@ChotuKatappa Recently started tracking Cipla story

Cipla is into respiratory, ipm, chronic and cardiac profile

Cipla is in rank 1 for respiratory and their strategy of ipm in India is playing out

They have strong foothold in South Africa

Next set of growth : peptide injectable, advair, grevlimid

My triggers for buy

Now as per the concall the management said the recent jump in revenues are due to price conditions and most of the American companies are closing their business due to losses or amalgamation of business with some other to survive.

Second as per multiple sources I heard of us generics market will not do well

It’s just that branded generics will do well in domestic front well Cipla is poised for it

Third opportunities like peptides, grevlimid

Fourth if you look at their ipm market it has substantial grown in chronic portfolio part

Fifth : Cipla’s lead peptide asset Lanreotide injection, launched in Q4FY22, is consistently gaining market share. The product currently has market share of 18%, up from 17% in Q4FY23, 14.1% in Q3FY23, and 9.6% in Q2FY23

Now why in such case promoter sells 33% stake

First reason as per the sources below the promoter doesn’t have children

Second why only sell to black stone only

I don’t know. We have to wait and find out from the management

If I were to think about it – I think big investors could only buyout such big stake now at what % discount don’t ask me…

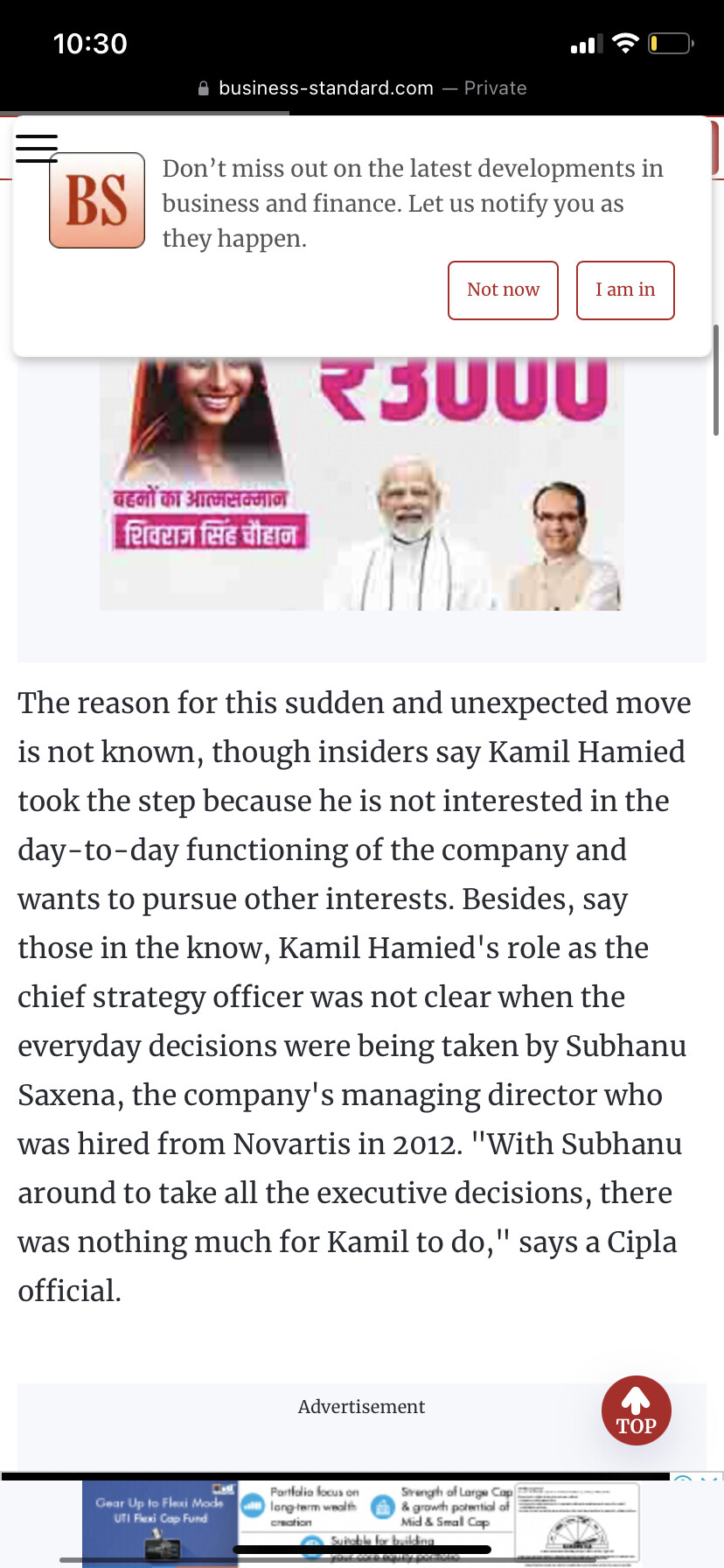

Yusuf hameid has Mk hameid too as vice chairman but he is retired on March 2014

Now mk hameid has 3 children among them

2 daughters

1 son

Seems like no one is interested !!

I further believe Cipla should do well and they are also exploring bio similar opportunities for respiratory side

@ChotuKatappa now can you drill down to check and tell me

how is the Blackstone management

Do they understand the pharma complexities

Did they ever manage pharma companies and if so did they likely succeed

| Subscribe To Our Free Newsletter |