HGINFRA,

Some info from their annual report…

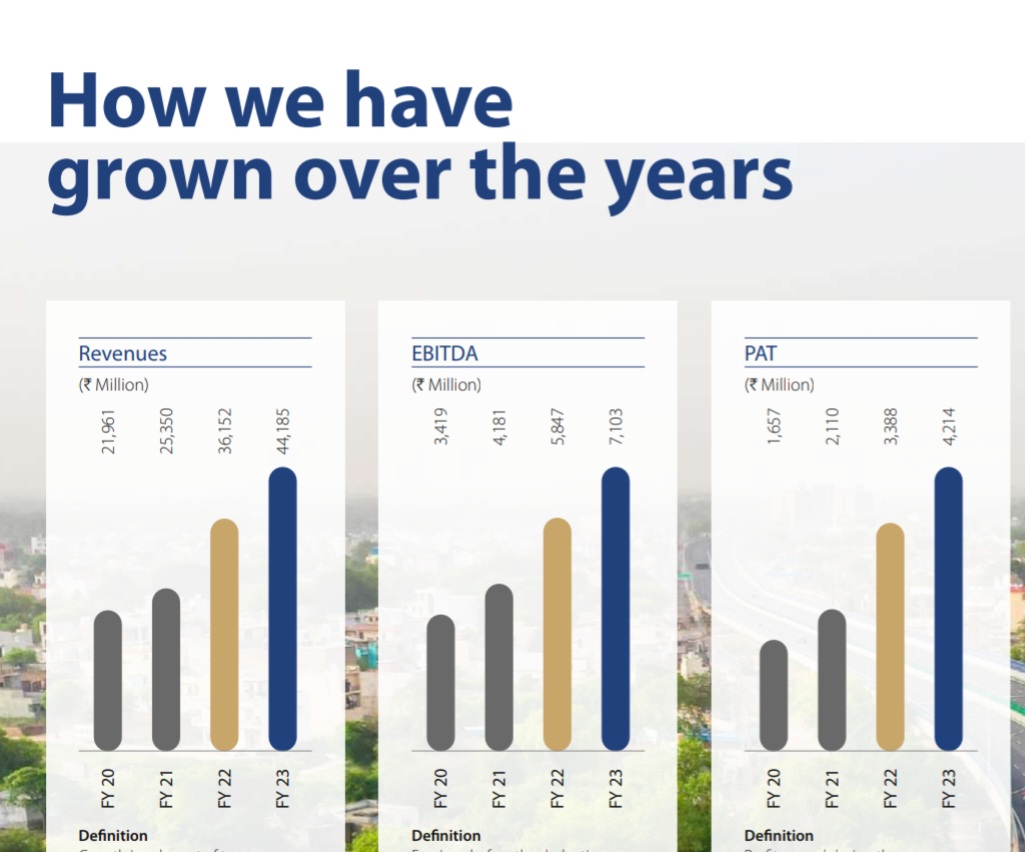

● Consistent rise in revenue/ PAT since last 4 years.

● Maintaining EBIDTA margin of 15-16%, RoCE of near 30%.

