AR 23 is a good read – Switchgear etc are seeing healthy demand and grew 40%+ incldg exports, higher probability case of 20%+ topline and much higher Ebdita growth(improving product mix + RM stability + better realization ) – overall a good proxy for electrical infra theme with good growth + some rerating possibilities,

-

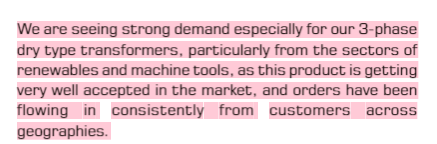

New products (much higher margins) seeing good traction in exports with spike in export for 3 phase dry transformer and DP contactors volumes, should aid product mix improvement.

-

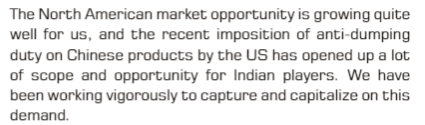

Industry & tailwinds – some tailwinds working in favor ofIndian players in expports particularly , CG Power in their concall has indiacted very high demand for switchgears and supply constraints giving visibility for future, to an extent that they are not able to fulfil given very large OB /enquiries. A possible tailwind here

-

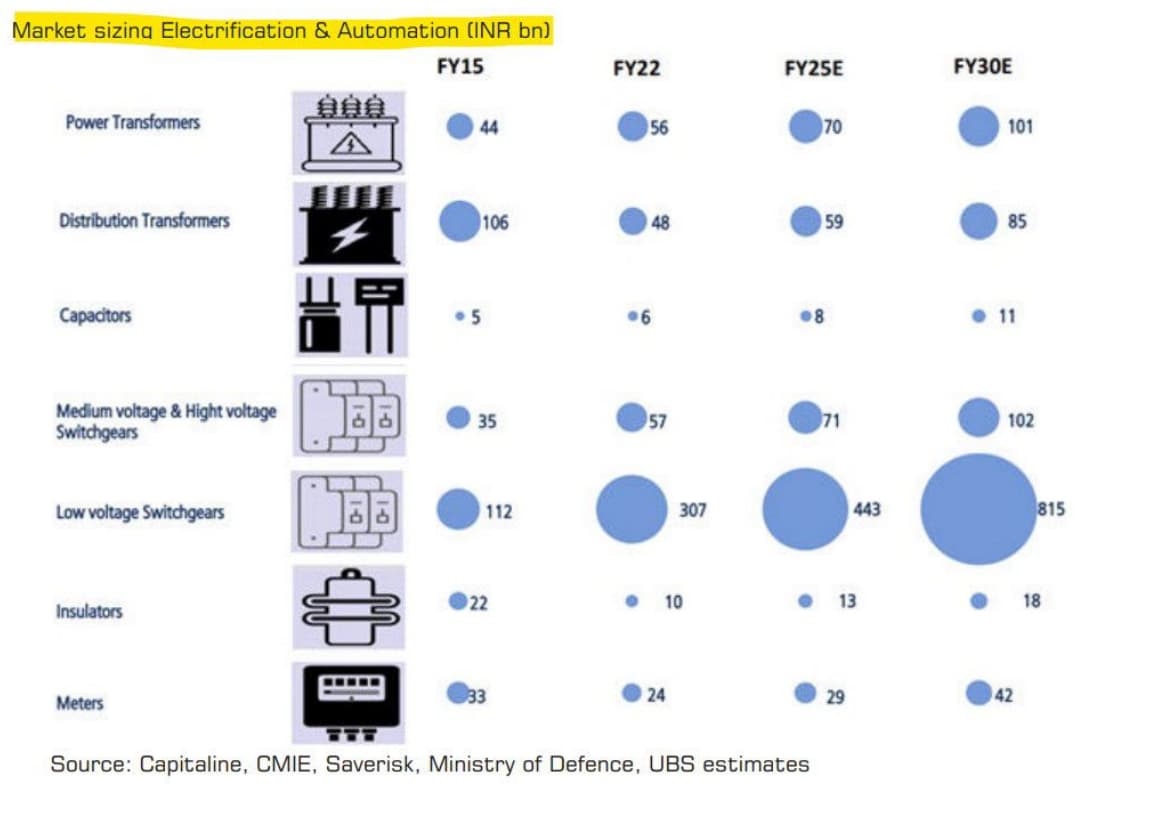

switchgear projections indicate rapid expansion i

Price action Taken out ATH on charts and likely to do well from here

EV chargers – Mgmt calls EV chargers JV as high optionality case FY 25 onwards but need to be seen as project has seen some delays, though some good discussion in Q1 concall here on status updates and higher focus on fast chargers (not a crowded space like regular chargers) – space as a whole should see exponential growth in coming times. Their JV with EU player makes it less denting on capital reqmt.

- Promoter also indicated raising holding in one of recent interviews – more connected to mkt perception than performance itself, if and when it happens will help further

D – invested

| Subscribe To Our Free Newsletter |