I am sharing my scuttlebutt analysis.

Current employees – 90 approx ( company staffs – 55 , contract staffs – 35)

new capex is for heavy packaging products. ultra high tensile strapping has 35% market in india which means new capex product has 350 crores to 500 crores business availability in india.

At present final output quality is 99.50%. Management is wants to try new grade chemical steel as a raw material. If it is working means quality rate jumps into 99.99%. It means rejection rate could be zero.

Management is not compensating with product quality. Even if the raw material price sometimes up they always wants to stick with quality raw material.

They have the production capacity of super jumbo coils 500 kgs. But their competitor GRIP has only upto 100 kgs. No info about signode india.

At present signode india is majorly focusing on packaging solutions only. No competitor is focusing on steel straps manufacturing business.

All competitor production lines are 20 to 30 years old lines. If they want to compete with krishca pricing then they need to change whole production line.

Raw material procurement

Krishca is procuring some raw material from chennai. They also procuring from bellari karnataka, west bengal too.

If I am going to supply steel straps to jsw or tata kind of companies they will insist to purchase raw material from them. If i am not purchasing raw materials from them then they will delay payments upto 90 days. if i am purchasing raw materials from them then the payments will be released within 30 to 60 days. These are non verbal agreement. (Disclaimer – these statement may be true or not. I am just sharing what i heard. Only for educational purpose).

Raw materials from jsw or other big corporates are placed on 100% advance payment only. Before placing order krishca needs to give 30% to 40% amount. After placing orders they need to settle remaining amount. Then only they will release the raw materials.

I am seeing this as a biggest moat as well as biggest drawback for krishca. Because if new player coming means he needs to put up so much money in raw material and inventory. Working capital could be huge if he needs to scale up the business. For krishca also these could be somewhat dragging. Their cashflow could be impacted. Need to watch how krishca here after going to manage working capital when they increase the production.

For signode india and grip their employee cost is around 7%. Most of their employees are aged above 30 plus. Their salary also above 3 to 4 lakhs. most of them may be joined with labour unions. so even if signode wants to fire the employees and wants to automise the production it could be somewhat difficult. But for krishca they are aiming to minimise employee cost 1.5 to 2% going forward. Their contract employess salaries in the level of 1.5 lakh per annum.

For shipping they are spending 6 to 7rs per ton per km if they wants to ship odisha or jharkhand or west bengal. But for their competitors it could take only 4 to 5rs per ton per km. Krishca is tackling this shipping cost with their employee cost. Also they made some long term arrangements with some transport companies.

Based on the above image we can clearly see that chennai to karnataka is only low distance. In vijayanagar jsw plant is located.

Their competitors also procuring raw ametrial from karnataka and west bengal. If signode or grip want to export then they need to transport to Vizag port. High distance for them. Where as for krishca its only 40km distance.

In gulf heavy competion from china and south korea. Krishca is going tackle this with one stop solution to their customers. They have plans to supply packaging instruments, employees, steel straps. By this way they are believing they could crack in gulf market. At present they are mostly supplying in gulf to small or unorganised players.

In packaging business they got something in west bengal. But the order size is unknown. Going forward if krishca wants to increase the revenue then they need strong presence in packaging business. Because packaging business requires less working capital and also long term revenue opportunities. But at present everyone is focusing on packaging business so i suspect how krishca wins here.

Top Steel Production state wise and capacity

Kindly note down below table data’s are based on FY2020 – 2021. As of now the production level is 126 million tonnes, increased 20% compared to 2021 volume. The capacity is also increased from 144 million tonnes to 154 million tonnes.

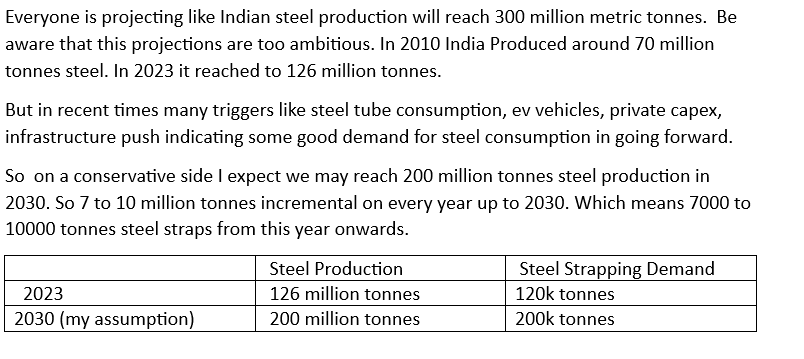

Future incremental Demand for steel straps in India

As per Management statement current overall steel strap consumption in India is 9000 – 11000 Tonne per month. For Conservative purpose we can take it 10000 tonnes per month. So yearly basis it will come around 120000 tonnes. Current Indian Crude steel production is 120 million tonnes approx…

So roughly 1 Tonne steel strap is used for 1000 Tonne crude steel production. (These are rough estimation only)…

New Welding Plant

Regarding welding business as far as i know market size is large. But if managements try to touch too many businesses at a time i might be worried.

PSU Business opportunity

In psu steel strapping i believe there is nice opportunity. Margin may be above 25% ( i don’t know exactly but assuming based on feedbacks). But receivable days is more than 120 in psu contracts.

Kindly share your feedback guys.

Disclaimer – These information collected from many people. So there could be something wrong or misplaced. Sharing it for only educational purpose

| Subscribe To Our Free Newsletter |