Doing pretty well, 1250 is big resistance, once this is taken can see 1500 to 2000 levels

Inox Wind Ltd

-

Management guiding for 500MW(2000cr-2500cr) installation this year and will conservatively do 700MW(2800cr-3500cr) my estimate in FY25. Current sales of 700cr.

-

Company will be debt free by Q4 FY24 (current interest cost is 330cr). They did a 500cr QIB on 8th august which will be used for clearing debt.

-

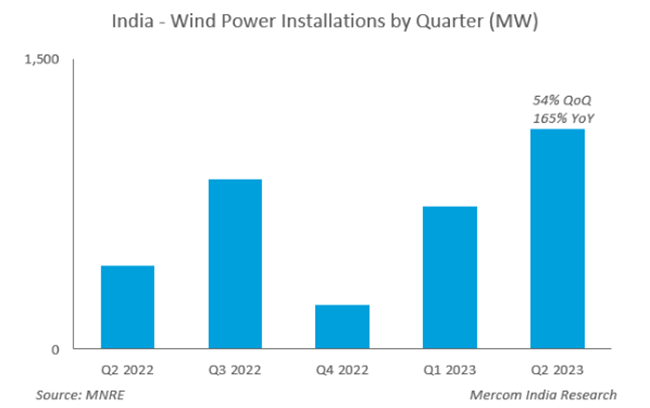

Current wind installation run rate is 4GW per year which will easily cross 5GW in FY25 and Inox historically maintained 20% market share hence ideally they should do 1GW.

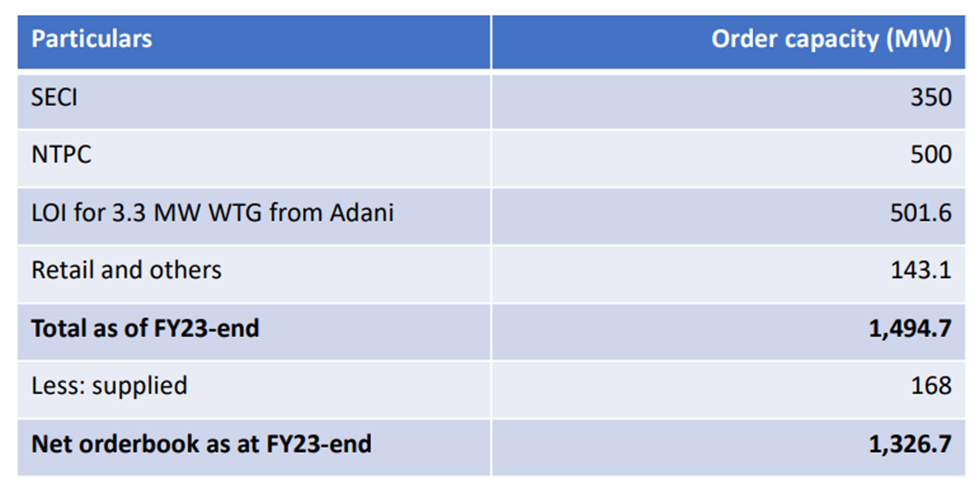

- Their current order book is 1.3GW and we still have 2.5GW of auction to be done this year from center (private not included) so as per me the demand> than supply. Hence the key thing now is execution apart from that everything is in place

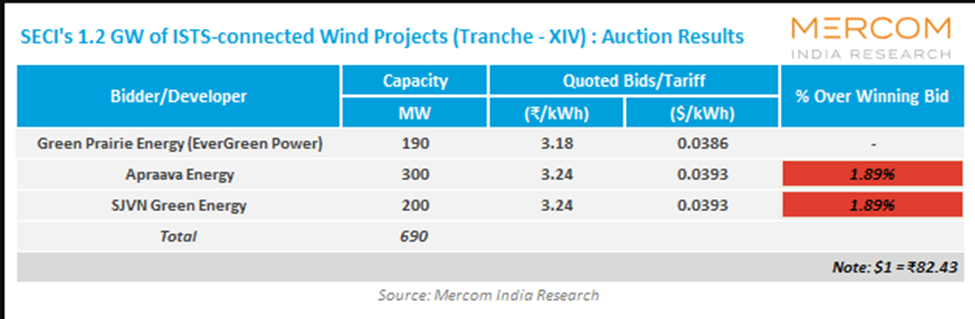

- Once of the biggest reason for the collapse of wind industry was tarrif. In a 1.2GW auction in June 2023 by SECI only 600MW qualified as bidding price were above cut off tariff. Margins will be at historical level 14% – 15%. Tariff went as low as 2rs per Kwh in 2019-2020, Currently at 3.24

TECHNICALS

Recently gave a big breakout and I expect from H2 we would see significant improvement in numbers.

- Current suzlon valuation is 17-20 times FY25 EPS ,if inox gets these valuations they should trade at 300 to 350 (Please note I am assuming a PE of 17-20, this is my base case assumption) @fundoo

I have already posted about them on their thread the reason I putting it here again is after the recent fall I have increased my initial position by 35% and at these levels the RR looks good..

Disc – Invested, with average price of 175

| Subscribe To Our Free Newsletter |