The google rating is 3.3 from 1380 reviews, not insignificant, whereas Royal Care is 4.3 from ~600 reviews. This is a primary organic information source for a lot of new customers aside from word of mouth.

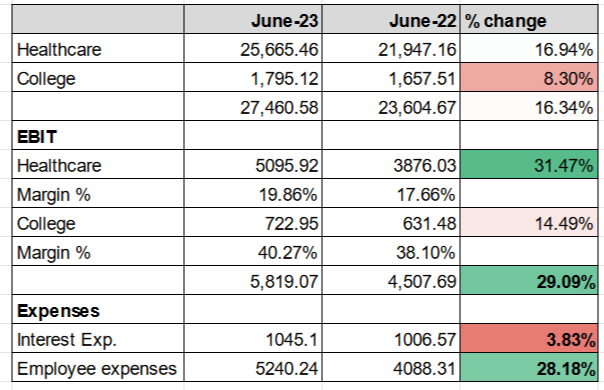

I was going through their Q1 FY’24 financials:

I think the AGM is on 25th Aug. If someone is planning on going and ask the below questions or knows the answers and can shed some light:

- There has been a healthy growth in EBIT (30%), then why have they not paid off the debt (see interest expense). Are they planning on using the money for some expansion plans?

- Employee costs have gone up 30% YoY basis. Aside from appraisals, what is the reason for it?

Edit: Same case for KIMS and KMC, are 30% hikes standard in hospitals ?

? - Any specific plans to scale up the occupancy of the medical college and the hospital to 75%?

- What is strategic view of the hospital to attract medical tourists, are they going for MTQUA certification or tying up with intermediaries?

- Has there been any institutional interest in the hospital stock in past half-year?

- Why is the customer rating so low if the hospital boasts of a stellar reputation, should they not address the issue?

| Subscribe To Our Free Newsletter |