Some key observations since the Flipkart Deal and why I feel the company deserves to be looked at again now:

-

Revenue for FY 23 : 1036 Cr up 67% YOY with latest Quarters showing much higher % growth YOY and QOQ. Company is on a run rate of 1200 Cr+ FY 24 without opening any new Warehouses.

-

Company has a total plan of building 20 Warehouses and has opened 7(4 last FY).

-

Since the B2C biz is now an Associate Company the GMs and the EBITDA margins are in much better shape although EBITDA is still negative. Wholesale biz are a function of Volumes and Operating leverage would play out with more Warehouses and lower discounts(more on this later).

Flipkart Health+:

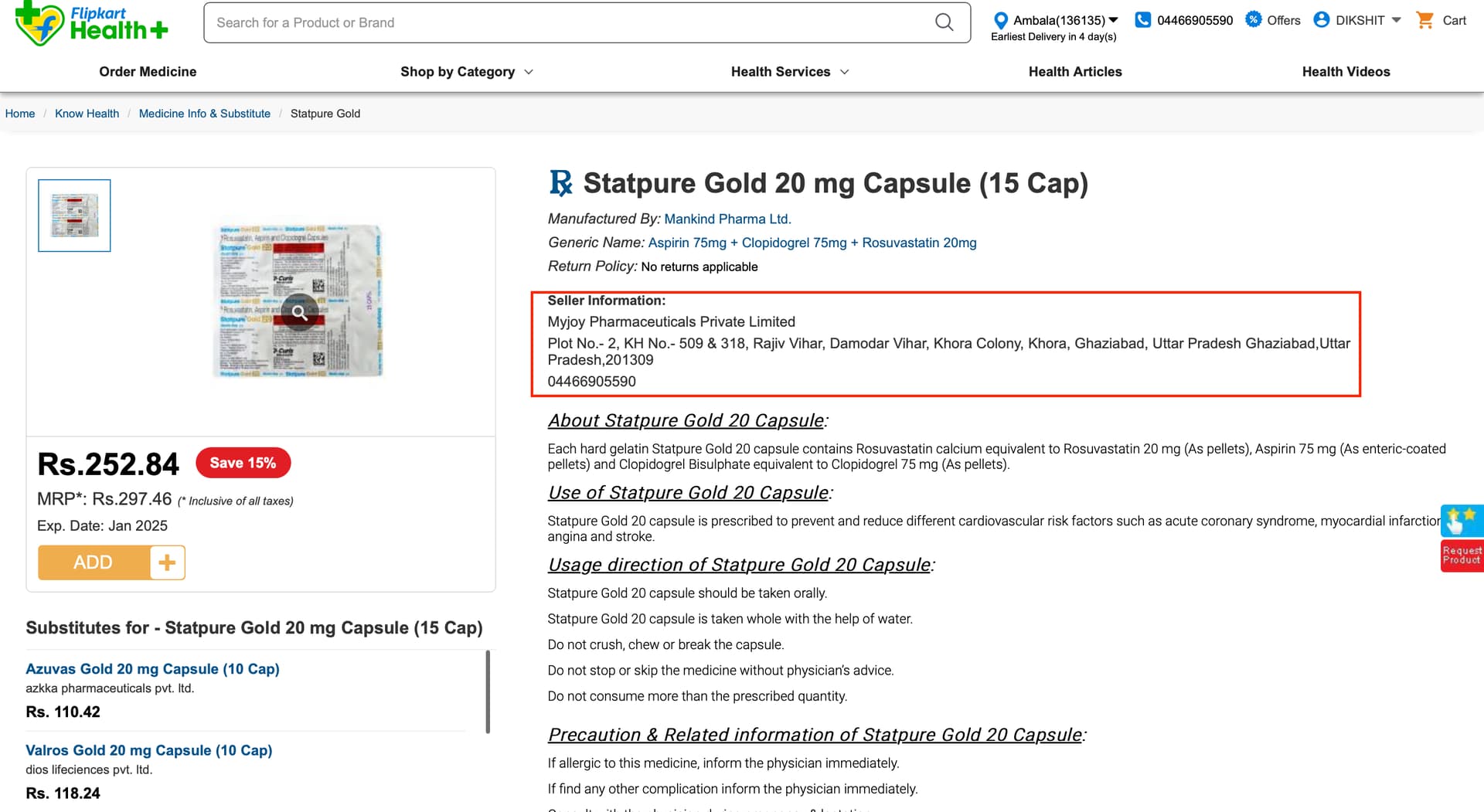

The Company has a double growth engine since the Flipkart deal in my opinion. For most medicines being sold on Health+ platform Myjoy Pharmaceuticals is the Seller which is a Subsidiary of SVL.

