Thanks Venkatesan for your comments. I have about 5-6 stocks under R&D, I shall share them as and when I build rationale on them.

My rationale on PB Fintech (6% allocation, 52% profit).

Background – My first buying was in July 2022 at 557 and my last transaction (sell) was in July 2023 at 775.

From its IPO till early 2022, I thought this is the most pathetic tech business. What’s the point of having online platform? Comparison? and then having some people to call customers to buy insurance, not much different from existing direct agent sales business! I thought it’s a charade of a tech business in the form of hidden physical presence and I thought it will never be profitable as they will need lot of people to continue to grow.

Then in early 2022 I started hearing about PB from people I follow. Amit Jeswani talked about it in April 2022 here https://www.youtube.com/watch?v=F8nmBsYSz64 (at 42 minute) and here in June 2022 https://www.youtube.com/watch?v=OZADGK7vYt0 (at 36 minutes). Amit Jeswani has explained all the rationale from 36th minute to 42nd minute, which later on I also discovered ![]() . Mr. Ishmohit was also studying it during the same time –

. Mr. Ishmohit was also studying it during the same time –

Sourced from twitter page of Ishmohit.

When these people study or talk about businesses, I take note of it. Though I was very reluctant, I started listening to conference calls. First thing I noted that loss for March 2022 ending year had 833 crores of loss, but it included 500-600 crore of ESOP charge. I had a bit of a sigh of relief that all the losses are not business related but bit of accounting also. I took a token position (1% of portfolio) as stock was downhill all the way (from 1300+ in November 2021 to my first buying of 557 in July 2022).

I continued to follow the company and I had a eureka moment in August 2022. When I noted following:

Source: Company transcript Q1 FY 2023 call. https://www.bseindia.com/xml-data/corpfiling/AttachHis/63891711-e1ab-4fa2-8fff-26d615f1b572.pdf

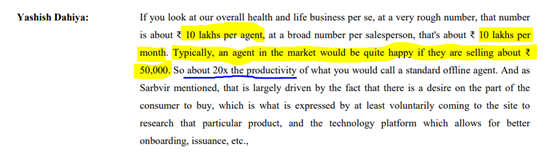

So the PB’s agents were doing 10 Lakh a month kind of premium with a follow up on online queries. My excel/calculator started working; that means one agent on average does over 1 crore of premium annually. On a take rate (commission) of ~13%, per agent revenue is ~13 lakhs. We know in India for a similar skill set companies must be paying around 8-9 lakhs annually. So per agent PB was highly profitable. Any Insurance company hiring agents will have similar cost but premiums per person will be low.

Post this eureka moment I tripled my position to over 3% by October 2022. However, stock kept going down around 360 by November 2022. So I had no courage to build position, then stock moved up so I built my position further in range of 450 rs to 540 rs to take up the position to ~5% by February 2023.

So my initial thought process of PB Fintech being a not so good business changed with two things 1). Why customer comes on PB platform? The main thing is there is no push but a pull, customer needs the product so when a PB agent or their call center makes a follow-up then conversion rate is very high vs. a cold calling agent from direct insurance companies. 2). Owing to high conversion rate productivity of an agent is very high so highly profitable proposition.

PB has its own call center support (300+ employees), offline agent support (1000+ employees), and about 1 lakh point of sales persons. Now think how someone can replicate this without bleeding for years? PB has created its own brand over the past many years.

Online insurance penetration will continue to increase so PB shall continue to grow at 2x-3x of industry growth. I personally put industry growth in 10-15% range. So PB will grow topline (at similar take rates) at around 20-30%, while bottom-line will grow at much higher rate owing to operating leverage (fixed costs and relatively stable marketing costs). I have not looked at their paisa bazaar much but that is also coming up well and provides optionality.

For such business I would have kept higher allocation but I note that ONDC kind of platform; Bima Sugam may impact its business either shaving off growth or shaving off take rates. Keep an eye…

Disclaimer: I am not a financial advisor and nor a SEBI registered Analyst. The content shared here is only for learning purpose. All the names mentioned here are for example purpose. I may buy more, exit or partly sell the stock/bonds without any prior intimation.

| Subscribe To Our Free Newsletter |