● Maintaining Low gearing ratio

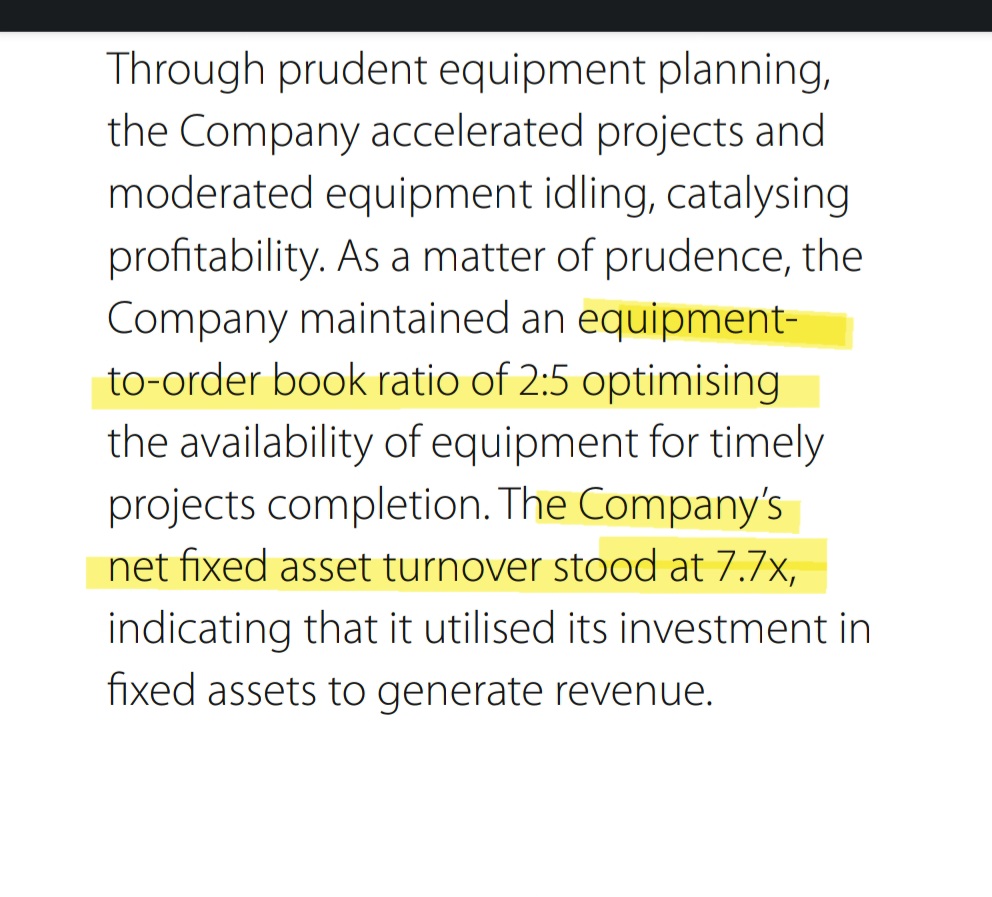

● Net fixed asset turnover at 7.7x

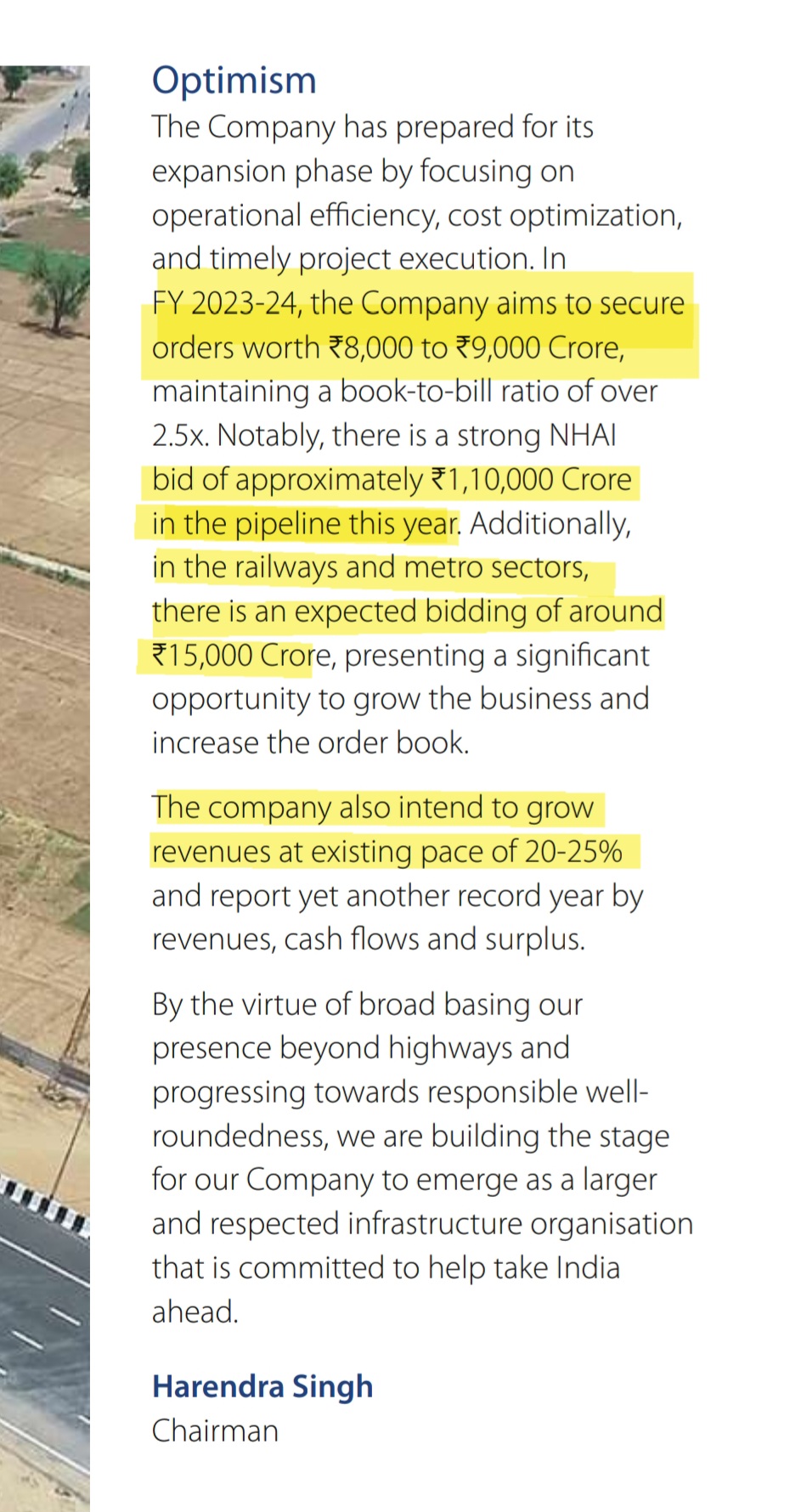

● Company aims to secure orderbook of 8-9k cr.

