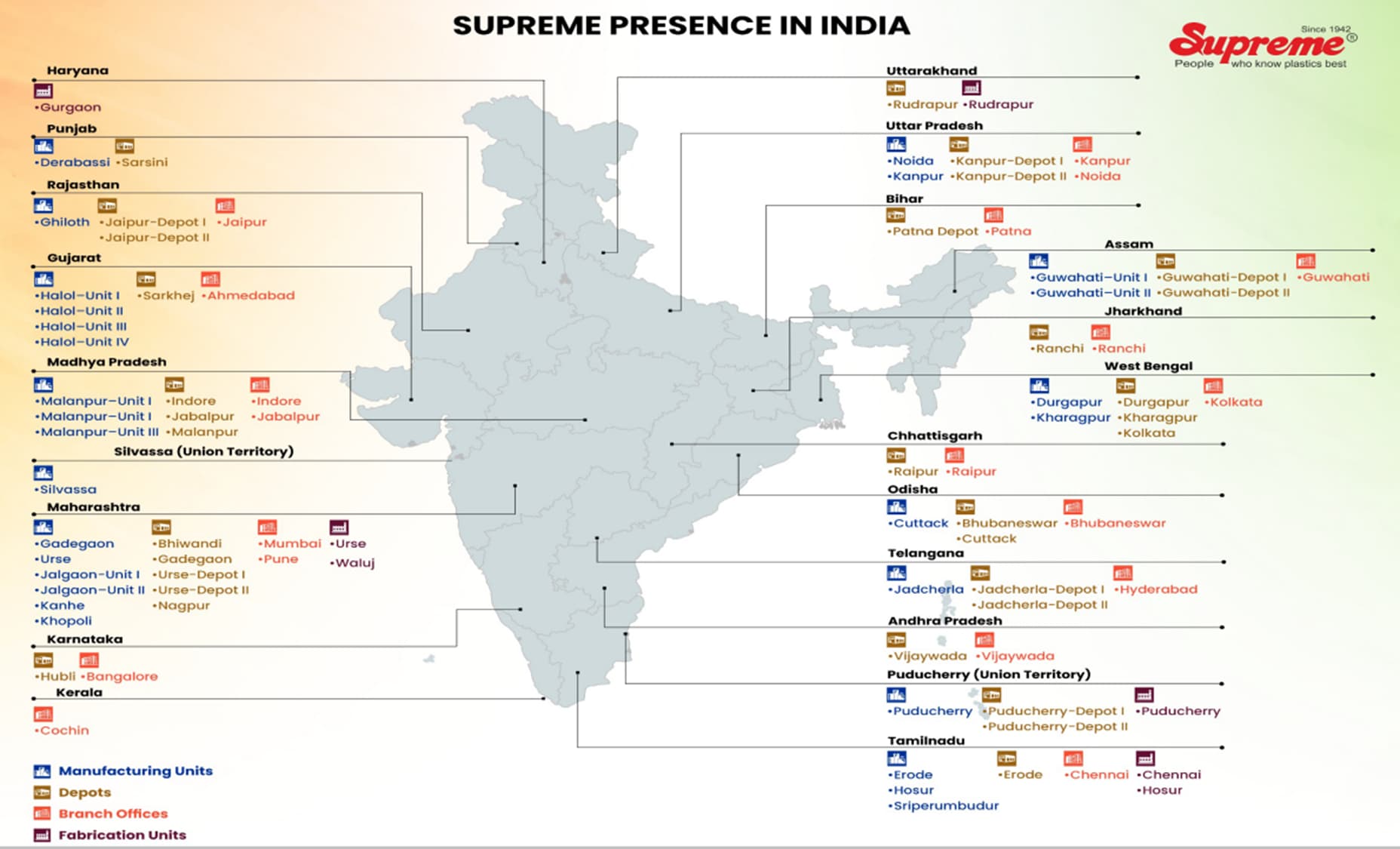

This is a peaceful company to own. With well diversified manufacturing facilities, distributors & products. The company has a leadership position in all the segments it operates & running more than 20 manufacturing facilities across Country.

