Background

Oriental Carbon and Chemical Limited’s (OCCL) primary business is focused on producing insoluble Sulphur which is a specialty chemical used as a vulcanizing agent to make rubber stronger and more elastic. The largest use of insoluble Sulphur is in the production of tires. OCCL’s market cap on 1st August 2023 is approximately $100M (8 billion INR) with approximately 80% of it constituting tangible book value.

Outside of China, there are only three large producers of insoluble Sulphur – Eastman Chemicals (70% market share which has sold its tire additive business to a private equity firm for $800M in 2021), Shikoku (15% market share) and OCCL (10% market share). Of these three, OCCL is the only pure play on insoluble Sulphur. Chinese production has typically been consumed within China.

Business drivers

86% of OCCL’s revenues stem from insoluble Sulphur with the remaining coming from byproducts like sulphuric acid and oleum. Of the total revenue of insoluble Sulphur, 50% comes from international consumers. OCCL is the sole manufacturer of insoluble Sulphur in India with about 50-60% of domestic market share and 10% of the global market share (mostly focused on India and Europe but growing in the USA as well). Insoluble Sulphur is approximately 2% of the cost of tires. While the tire market has many players and is fragmented, the market for insoluble Sulphur is highly concentrated. Overall, in the world and specially withing India, the number of kilometers driven per capita is bound to increase, and thus the market for OCCL is going to grow.

The key business drivers affecting the demand of insoluble Sulphur are the replacement market which is about 70% of the tire demand and commercial vehicles which consume approximately 10 times the amount of insoluble Sulphur as passenger vehicles. Typically tire manufactures enter into a five-year contract or longer with a supplier of insoluble Sulphur and thus the barriers to entry for competition are high. Moreover, the standards for insoluble Sulphur are consistently increasing, thus making it hard for new players to enter the space.

Analysis of Financial Statements

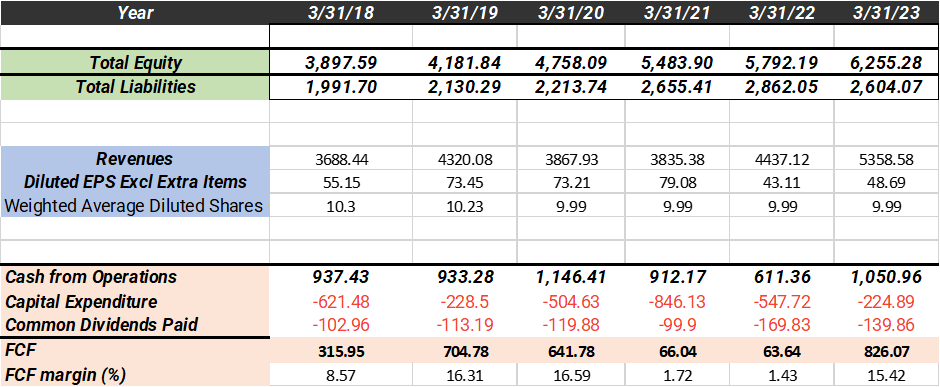

Table 1: Key metrics from financial statements in millions INR over the past five years.

With a market cap of INR 8000 million, the tangible book value is INR 6255 million and there is a healthy five-year equity growth rate of nearly 10% per annum. EPS growth rate has been low because of high input costs (Sulphur, coating oil – these are byproducts of oil refining and OCCL competes with fertilizer manufacturers for these raw materials), high freight costs and high costs of energy in 2022-23. This has also pulled down the ROIC by several percentage points in 2023 to 10% (five-year average is 14%). Total debt levels are reasonable at six times average five-year FCF of which long term liabilities are just INR 800 million. Dividends are sustainable at only 32% of five-year FCF. EV to EBIT is 11.4 in 2023 but this is with subdued earnings owing to high input, freight and energy costs.

On a ten-year DCF basis, using FCF as the input, and assuming conservative growth rates (10% and 7% for the first 5 and last five years with a historical PE of 15), the stock is currently priced for 8.3% return.

Table 2: A DCF valuation for normal, best case and worst-case scenarios using FCF as input.

Investment thesis

While a specialty chemical with several barriers to entry, insoluble Sulphur has the characteristics of a niche commodity. OCCL has a strong balance sheet but only mediocre ROIC and needs continuous capex (despite that typical FCF margins are 15%). There is a large and growing opportunity in India where OCCL does have an advantage in terms of lower freight costs for the finished product. To have a good margin of safety, a good entry price would be close to book value to minimize downside risks and leaving just the upside which can be a 2x. For now, wait for a 20% decrease in price to buy.

Company news

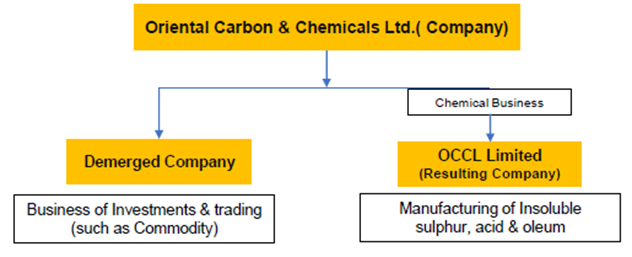

OCCL over the last few years has invested in unrelated companies (VC style) with approximately 12.5% of market cap held in these instruments. While these investments have been successful so far, there is a risk of deworsification. However, the company had announced a demerger with the chemical business (cash cow) separating from the rest. This is expected to materialize in 2023.

Catalyst

A lot of bad news is already baked into the price. Both the demerger and the normalization of input, freight and energy costs (or even one of them) will improve margins and EPS. The tangible book value provides a floor for price. If purchased close to book value, this is a good risk reward play.

** Invested

| Subscribe To Our Free Newsletter |