● Railway metros – expected bidding of 15k cr.,

● NHAI expected bid of 1.1 lac cr.

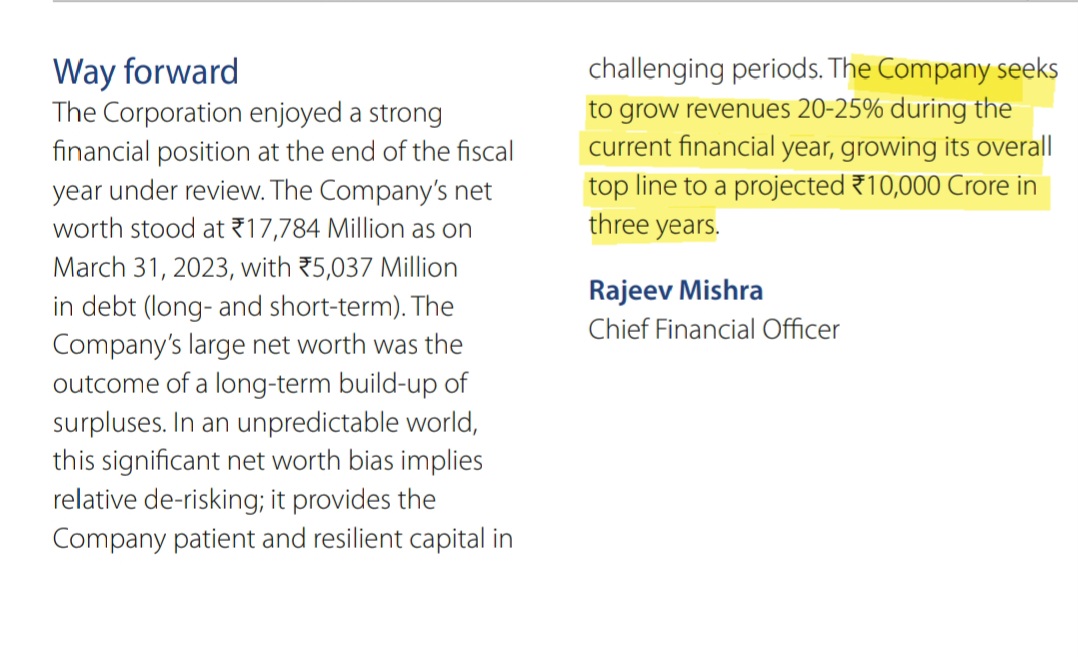

● Company seeks to grow revenue 20-25%, growing top line to 10k Cr. In 3 years time.

