Hi Girish, thanks for your comments. Definitely pledge is red flag however we should put everything in context. If promoters are honest and they use the pledge to benefit the company (for loans or borrowing) then you have to think about it. Nevertheless, I shall never keep high allocation to companies which have pledge (high for me is anything 3% or above) as not everything is in promoters control especially market movements and resulting margin calls on pledge or subsequent selling by lenders for recovery.

Now my rationale on Syrma SGS (7% of allocation, 68% profit)

Background: My first buy was in September 2022 at 292 rs. My last transaction (part sell) was in July2023 at 496 rs. My average cost is 280.

In one of the video Ishmohit (SOIC) mentioned that knowledge is cumulative and my buying in Syrma was based on cumulative learning – linked to Dixon Tech, which I bought in 2019. Dixon was making TV sets, Phones, LED lights and security cameras with leading market shares (in some cases up to 30%). For any company in India consumer business having market share of 5-10% itself is huge ask. First thing came to my mind was economies of scale with such market share. I also thought I can play consumer appliances and discretionary spend story through Dixon which was reasonably valued in 25-30PE range. So I entered Dixon for 15-20% compounding returns over next 4-5 years. In April 2020, Indian government announced the much popular PLI scheme. Suddenly my senses woken up, I did some rough calculations on the opportunity size just for mobiles. My numbers were whopping. I added Dixon aggressively. I said in my mind this company will have revenue of 1 lakh crore in next 10-15 years (4k crores in 2020). Also I thought this should trade at 50-60PE given the growth. Rest is history, everyone knows Dixon story. I sold Dixon fully in January 2023 after shocker results and weak guidance, the point was not just the results and guidance but the point was amalgamation of 100PE with it.

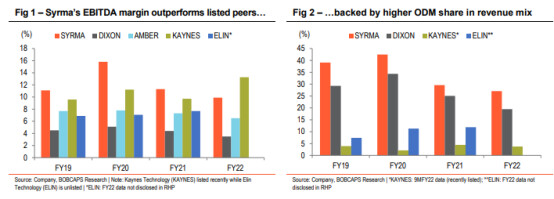

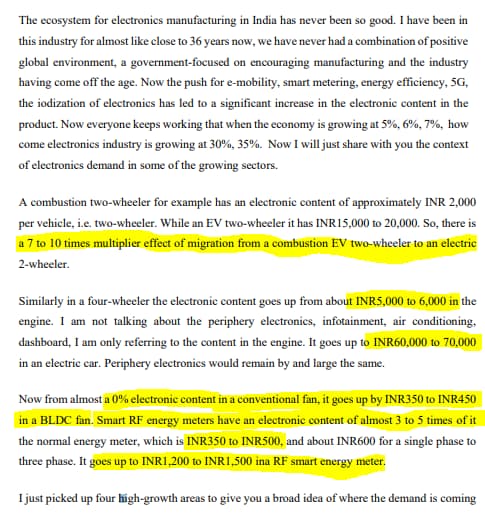

Now how is this linked with Dixon, I was closely following the sector given the opportunity size. With Dixon, Syrma was compared too much during its IPO. The key difference in both was EBITDA margins, Dixon was in broadly in 4-6% range while Syrma was 2x of that. Syrma’s high margin is due to its design capabilities. Its high share of ODM in overall revenue mix vs. Dixon mainly led to it.

Source: BOBCAPS, publicly available report – http://www.dsij.in/productattachment/BrokerRecommendation/SYRMA%20SGS8.12.2022.pdf

There are other areas where Syrma was better than Dixon but it traded at lower PE than Dixon. Further my confidence was boosted by the fact Mr Sumeet Nagar’s Malabar Fund invested in Syrma during IPO – https://www.youtube.com/watch?v=99T-Cta8gf8&t=1231s . My earlier successful investments like Affle, Indiamart, and Saregama were also overlapping with Malabar Fund. While in February 2023, Gautam Trivedi from Nepean Capital also talked about their investment in Syrma (he/his fund invested in Hindustan Foods long back so another alignment of thinking with good/great investors or fund managers. To stay convinced I continue to find reasons, to a certain extent it leads to confirmation bias also (but I don’t mind it). Disappointment in Dixon’s Q3 FY 2023 numbers led me to totally shift my Dixon holdings to Syrma.

Other factors which helped my rationale were, management seemed honest as they reduced IPO. Pre-IPO placement was at 290 vs. IPO price of 220. They mentioned that they wanted to reflect the market and wanted to be a long-term partners with stockholders and benefit together. When most promoters and early investors are trying to squeeze every penny from market, it was a good gesture. I found company has been guiding for very high growth (30-40%) from past several quarters and continue to do so. I have extracted below excerpt from Q4 FY 2023 concall of the company, which provides rationale for high growth:

Source: company concall transcript filing on BSE.

I note that company has been very acquisitive and they had provided good rationale for it. For their recent acquisition of medical devices company Johari Digital, they mention that getting approvals and developing products would have taken many years so they went ahead with acquisition.

Now I will end this with my final thought: whenever a industry has a tailwind we should look at the whole value chain (vendors, suppliers, distributors and customers) and as many players in it.

Disclaimer: I am not a financial advisor and nor a SEBI registered Analyst. The content shared here is only for learning purpose. All the names mentioned here are for example purpose. I may buy more , exit or partly sell the stock without any prior intimation.

| Subscribe To Our Free Newsletter |