Disc – I have completely sold my holdings in last 2 months. This is not a buy or sell recommendation. Views are biased due to recent selling.

There are 2-3 areas that need to be addressed.

Promoter Selling

People who track Shivalik for many years know that management is very conservative and was very averse to share information in the earlier years. That changed in recent years with presentations and conference calls (better for investors, better in the long term).

The company did big institutional days in Mumbai in last few months and came out with detailed presentations. The company did not need funds at that time – capex was done for 1600cr revenue capacity and rations/cash flows are absolutely superb and they can fund any future capex from internal accruals. So it was very clear that promoter selling stake was absolutely one of the possibilities for such an investor overdrive. Other was big acquisition – that will take business to next trajectory.

But promoter selling needs to be put in the context of promoter’s view and past track record. Here are promoters who have painstakingly built an absolutely niche business, dedicating many decades of their life, their own capital, developed own technology etc. They did not sell shares during those decades. For them, wanting to get some cash for their stake after 20-30 years of Tapasya is absolutely fair. There are examples of companies like Page Industries, P I Industries – where companies have created enormous wealth even after the promoter selling.

Why Did I Sell

With all this Gyaan, why did I sell my holdings hypocritically – It was a matter of process/discipline. I am still not sure if it was right decision to sell. From hereon, most of the money would be made from earnings growth rather than rerating (although one can never rule out rerating). The balance of probability has shifted in favor of compounding returns rather than multi-bagger returns.

The other two factors that have kind of discouraging are that – They are guiding for 1600cr growth by 2030 or in 6-7 years. That is 20%+ CAGR growth over 6-7 years. At 690-700, that was like buying 20% growth at 50-55 PE.

The other factor is that business was making 16-18% margins previously and now it moved to 24-25% kind of margin range. I am unsure if these margins are sustainable – to be fair, gross margins have not moved all that much and probability is pretty decent that margins might be sustainable. But we have seen so many cases where margins moved up for companies around COVID times only to regress badly. With expensive valuations, I thought it was better to err on the side of caution.

Another thing was that their market share in some of the segments is already in double digit globally. So ebbs and flows of industry will impact your performance – business can not grow despite the environment at that kind of market share.

From hereon, I am still very interested in tracking the story – looking at how things are unfolding in smart meter space. I am ready to jump back on bandwagon if I get clarity that margins are sustainable and growth rate will move from 20% to 30%. This will be a trading bet and that will have different process in terms of entry/allocation/exit etc.

Business

Now coming to the interesting parts – what is happening in smart meter space in India is absolutely amazing (Exponential growth).

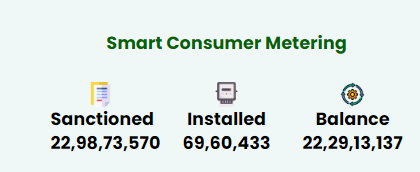

- India has sanctioned 23cr meters and only 0.7cr are installed. Each meter is 8000-10000cr range revenue opportunity – which translates into huge opportunity overall.

- If one goes through conference calls of smart metering EPC players like Genus Power, they have order book of 8000cr+. They are talking about installation of 3-4cr meters over next 3-4 years – which roughly translates to 30,000cr+ revenue over 3-4 years. Genus power is guiding for 1200-1400cr revenue in FY24 and multifold jump – the year after that.

- Similar stories will play out in HPL, Secure Meter, Tata Meters etc.

- Shivalik has opportunity of 50 rs per meter in shunts and 100rs per meter in Silver contacts. If 2cr meter gets installed every year from Fy25/FY26, that is like 300cr of opportunity for Shivalik – which is quite significant.

So the real next step is to do some work to figure our/narrow down Shivalik’s place in smart meter supply chain.

- Foreign exchange spent by Genus in last two years is as follows – FY23 (239cr, revenue – 808cr), FY22 (261cr, revenue – 808cr). So significant part of components are imported. We need to see whether shunts/silver contacts form part of this or not.

- If Chinese companies are involved in this supply (most likely), we need to see the price gap between SBCL’s products and Chinese products. Things will also change if there are import barriers that are raised.

- Based on following players, it also looks like relay + shunt is sold together (need confirmation). We need to find out why? is there any motivation to buy standalone shunt for meter manufacturers? We also need to see if there are some big relay manufacturers in India with whom SBCL can partner.

Doing some online searches – do see following Chinese players in some of the products –

On the homepage of the company (https://www.weijiaelec.com/), there is a video where they talk about having 50,000 shunts per day capacity. They also briefly mention beam welding. 50K per day shunt capacity is not that big, assuming 0.25$ per shunt cot – revenue comes to only 40cr annually.

Following is another Chinese company which have Shunt resistors that are listed on their website. I have no idea if they are manufactured in-house or procured from outside by the company.

| Subscribe To Our Free Newsletter |