[New to Tejas Networks.]

The company’s Mcap is 14.3K cr.

and the order book seems close to 10k cr. ( 7500cr from tcs for bsnl + ~2400 that will come for ITI )

and this 7500 cr will be in the next 1.5years.

Now, my query is,

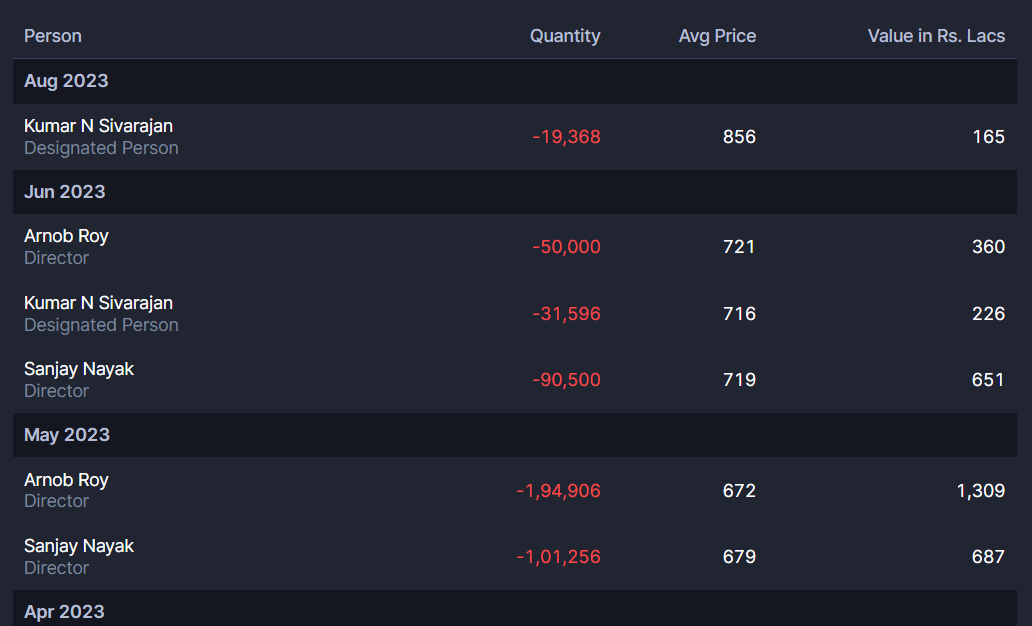

why are the kmp & director’s selling it all off?

there is an inventory buildup of 354 crs and recievables of 169 crs.

and anything regarding the dilution of equity done for 1500crs in 2 years?

edit* : inviting views, just the selling part seems a bit off since, kmp would want to hold onto even higher number of shares, they why are they selling so much that to month on month as the prices sore.

| Subscribe To Our Free Newsletter |