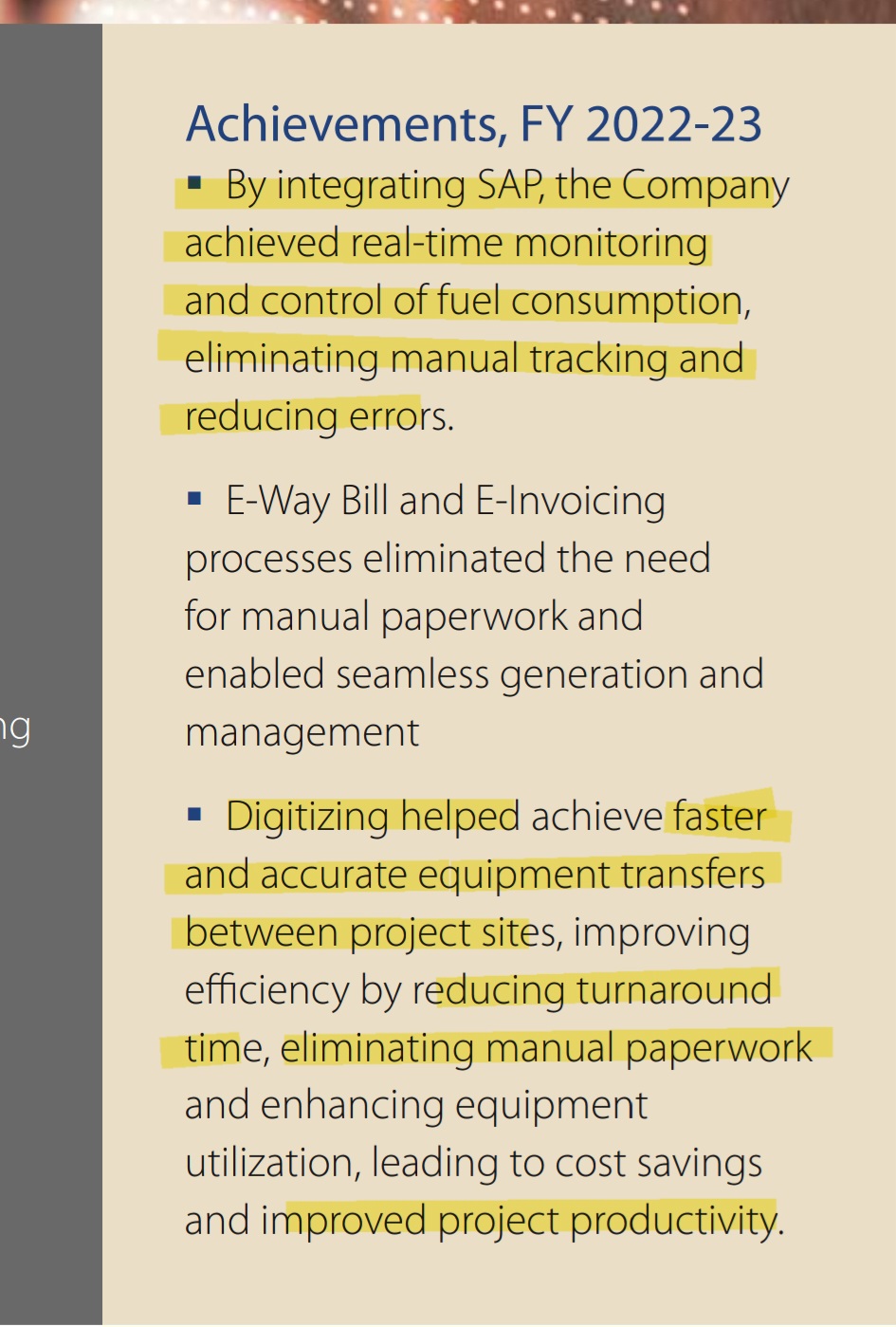

● SAP implementation completed. To improve productivity.

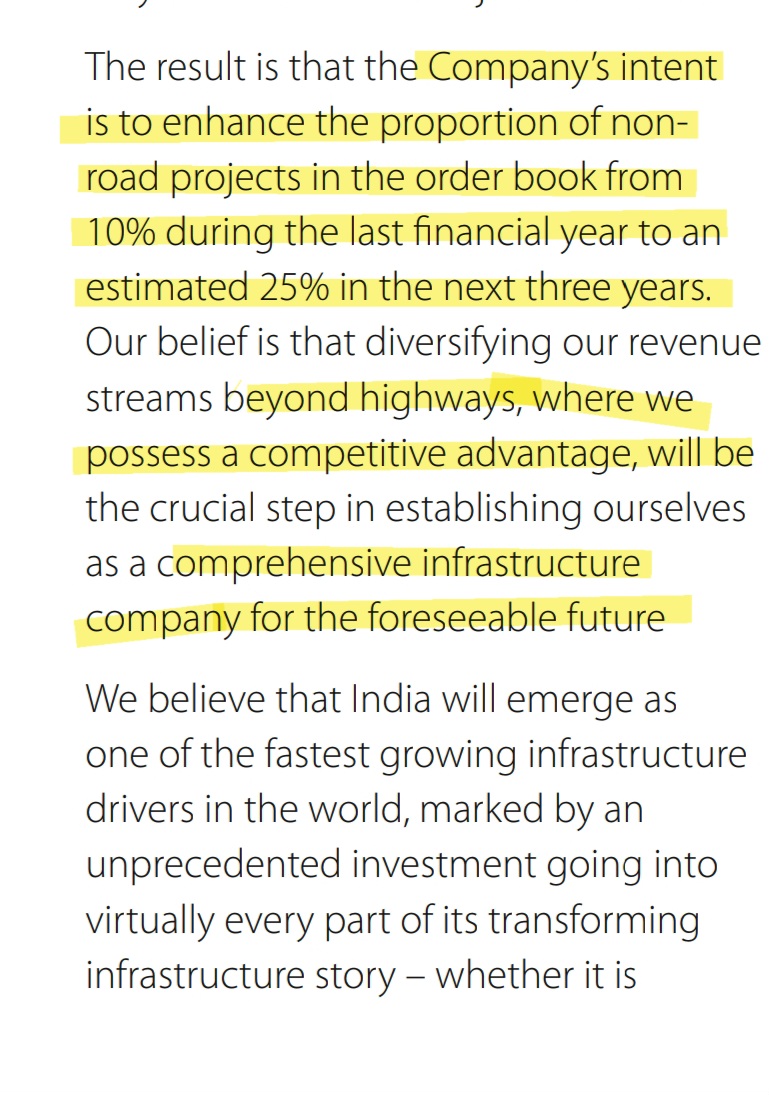

● Company aiming to increase it’s non road orderbook from existing 10% to 25% in next 3 years from railways, metro & Water resources.

