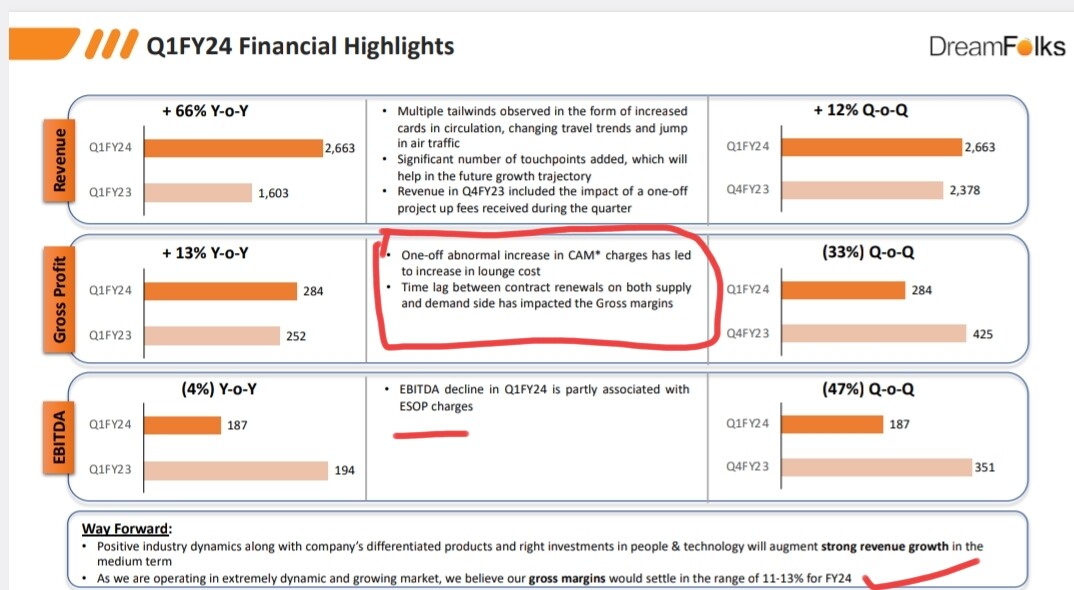

Dreamfolks revenue grew impressive 66% yoy to 266 Cr in line with rise in air travel in Q1. Gross margins are down to 10% compared to 15% in Q1Fy23 and 18% recorded in Q4Fy23 which is disappointing.

Management highlighted a few reasons for the drop in margins:

- One off abnormal increase in CAM charges(common area maintenance) as airports have increased the charges which are passed on by lounge operators to dreamfolks.

- Time lag in passing on yearly escalation charges from lounge operators to bank/credit card providers.

- Employee expenses/ESOP charges(impact of esop will be 6.3 Cr for the FY.)

- High margin of Q4 was contributed by one off revenue for a lounge consultancy service by dreamfolks.(Management didnt even mention this in Q4)

Generally lounge operators will revise the prices from April which will be passed on to network providers starting from Sept month. This quarter seems to have maximum impact of this and is likely to continue in Q2 as well.

Generally yearly cost escalation which use to 5-8% has gone upto 15% now which is difficult to pass on due to higher than expected footfall of which affects card providers.

As more and more airports gets privatised likely that CAM charges will increase as happened in Q1.

Overall management guided for 11-13% gross margin and topline growth of 50%.

Margins may see some improvement as their revenue from other high margin business like golf services increases meaningfully which is probably few years away.

In my view gross margins unlikely to improve even for the next year. Why will lounge operators /network providers offer higher margins again once they make dreamfolks work by accepting 10-12% margins?

Discl: I have sold dreamfolks today except tracking quantity.

| Subscribe To Our Free Newsletter |