Tatva Chintan reported sales growth in June quarter and marginal improvement in operating margins. But its below the line items like depreciation ( related to higher capex) which are acting as a dampener on the results at net profit levels.

This company is a classic example of a hot stock in a hot sector. When chemical sector was the rage, this company was touted as a company with competitive edge, and entry barriers etc. These terms are very important to understand and apply. By themselves they are not a license to pay crazy valuations. And Tatva Chintan began its listing journey enjoying crazy valuations. When its valuations were at peak,

I guess peak market cap was around 6500 crores plus. And sales were a mere 400 crores. A lot of extrapolation was done about capex coming on stream by X number of years and sales figure being double that of the sales at that time. And then margins were also extrapolated based on management guidance. And based on that, a lot of experts predicted that at ABC valuations, it would be justified to buy this company.

As of now valuations have nearly halved ( still not there, but just about there. ) And still no clear light at the end of the tunnel. While it may be one of the better chemical companies with some kind of moat, or competitive advantage, the key take home learning for us is that it was a ” Hot stock in a hot sector” … A classical example of what Lynch preaches in his book.

Maximum money is made when a company is bought at cheap (read commodity type company valuations) valuations, and it reports growth and profits that are expected from a speciality or niche company. Majority of the money is made from re rating, and the other big chunk from actual growth.

Now apply exactly reverse logic to above paragraph. Imagine a company bought at 100 PE (according to screener this used to quote actually at 100 PE or close to it), delivering negligible growth, and swift contraction in valuations to sub 40 ( as seen during April 2023) . The key thing to note here is that even if the company starts delivering growth at a reasonable clip, one cannot expect valuations to reach levels of 100 PE…

The other tell tale sign was an extremely appealing IPO happening during sectoral fancy. One needs to beware of these kind of IPOs. We have seen this kind of history being repeated off and on … In 2006-2008 era it was infra and real estate companies. In the run up to 2015 pharma peak it was pharma companies. Nowadays its railways, defence, power etc. And these things will keep on repeating with old wine in new bottles.

So starting valuations matter a lot while evaluating a company. For a time being they do not matter in a hot sector and a hotter stock. But after market wearies of lacklustre results, prices tend to correct or go sidways. Either case the capital invested does not produce any return.

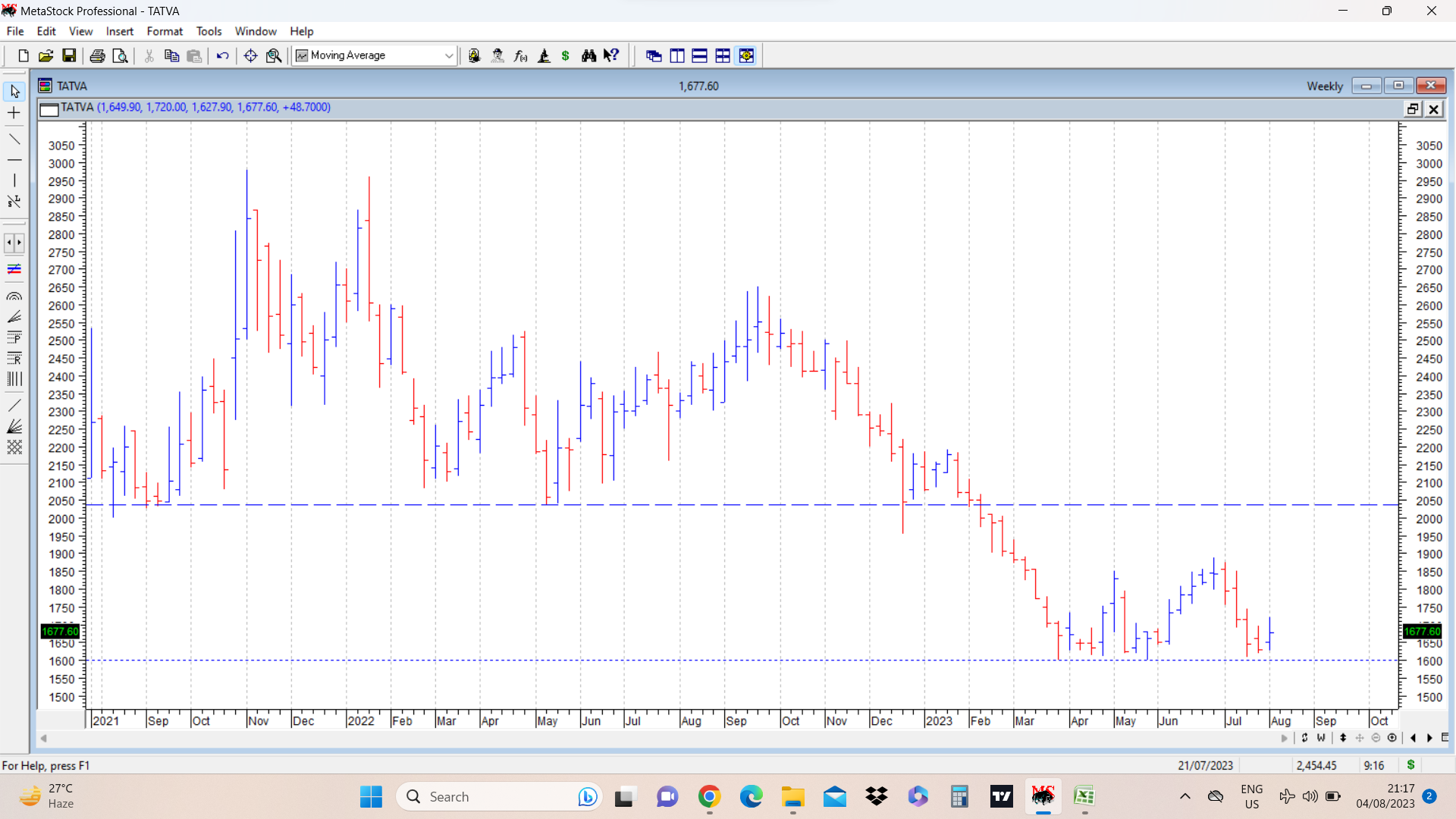

Attaching a simple chart where breach of post IPO lows was an indication to exit. That level was around 2000. After that stock price has not gone close to those breakdown levels. New next level to watch is level of 1600 or thereabouts. Just for record, stock listed on bourses in July 2021 and its more than 2 years since then. Folks who bought post IPO and listing, considering this as a company with moat etc are still sitting in losses and their capital has not produced anything for more than 2 years, and while a lot of other stocks have doubled or tripled or more.

| Subscribe To Our Free Newsletter |