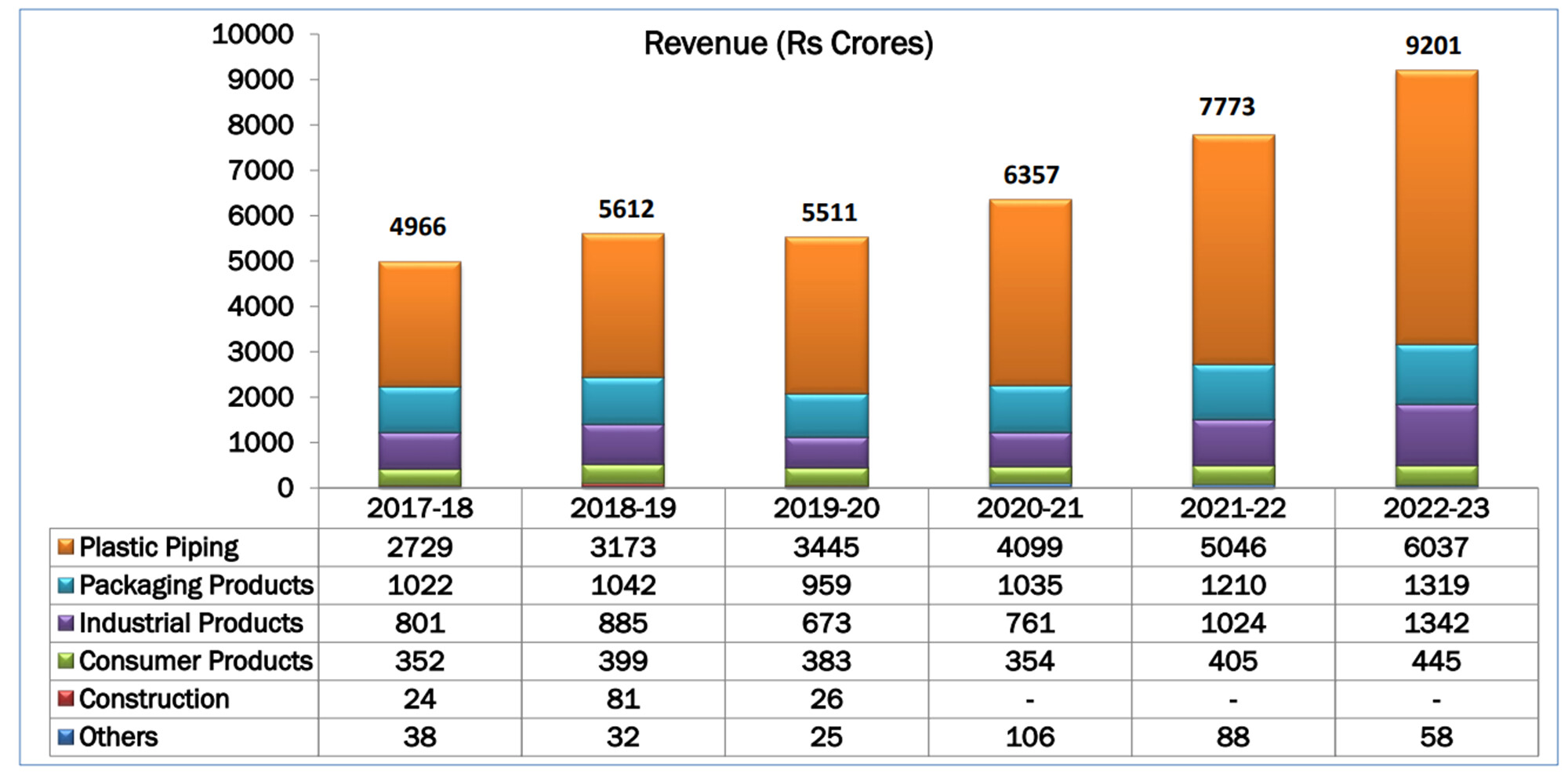

Below are the segments its operates & revenue contribution –

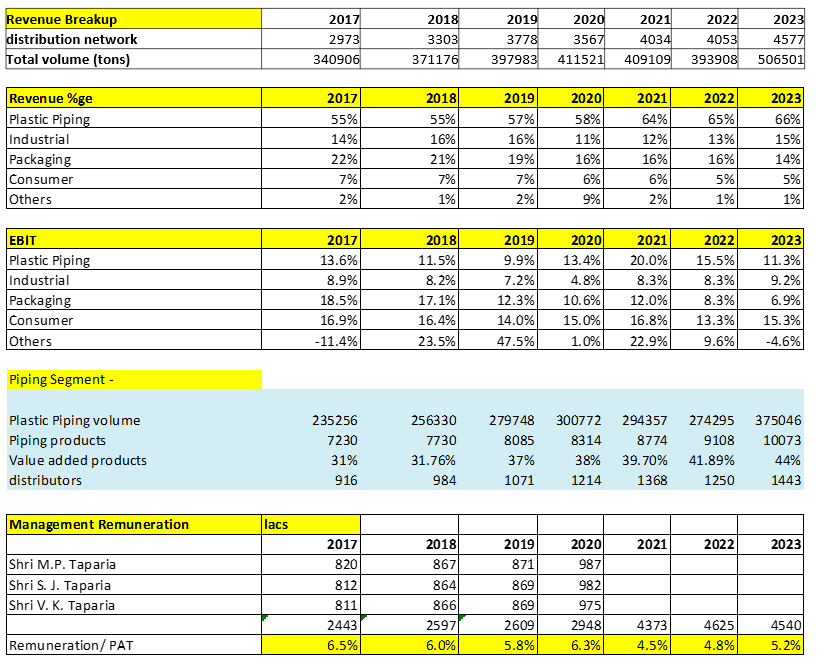

Plastic Piping (66%)

Consumer Products (5%)

Packaging Products (14%)

Industrial Products (15%)

Others (1%)

This company is a typical example of how great companies remain great. (81 years in business).

