Hi everybody,

The results are not how exactly I expected, there are new things which I am seeing.

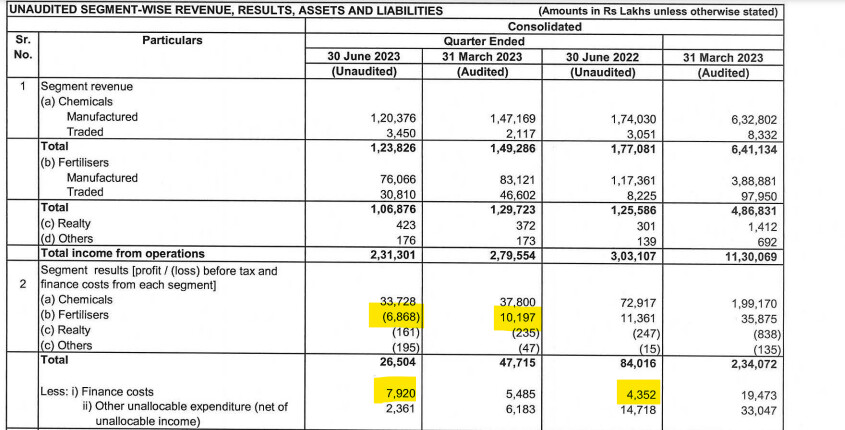

The fertilizer segment was totally unexpected,

we can see from a profit of 101cr in Q4FY23 to loss of 69cr in Q1FY24

-

They took a 161cr of hit

-

Finance cost is almost up by 90% YoY, I think this should still go higher in Q2

-

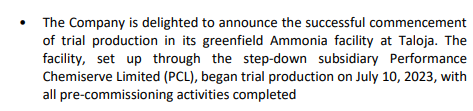

I cannot see depreciation increasing in this quarter. I think this is because their trial production started in JULY 10th so for next quarter we should see depreciation going up

This quarter dep is 59cr and last quarter it was 69cr . (this can go up by 20 to 25cr, just my guess)

-

Chemical segment profitability down by 54% YoY and 11% QoQ this is despite IPA doing extremely good. (I think IPA comes under chemical segment, please correct if wrong)

- TAN they are expecting volumes to decrease in Q2 due to monsoon and ammonia prices have further corrected form last quarter so Q2 TAN it looks like can be the worst.

Next quarter

- TAN volumes will go down, ammonia prices have further corrected

- Interest cost will go up, depreciation will go up

- IPA should be strong, fertilizer I have no idea.

Looks like next quarter PAT can be either in same lines as current quarter or even worse. Wafting for concall (if they would do) for better understanding. Overall if 500 is breached we are definitely seeing 400.

I am very much interested in this company and I think ammonia capex is going to be value accretive, waiting for the right time to enter where margin of safety is high. They only thing which is difficult to predict is weather all of this is already priced in or not.

Disc- tracking

| Subscribe To Our Free Newsletter |