Thanks for summary @avneesh , have done some cursory research post Q1 results, AR 22 has some interesting pointers, this year AR and AGM should thro more light.

- Co seem to be focused on some segments – key focus area – snapshot from AR 22

-

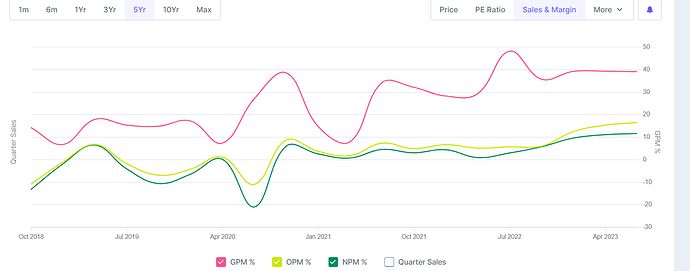

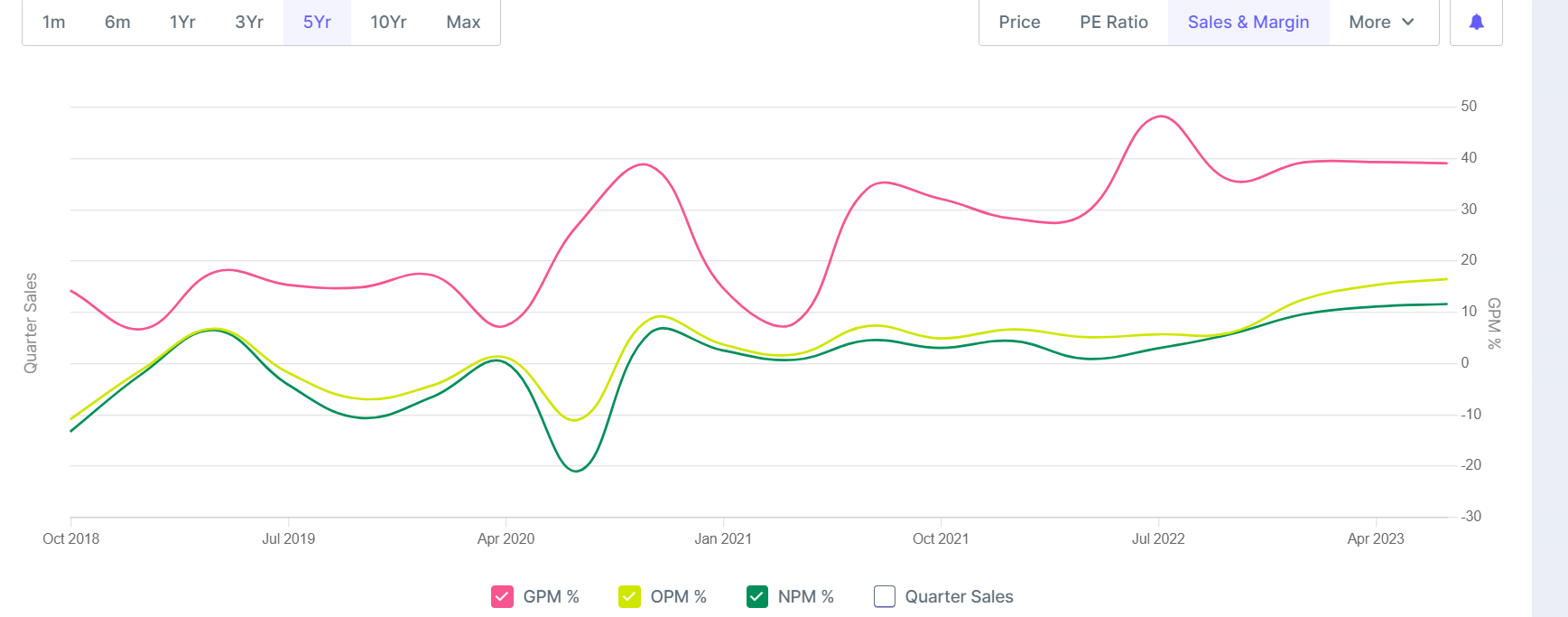

Margin trajectory is healthy post new promoters taking charge – GMs have expanded and trend seems healthy

-

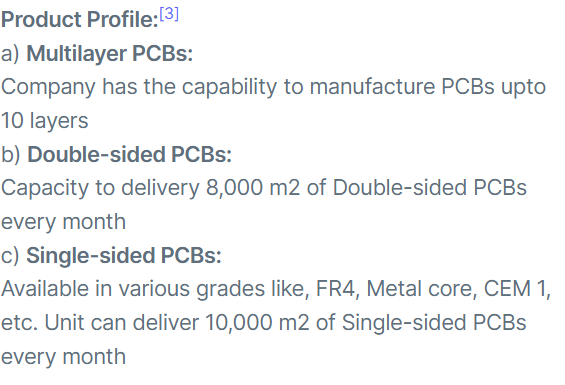

One can do google to understand realization difference between single layer vs double sided – comes to 3X range approx – indicates value addition (also validated in above post per Kayne notes)

here are current capacities – based on broad realization trends – company is making healthy margins at modest utilization (60% type broadly by very high level calcs ) – This is something that need more work as product mix may change margins a lot

-

One thing that stood out for me was UL certification per AR(there are other certificates as well) – now this may be based on Fuba global exposure and association – it could be a key asset/differentiator if co truly exploits it well going ahead

-

In some ways company potential ties to ESM rise + make in india push fortunes – explains good show in recent past vs longer history of no performance delivery, New promoter likely deserves some credit too.

-

On quick research it appears that many unlisted players are manufacturing PCB in india (YT has some videos) – however it is likely that broadly there will be min two categories – 1) mission critical apps – medical / auto/defense etc vs 2) consumer electronics/toys etc. Category 1) is where UL type certification+ sophisticated mfg infra + skills and complex products (double or multi layer) will come into play and serious players will choose this path.

-

PCB assembly is commodity and almost everyone seem to be doing it.

-

New promoters are increasing stake(Bharadwaj family), Old hands are exiting(past promoter + others) – explains large volumes and bulk deals – absorption by mkt says accumulation as well.

-

Copper clad plates etc as RM imports context (price + freight) seem to be helping now co (after playing reverse role in last year) – However margins pressure in FY 21/H1 FY 22 indicates pricing power may not be present and this needs validation.

There is lot to understand about company, however being a nano cap information may be tricky. Current phase of bull mkt makes it even more tricky where everything is roaring ![]() . If this story does play out as Electronic mfg proxy with some tech edge, should have a decent long runway and hopefully enough opportunities to ride.

. If this story does play out as Electronic mfg proxy with some tech edge, should have a decent long runway and hopefully enough opportunities to ride.

D – Hv small positions post Q1 nos, most of above are feelers/quick research data and could be off, pl apply own discretion.

| Subscribe To Our Free Newsletter |