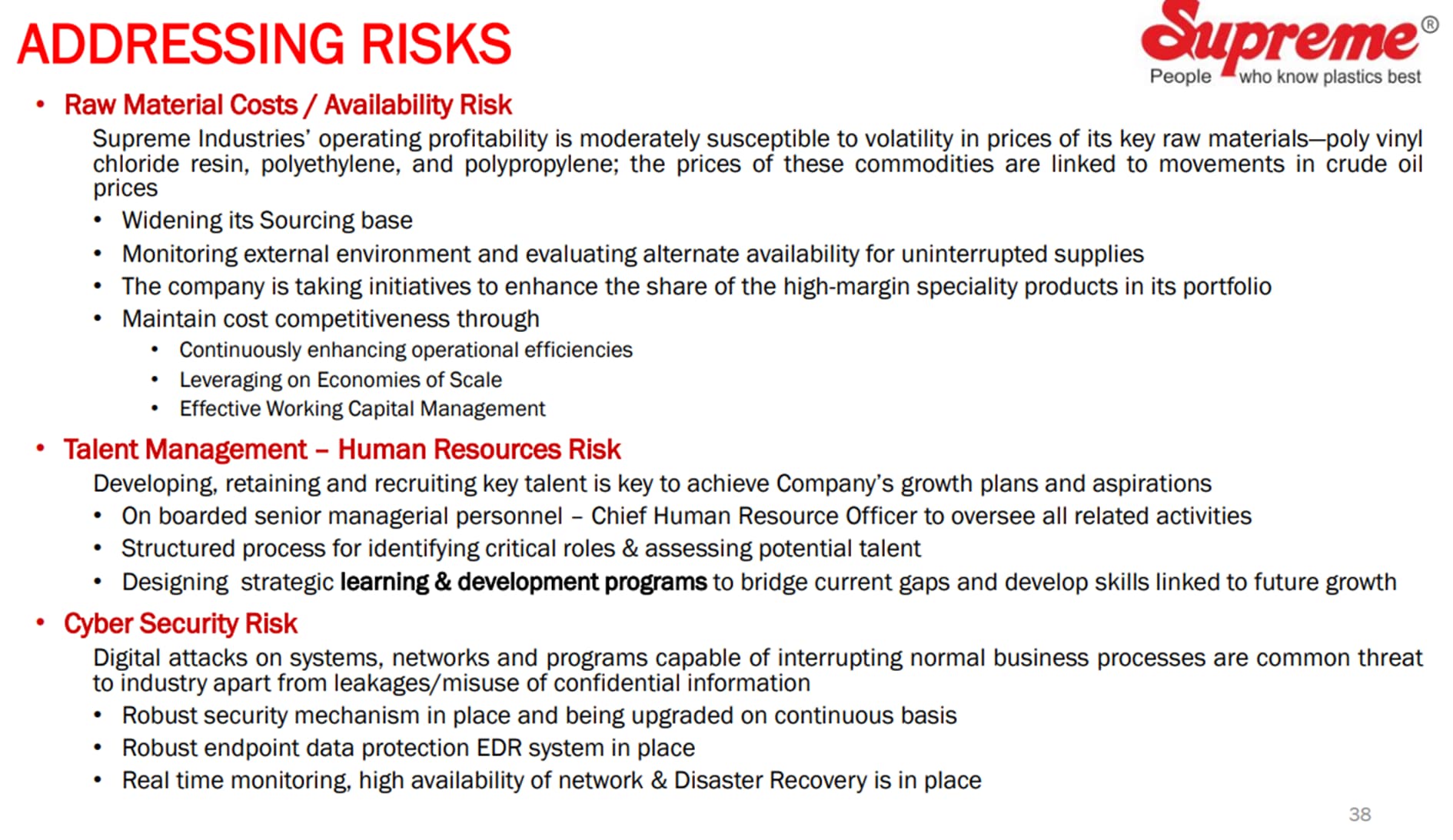

However, the most concerning things abouts this company are 1) no clarity on Management Succession plan 2) volatility of raw materials.

