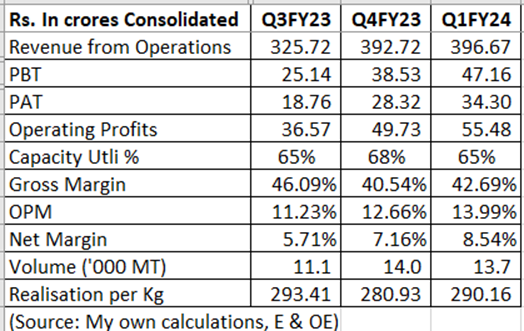

The Q1 FY24 results looked disastrous on a YoY basis. Moreover, in the concall the newly appointed MD VS Anand said there has been aggressive Chinese dumping, and it has in fact intensified in July. I am surprised that despite this, the stock has not fallen since the results. This may be because sequential revenues, operating margins and profits have risen for two consecutive quarters, volumes have inched up and realizations have remained stable.

Capacity utilization in Q1 was 65 %, so there is ample scope for growth without incurring any major capex. Even at current scale of operations (i.e., assuming no growth), the company should earn around Rs.150 crore of CFO per year. Debt is zero. Maintenance capex is around Rs. 30 crores. Cash in hand is more than Rs.200 crore and there should be a cash accretion of more than Rs.125 crore per year going ahead. This is assuming no growth.

Restrictions remain in place for tyre imports, though there is no complete ban. Tyre imports into India went up 15 % in FY23 (by value), but they don’t seem to be a major worry for tyre makers in India right now, going by their commentary. This augurs well for domestic tyre production, and consequently for NOCIL.

With no major capex on the horizon, zero debt and surplus cash, there is a lot of optionality in the company, either to increase the dividends / buyback or deploy funds for other initiatives. VS Anand took over as MD of NOCIL from 1st August 2023. A new chief always kindles hopes of injecting new life into the company. In reply to a question on what he would like to change at NOCIL, he said he would like to be bold and brave in international markets. I am not sure what this means, but I would be watching closely his strategic actions.

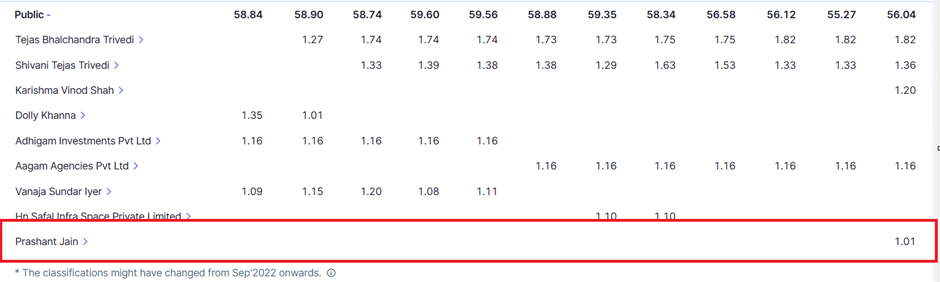

Finally, I notice that one Prashant Jain has taken a 1 % stake in the company last quarter. Not sure if it is the “same” Prashant Jain we all know, but he was also a “value” investor.

Based purely on price action, it seems to me the stock may just have bottomed out.

(Disc.: Invested. Not a recommendation)

| Subscribe To Our Free Newsletter |