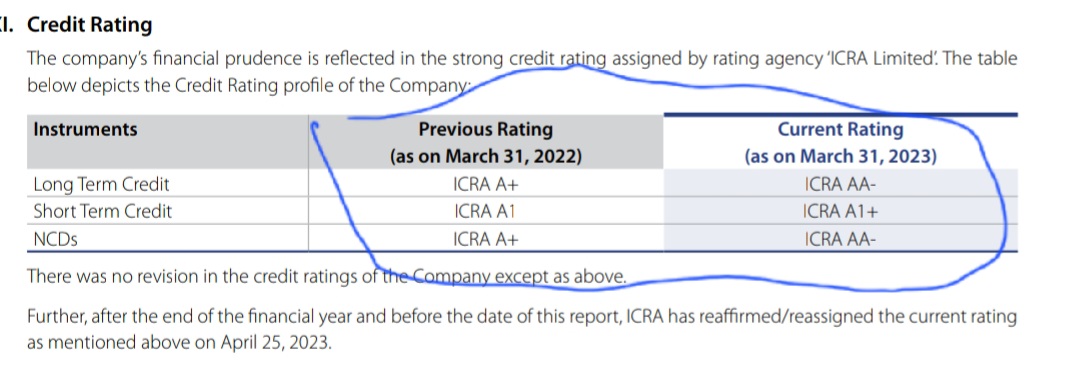

● Credit rating of the company improved during this FY.