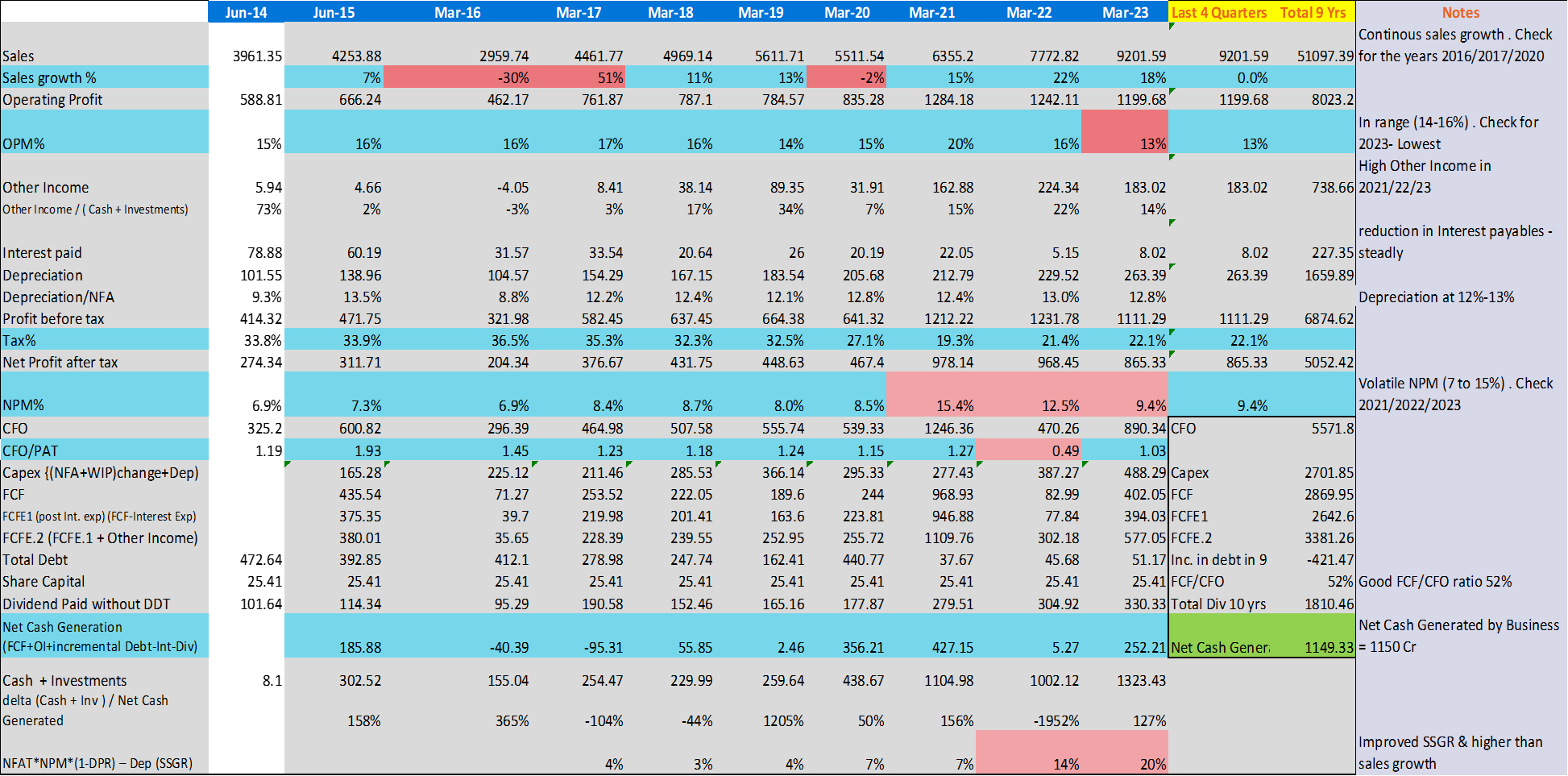

Financial Analysis Summary –

Balance Sheet looks good at high level – Funds are generated using profits & used for Net Block, debt reduction, Cash balance, Investments.

