ICIL has reported an increase in total operating income by 32% to Rs 221.88 crore in FY23 (Rs 168.35 crore in FY22) on account of higher execution of work orders largely driven by improved demand of MHE and industrial gear segment. The MHE segment continued to remain the largest contributor to the overall revenue and constituted around 60% of the total revenue in FY23 followed by industrial gear segment (30%) and the building material segment (10%). Further, the PBILDT margin has improved from 6.02% in FY22 to 7.51% in FY23. The margins are still subdued on account of loss-making building material division (BMD) which reported loss mainly on account of the deferral of launch of new products from December 2022 to April 2023. The management has enunciated that the performance of the building material segment will improve from Q2FY24 onwards with the introduction of new products in April 2023 and the segment will break even in the current fiscal. Going forward, with the introduction of new products in BMD and the discontinuance of payment of royalties for the MHE segment are expected to lead to further improvement in profitability margins.

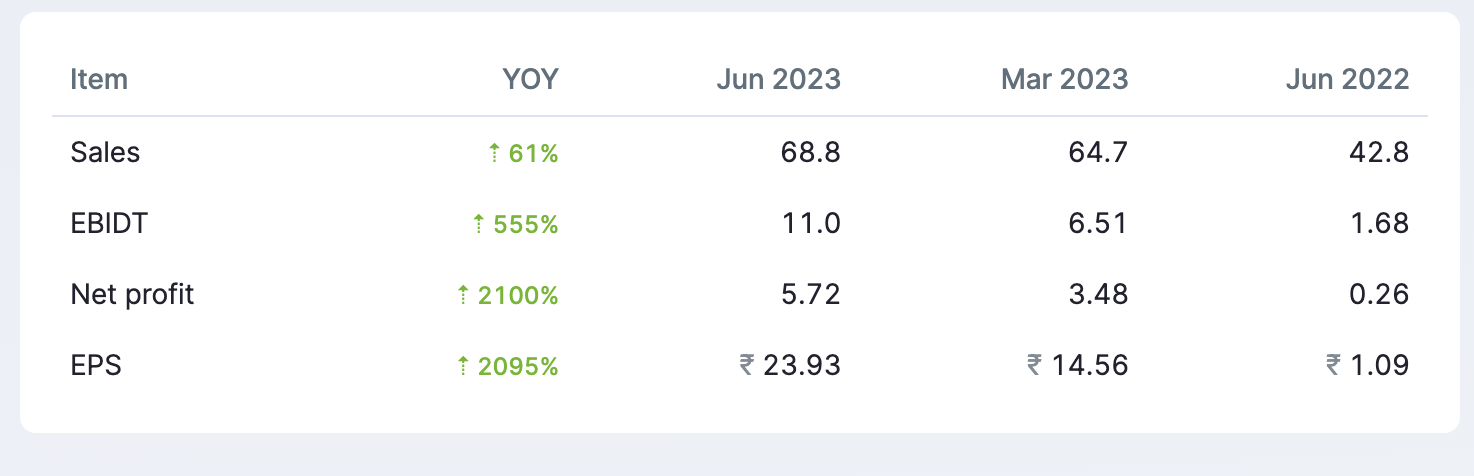

Amazing results. EPS has gone from 1 to 23. Is someone still tracking this company?

| Subscribe To Our Free Newsletter |