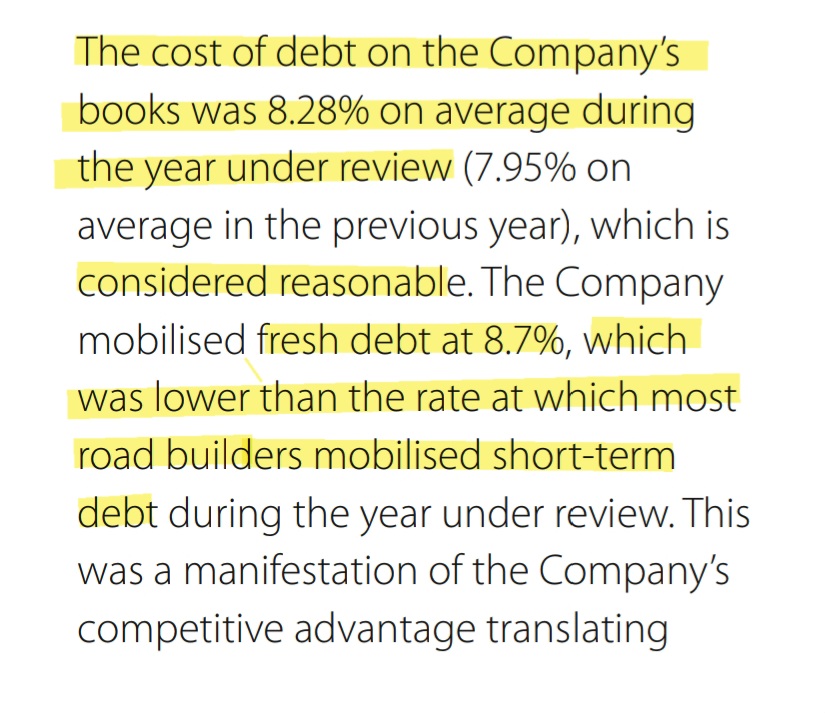

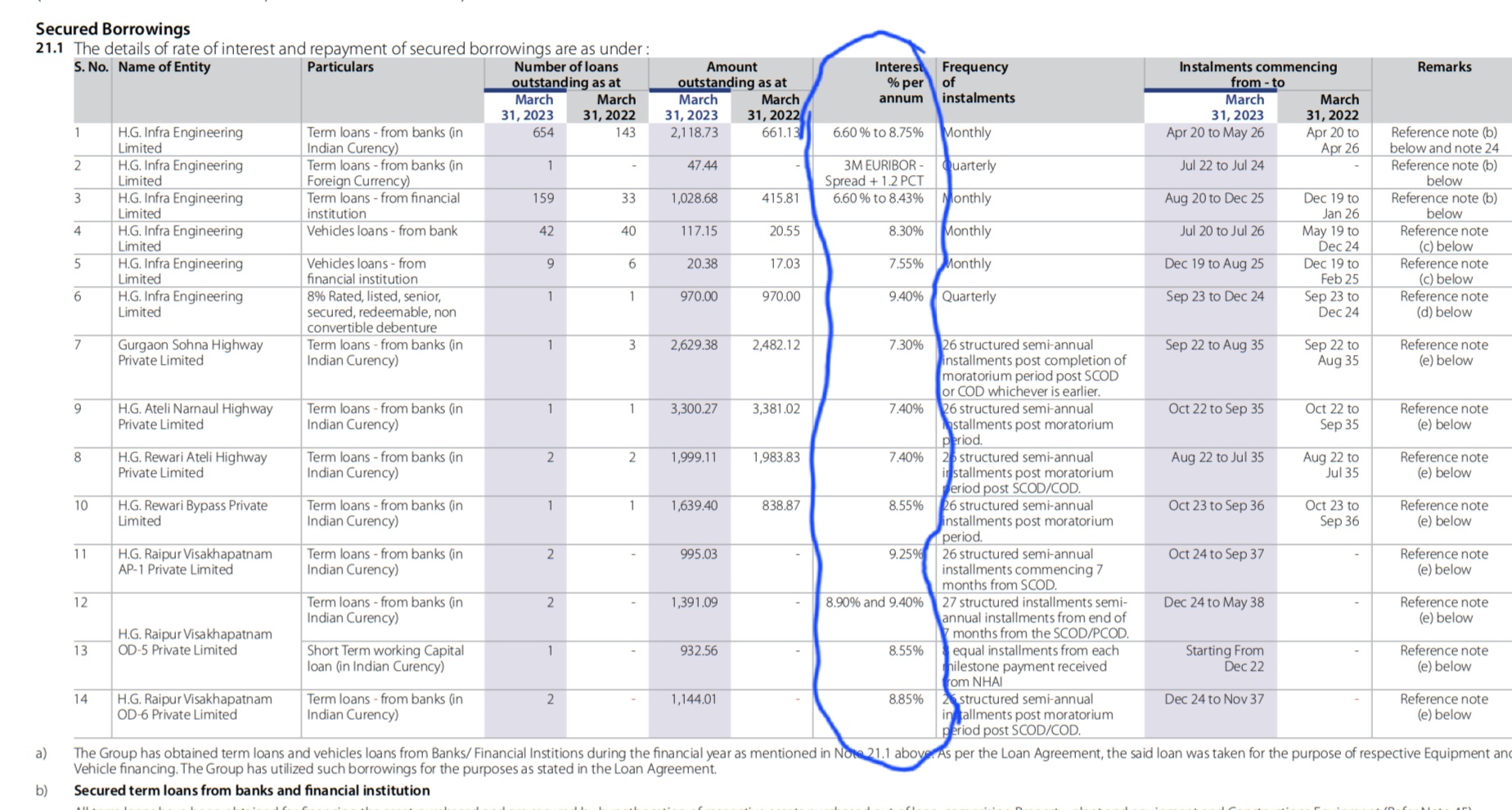

● Average Cost of debt was 8.28%,

● fresh short term debt at 8.7% one of the lowest in peer group…

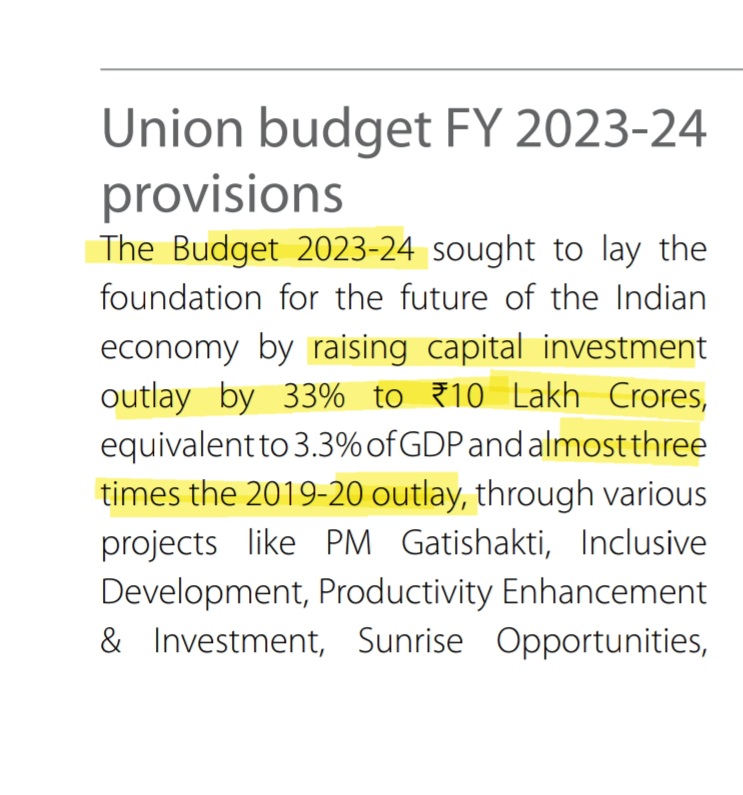

● Budget 23-24 – Raising capital investment outlay to 10 lac cr. – Almost 3 times of 2019-20 outlay.

