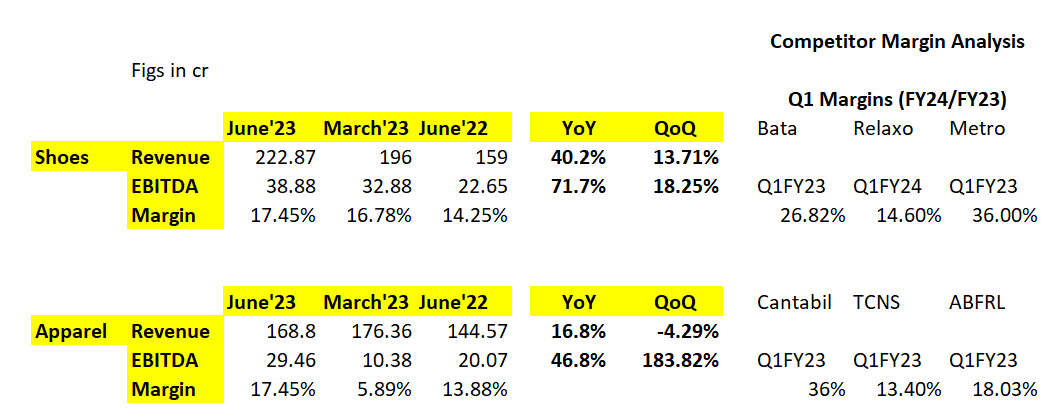

The margins of Mirza are slightly on the lower end. I did a comparison here:-

-

Supply chain optimization & omni channel initiatives (marketplace, own website, etc.) will really help them over the medium term. They get good traction on their insta page, but some of the usual tricks are missing (insta shop for example). These points will help them with incremental margin. Also brand building efforts – imp for mid / long term. Closely linked to success of any loyalty program.

-

Revenue growth in the shoe segment is fantastic. If you go to their product collection, the shoe collection design is really trendy, so I’m not surprised. Remains to be seen if they can sustain the demand traction.

-

Shoe segment margin comparison with Relaxo isn’t ideal. Their ASP is <200 while Metro has been trending towards the premium range lately. But goes to show that their is room for improvement here. In my view, scale will fix things by itself (better demand prediction, inventory insights, etc.)

-

Apparel growth is sluggish but will give them benefit of doubt since its a new adjecancy for them and they’re still in the learning phase.

D – Invested. 10% PF position approx.

| Subscribe To Our Free Newsletter |