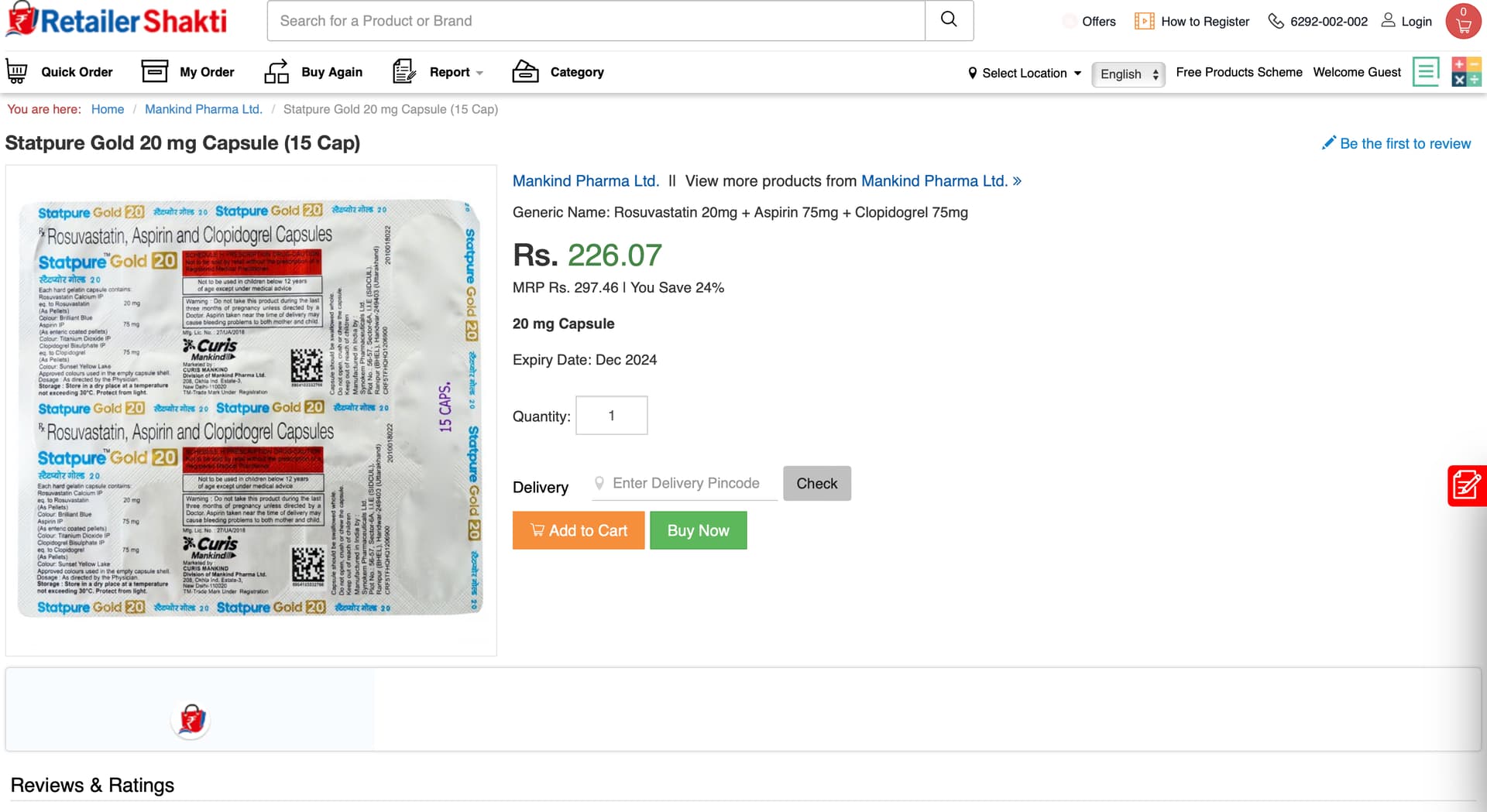

The Wholesale platform(Retailer Shakti) buys medicines in Bulk directly from Pharma Companies and then further sells the medicines on B2C platform via Myjoy thus pocketing the margins at both levels and enjoying the growth, fulfilment, reach & customer trust capabilities of the Flipkart brand ex the Platform Cost that Flipkart would be charging them. This could be a big enabler in their 97% YOY growth in Q4 FY23 other than the growth from the B2B retailer platform. Labs biz is most likely not this huge for them.

Yet to verify this with complete certainty as financials for the subsidiaries for FY23 aren’t updated on the website yet.

The price for the same medicine on the Wholesale platform is attached below and the margin difference for Myjoy comes to around ~ 11.5% ex Platform fees of Flipkart. This is also ex the margin of their Wholesale biz. For FY22 their Wholesale Biz did 4% GM, impact of any Operating leverage playing out has to be seen for FY 23. Myjoy had no sales in FY22.

Retailer Shakti B2B Retailer:

A simple google research reveals no large Competitor in the B2B Medicine space and seems like the initial mover will have the biggest market share since the entire country is up for taking. Sastasundar is already the biggest Pharma distributor in West Bengal with a 7% market share. They’re yet to open 13 more Warehouses in India.

The mobile web UI for Health+ is also much cleaner now than before and most likely Flipkart will revamp the Desktop web in sometime as well.

SEO is a key area where the Health+ platform lags with most search results from Health+ on Page 2 of Google search. The reason I’m highlighting Health+ isn’t from a 25% stake view point but from the Customer growth leading to growth in the Wholesale Procurement business and the combined leverage thereof including the growth in the Retailer B2B business.

Company still has a comfortable Cash position of ~ 700 Cr including Minority share which is going to be reverse merged soon and will simplify the Corporate structure.

At a P/BV ~ 1 pre/post proposed restructuring and a cash position of 0.6 BV including a 25% stake in Flipkart Health+ demands a relook given the huge market opportunity but comes with a big regulatory risk.

Yet to do a thorough valuation, will post once done.

Risks:

Pending Government regulation on e-sale of drugs – India’s latest draft bill proposes strict curbs on online sale of drugs, dealing a major blow to e-pharmacies

The nature of their agreement with the B2C platform is still unclear. Flipkart onboarding multiple vendors is also a risk. I’ve asked the Investor relations for more clarity on their relationship with Flipkart and any exclusive agreements.

| Subscribe To Our Free Newsletter |