● Road construction between 12k to 15k kms. ( 16-21% higher )

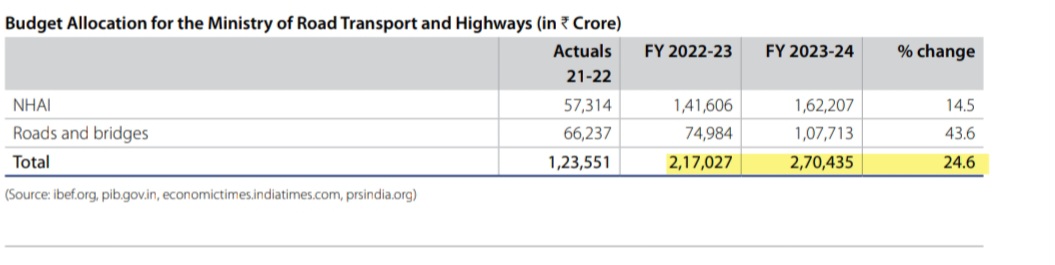

● Budget allocation: 2.7 lac cr. ( 24.6% higher )

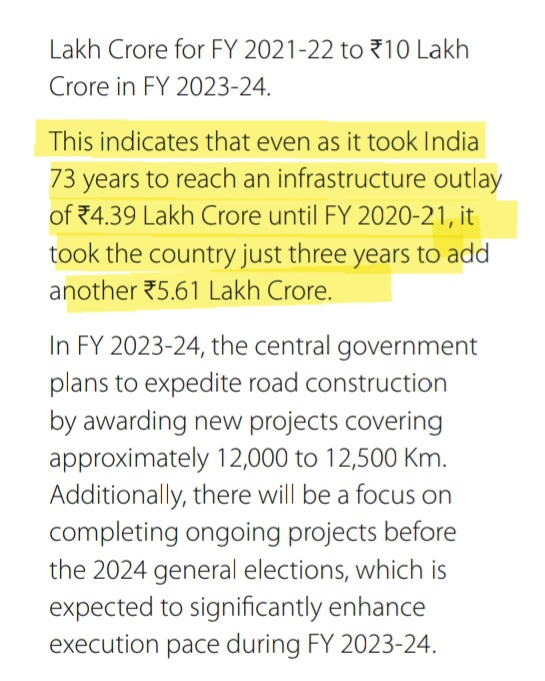

Infra outlay

In 2020-21 = 4.39 lakh cr.

In 23-24 = over 10 lakh cr.

