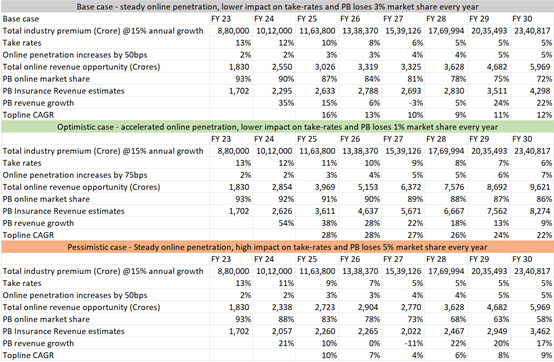

Satish thanks a lot for your comments. You raise excellent points. PB, PhonePe and Paytm Insurance are just brokers so I beleive there is some pricing gimmick. Either PhonePe is subsidizing it with low take rates or products offered are no-frills. The main strength of all these players is customer reach and conversion ability. As an investor we need to monitor and take the pain whenever necessary. We can take assumption and work with those. I have following back of envelope worst, base and optimistic scenario:

I assumed 15% insurance premium growth in all scenarios. In all scenarios in 6 to 8 years, return (CAGR) range is 4% to 28%. While on 2-3 years basis range is 7% to 28%. I played around with online penetration, take rates and lose in PB’s market share. All scenarios are on topline, while bottom-line growth might be higher than top-line owing operating leverage. Also note that PB has 5k crore cash, which can be used for buybacks in future.

In my assumptions Insurance online penetration best level is 7%, vs. 14% in United states and 6% in China.

Keep an eye, no investment is sure shot investment.

Disclaimer: I am not a financial advisor and nor a SEBI registered Analyst. The content shared here is only for learning purpose. All the names mentioned here are for example purpose. I may buy more, exit or partly sell the stock/bonds without any prior intimation

| Subscribe To Our Free Newsletter |