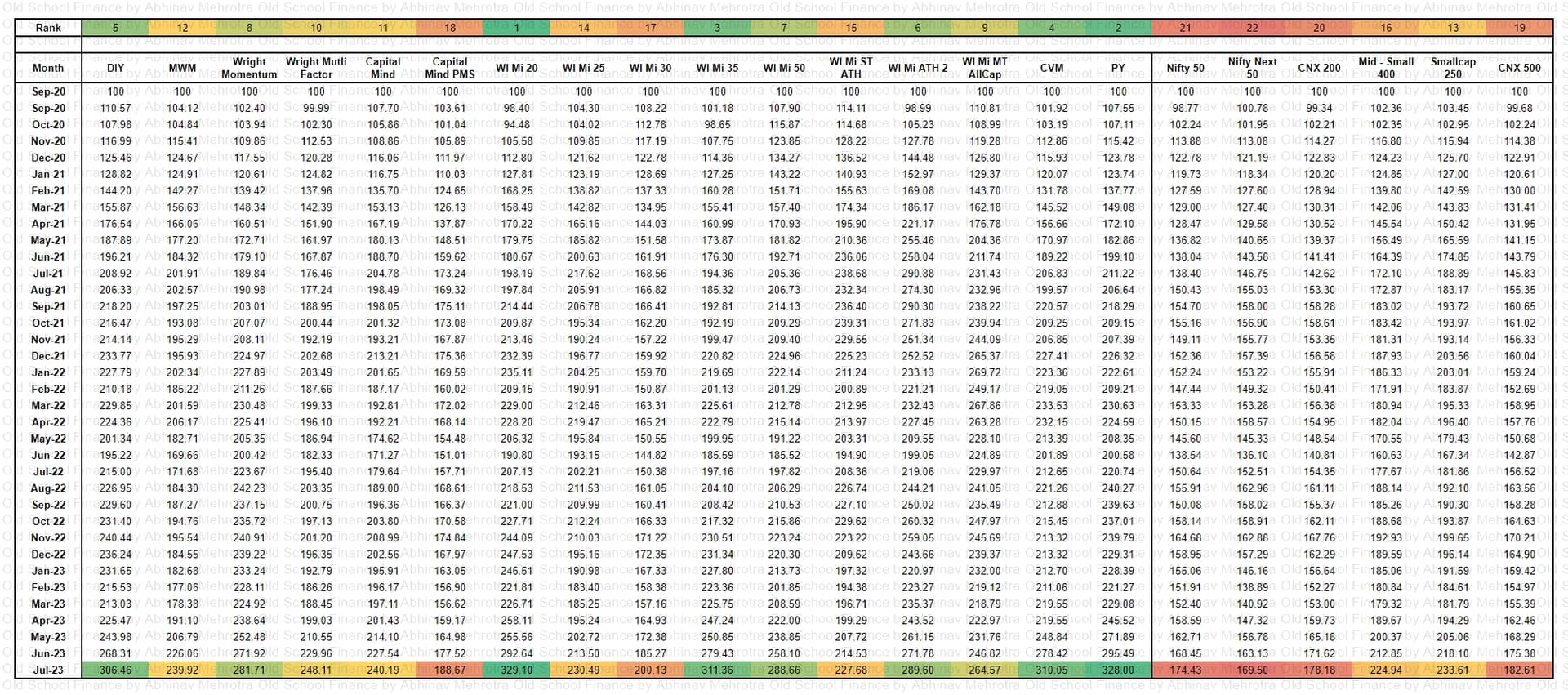

Since momentum is a well-known product I have benchmarked my performance to other smallcases as well.

Usually the correlation is lowest between value and momentum. So it makes sense to run a barbell or satellite-core framework in portfolio of these two.

Value+growth+quality can be discretionary and momentum can be systematic non-discretionary.

Mixing the factors doesn’t always have the best results. They are best run separately.

For diversification in portfolio asset allocation is a better diversifier than factor diversification.

You will find the fama-french library of factors date tailored to India here: Invespar

There is another resource called qfinr where you can input your PF returns, or your MFs and see which factor you have been historically been exposed to.

| Subscribe To Our Free Newsletter |