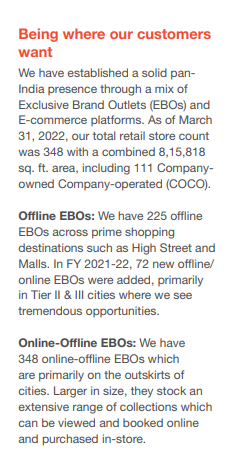

Hello everyone, I have been tracking this company and learning more about it from the detailed posts shared on this thread. Like most of us, I am excited about the growth in Redtape business. I, however, haven’t been able to reconcile the store-count related data shared across past annual reports. For example, the below section from FY2022 AR seems rather confusing to me. It says the total EBO store count is 348. It is then mentioned that number of offline EBOs in prime areas is 225 and finally number of online-offline stores (which are in outskirts) is 348! How can the total number of stores be equal to stores in the outskirts? How do we account for the rest of the 225 stores in prime city areas? Am I missing something very obvious here?

I have prepared a table containing the store count data in ARs of FY20, 21 and 22, and notice the same pattern.

| Number of stores | 2020 | 2021 | 2022 | 2023 |

|---|---|---|---|---|

| Total EBOs | 222 | 276 | 348 | 390 |

| offline EBOs (in prime locations) | 61 | 153 | 225 | |

| Online-offline EBOs (outside the cities) | 222 | 276 | 348 | |

| Shop in shop (or MBOs) | 830 | 246 | 245 | |

| Revenue from EBOs (In Rs. Cr) | 371 | 462 | 798 | |

| MBOs | 83.9 | 0 | 0 | |

| Ecommerce | 212 | 207.9 | 283.9 | |

| Total | 666.9 | 669.9 | 1081.9 |

Further, I notice that while each AR highlights the company’s MBO presence, there is no revenue being ascribed to this channel FY21 onwards.

Separately, Redtape Limited’s FY23 and Q1-24 numbers look impressive on the growth front. I observe that it has inherited a manufacturing facility from the erstwhile parent and has even undertaken a significant amount of capex (163 cr) in FY23, which is visible in the cash flow statement. It seems these funds have gone towards enhancing manufacturing capacity (the details of CWIP mention unit-5 and unit-3), and presumably for development of new stores.

It will be interesting to know what proportion of the stores are owned by the company, whose real estate would be on the company’s balance sheet (FY22 AR says 111 stores are company owned and company operated). It will also be nice if the management can share more details on arrangement with franchise operators (deposits from franchisees seems to continue to grow with FY23 number at 122 Cr).

Finally, the balance sheet looks a little stretched on the working capital side, with inventory growing by over 50% and trade payables growing by over 100% (March 31, 23 vs March 31, 22).

Clarity on these aspects can go a long way in helping investors build conviction on Redtape Limited. (esp. considering the past concerns)

Disc: Invested just before the demerger, but interested in increasing my position size in Redtape Limited

| Subscribe To Our Free Newsletter |