Sandur’s Q1 results have been poor, highlighting a few important excerpts from the Investor PPT below:

- Mining segment

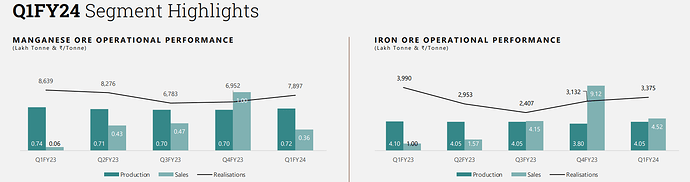

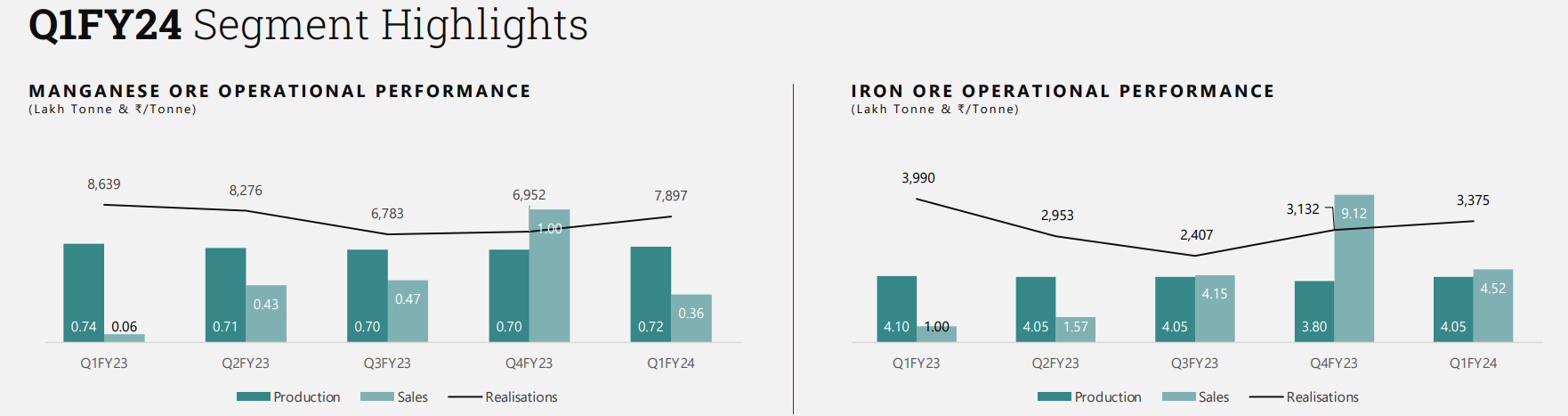

- Production of both Iron Ore and Manganese Ore mostly in-line with quarterly targets, although have some reserves of Manganese Ore left (broadly both are ~25% of annual capacity, so production seems fine)

- Prices of both seem to have rebounded compared to Q3 FY23 (attaching a snippet below for the realizations trend)

- Expansion – Based on the remaining approvals, expect to ramp up production for Mn Ore in Sept’23 and Iron Ore in Oct’23 (this is perhaps the most important part, since their effects should be partly visible in Q3FY24 and fully in Q4FY24)

- Once production ramps up, focus will shift to downstream operations – pellets and beneficiation

- Ferroalloys

- This has been one of the main party spoilers due to tepid demand, and while realizations have fallen 20%+ from Q1FY23, the production was quite low too. To put this into context, Sandur produced 11-15K ton each quarter in FY23 ( it has ~1.1L ton of annual capacity or ~25K quarterly capacity at 100% utilization), but only ~8K ton was produced in this quarter

- Sandur commissioned the renewable energy project with Renew in Jun’23, which will help in scale up once the demand environment is more conducive

- Coke

- Prices have fallen ~30% compared to Q1FY23, and 10-20% compared to the previous three quarters. Again, Sandur has optimized volumes here due to lower demand and low prices

Other-

- Submitted all necessary applications for listing on NSE, anticipate approval shortly

My personal opinion is that Sandur is not a QoQ or YoY story (and probably Coke and Ferroalloys are not even the most important segments), the key pointer in my thesis is the expansion in mining segment, especially Iron Ore. Just putting things into context, at current Iron Ore Prices of Rs 3.3K/ton, an incremental 2.9M ton (at 100% utilization) can add ~950cr topline with 45-55% margins i.e. 450cr+ EBITDA. The mining segment put together can add incremental 500cr+ EBITDA (even at 90% utilization), given that Sandur’s market cap is ~3300cr, it still looks lucrative.

Also, in my opinion the rights issue was not the best outcome for passive shareholders (and that has to be a key factor under ‘Risks’ in this play; maybe the Market won’t be in a hurry to give good valuations to such a business), but generally these things improve as the size of the company grows. And in no way, does this put a doubt on how good the management is (check what all they do for their employees, these guys are actually one of the good ones out there).

Disc: Same as before

| Subscribe To Our Free Newsletter |