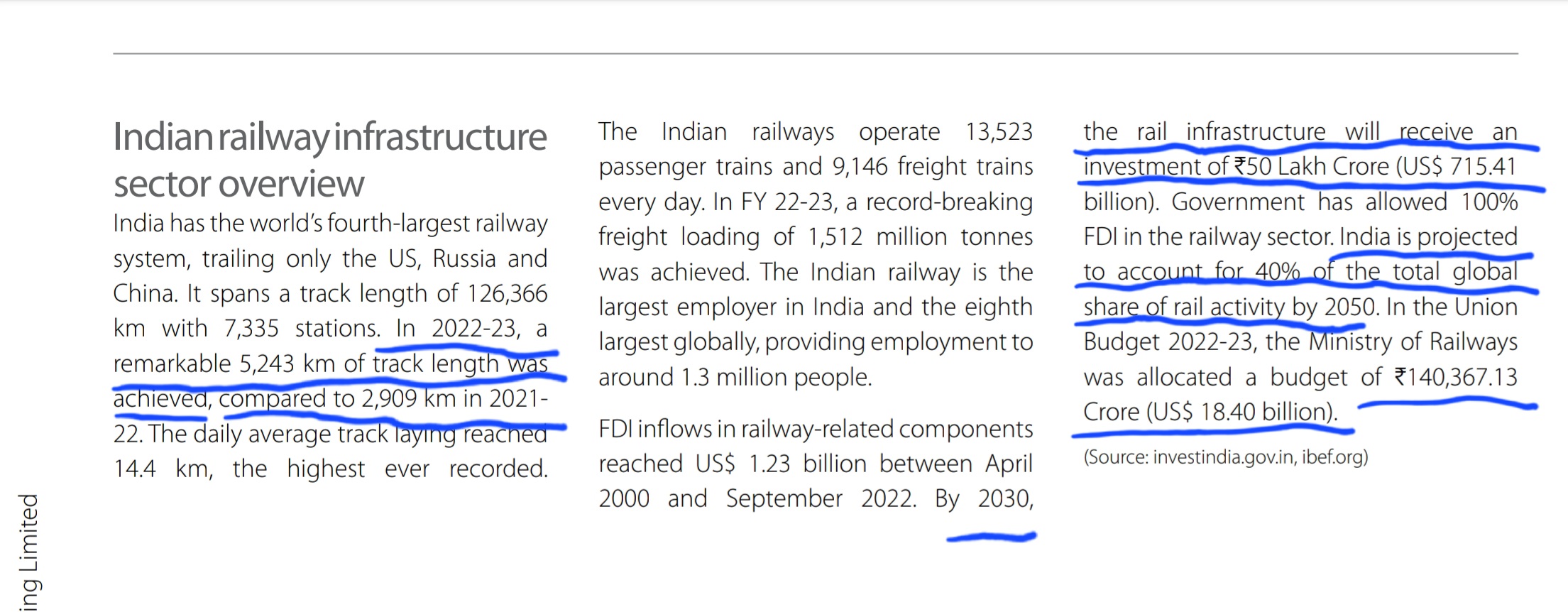

Indian rail infrastructure:

● To receive investment of 50 lakh Crore by 2030.

● 5243 km track length in ’23 vs 2909 km in ’22

● 140367 Cr. – Budget for ’23

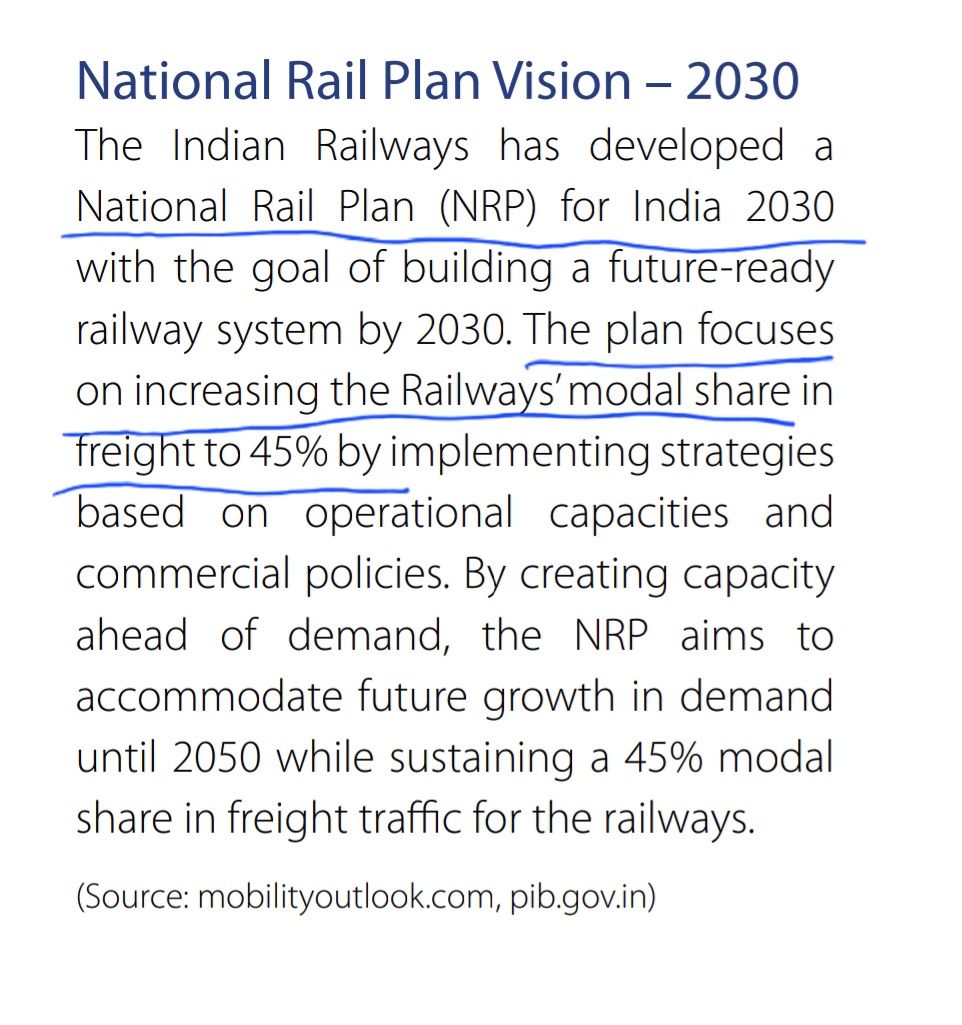

● NRP focuses on increasing railway model share in freight to 45%

Disc: Invested since early 2021.

| Subscribe To Our Free Newsletter |