Hi my name is Jaiprakash (JP) I am 42 years. I am an MBA with 17 years of experience in corporate world. My experience is mainly into credit ratings and investment research for global banks and corporate entities.

*Disclaimer: please note that I am not a financial advisor or nor a SEBI registered advisor or a research analyst. All the that I shared here is based on my personal opinion and my personal situation hence same may not apply to you. Please consult your own advisor before taking any action.

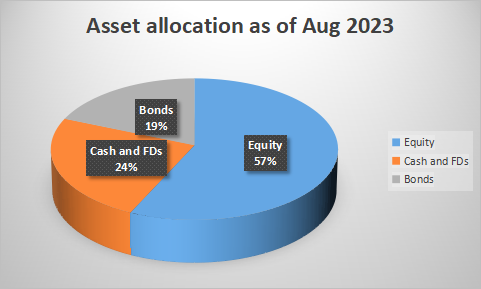

I have been investing directly into stocks since 2010 and I am reading valuepickr for a decade now. Until mid 2022 I was 90%+ invested in equities however, over the last one year I have increased my cash and bond holdings to 43%. The increased allocation of cash/bond holdings is reflection of my personal situation rather than having a market view. I have given below break-up of my current allocation to financial assets:

Keeping aside my personal situation, I believe bonds are good investments from 3 to 5 years perspective given that interest rates shall come down a year ahead and we might be able to reap benefit of capital appreciation. Some of the AA rated bonds are trading above 10% yield to maturity.

Equity investments:

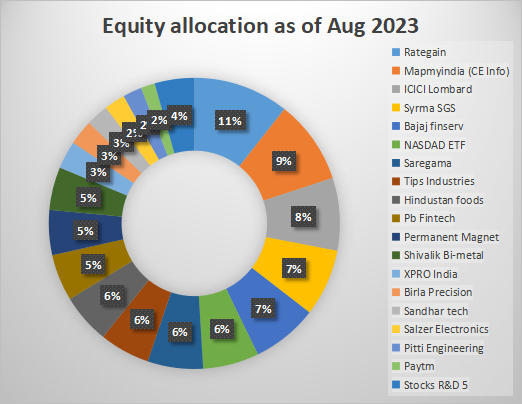

Below is break-up of my equity investment:

Rationale:

Rategain Travel Tech (11% of portfolio, 29% profit): My first entry in Rategain was at 370rs per share in December 2021. My average cost price is 362.

I was invested in IRIS Business Services 3 years back. In one of the conference call, CEO of IRIS, Mr. Swaminathan, was talking about SaaS businesses and he mentioned about Rategain being India’s largest SaaS company. I became interested as one CEO is talking about other’s company. This was before Rategain’s IPO. I started reading about the company and its CEO/Founder Mr. Bhanu Chopra. I was realy impressed with his focus on profitability . Here is one of the video of him A product with fewer features can sell more: RateGain’s Bhanu Chopra – YouTube talking at SaaS Forum 2015. You will get the gist in just first 3 minutes of the video.

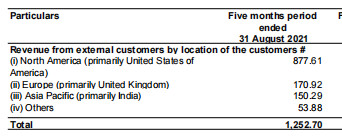

Then I went through company’s DRHP and I noted that the company earns majority of its revenue from North America (primarily United States). US is innovation hub and if an Indian company is able to make inroads in the US then it means it has good and competitive products .

Source: Company DRHP

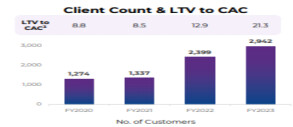

Then I kept building position from 2% of portfolio (in 2021) to about 8-9% (in 2023 on cost basis) as I saw company delivering. Few other key triggers for me to add were very low cost of customer acquisitions and opportunistic acquisition of Adara. In addition management under-promises and over-delivers. My last transaction was in March 2023 and I am not planning to add to it any more given its size in my portfolio.

Source: Company investor presentation.

Please note that I am invested and this is shared only for learning purpose.

Please provide your feedback as I continue to share my rationale for remaining stocks over the next few days.

| Subscribe To Our Free Newsletter |