Outflow to Inventory and Receivables is in-line with the sales growth

Other liabilities increased due to increase in trades receivables

Dividend issued is always ~35% of PAT

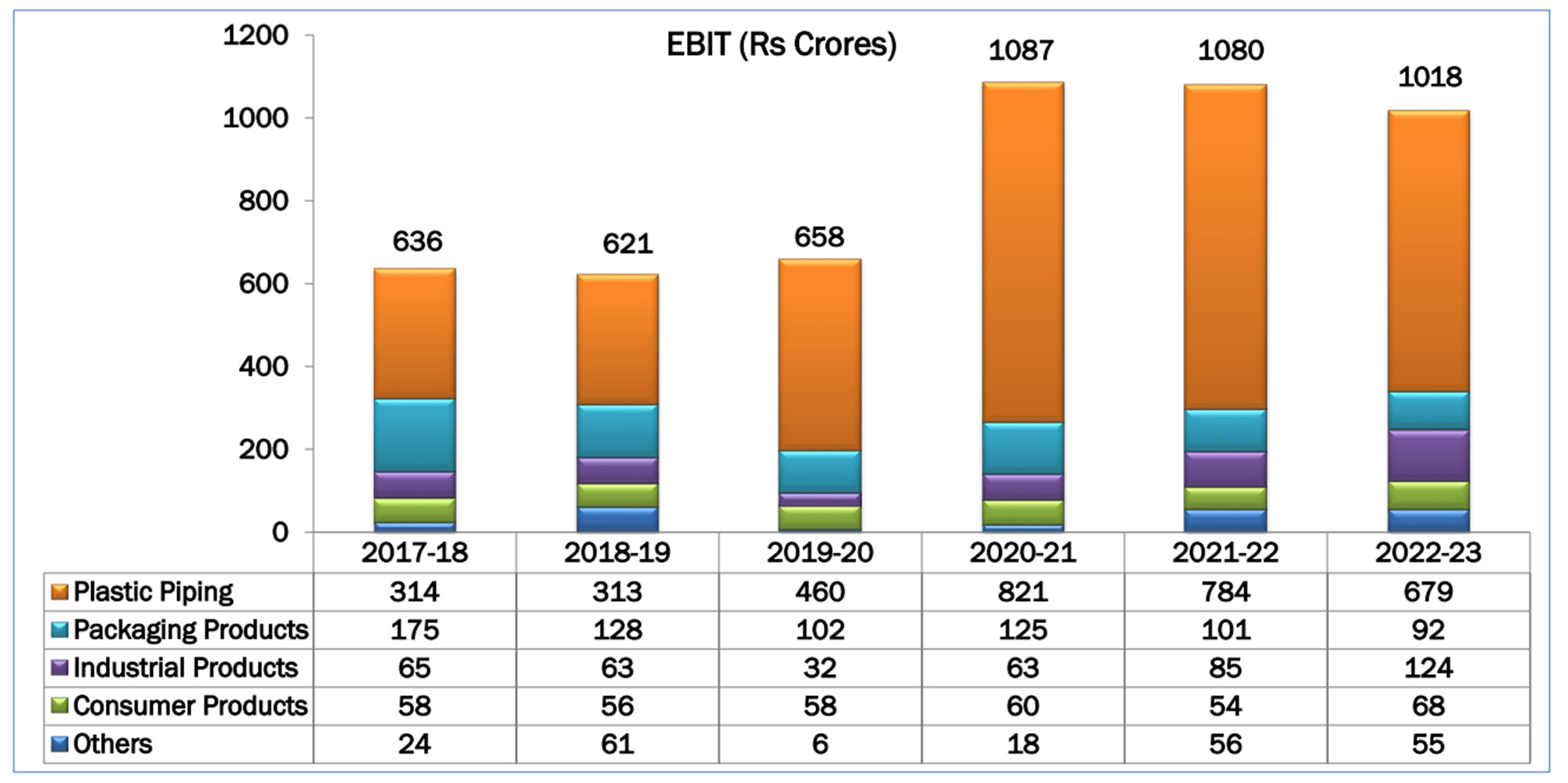

Continuous sales growth with range bounded OPM% (14-16) (check 2016/17/20)

High Other income in the recent years

Volatile NPM% (7 to 15%), check 2021/22/23

Good FCF/CFO ratio

Improved SSGR & higher than sales growth

Net Cash Generated / CFO is 20%

Depreciation 12-13 (in range)

Stable operations ratios

Controlled/Low debt

High return ratios (check for 2016)

Costs under control – Fluctuation raw material costs

In addition, an investor notices that until FY2015, the company used to follow a financial year from July to June. In FY2016, the company changed its financial year to end in March. As a result, in FY2016, the company covered only 9 months i.e. from July 2015 to March 2016. Therefore, all the financial data for FY2016 comprises the performance of only 9 months. In the years before FY2016 and FY2017 onwards, the reported performance is for 12 months.

| Subscribe To Our Free Newsletter |