Morepen Labs

Technicals:-

- Chart indicating reverse head and shoulder and hence long term trend reversal

- Volume pick up around downward trend line break on the right shoulder

- RSI strong and comfortably above 30/40 WMA. Respecting 10 DMA uptrend with support close below

Business fundamentals:-

- With the chemical prices coming down with China dumping, the entire API space is seeing margin expansion from raw material prices after a very tough 2022-23. Till Q4’23, margins were suppressed for these companies due to operating deleverage as there was a high amount of destocking all across

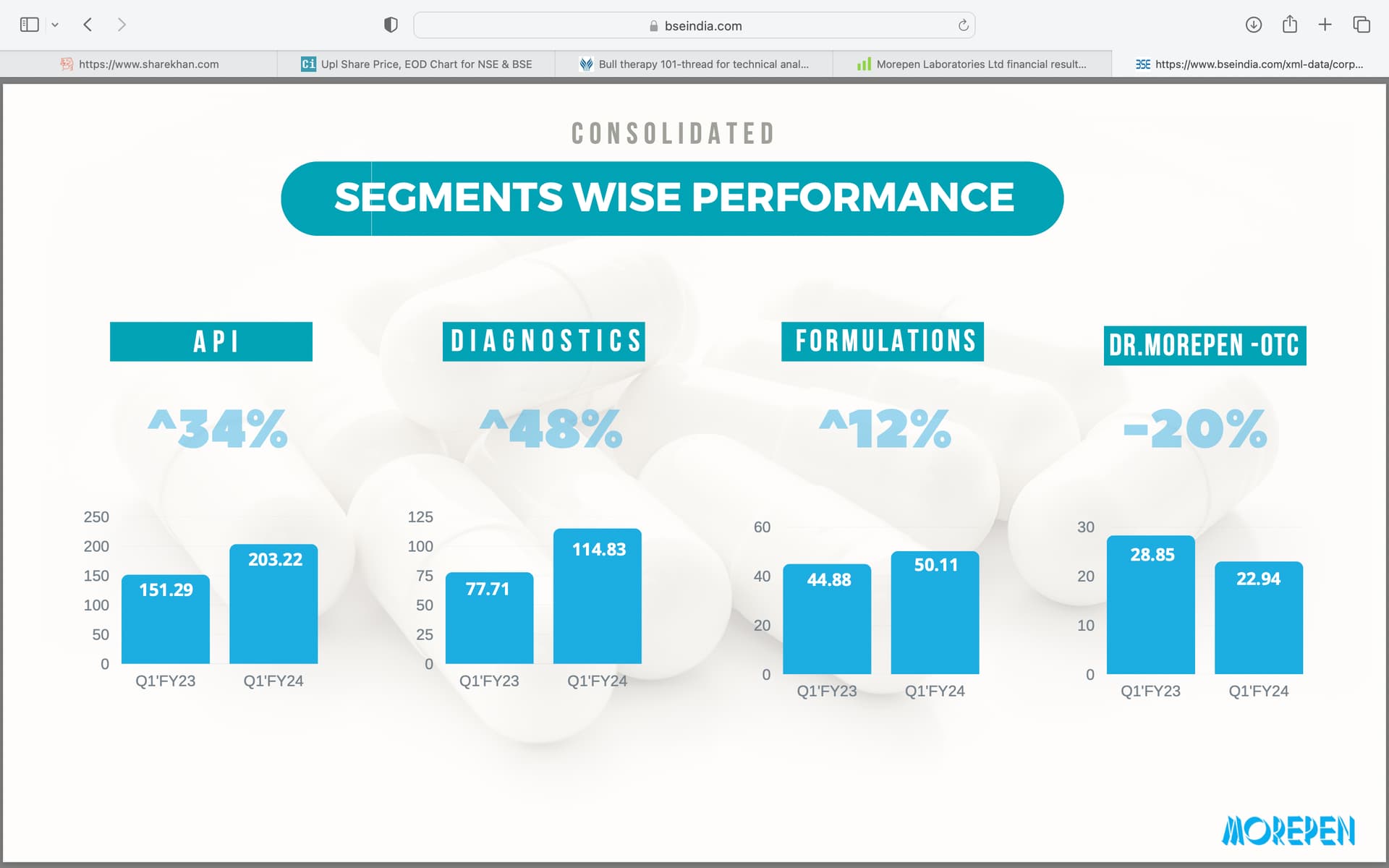

- Morepen delivered a great quarter, although on a subdued base with 32% topline and 73% EBITDA growth, on a subdued base. This was mainly contributed by strong growth in core API business and diagnostics business

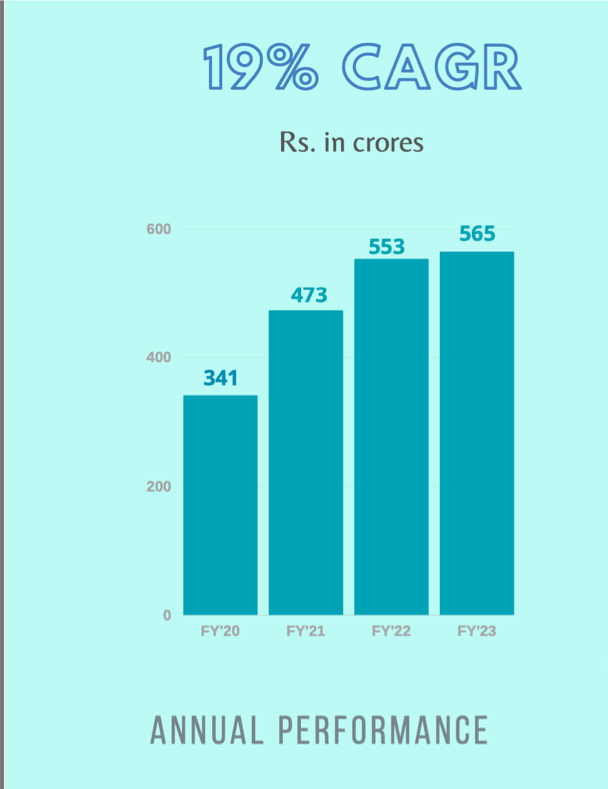

- Company has been delivering good growth YOY for a long time now. Despite a large COVID base, CAGR continues to be ~19% for the last 4 years.

- The margins finally saw an uptick from Q1’24. This company has done 9-13% EBITDA margins pre COVID and even a move to the bottom of this range would be a big positive for earnings on the current base of 6% margins in 2023. Margins finally saw an uptick and conference calls from other companies (notably Divis) indicates better margins should be ahead with RM prices and high stock inventory being out of the system

- Promoters infused capital in the company through warrants recently. This is almost a debt free company which has faced debt issues in the past due to being in CDR for a while. With this new capital, capacity addition is now happening, reflecting in the CWIP.

- They have an interesting consumer portfolio. Morepen as a brand is as it is well known in diagnostics, and new products in the consumer space look interesting

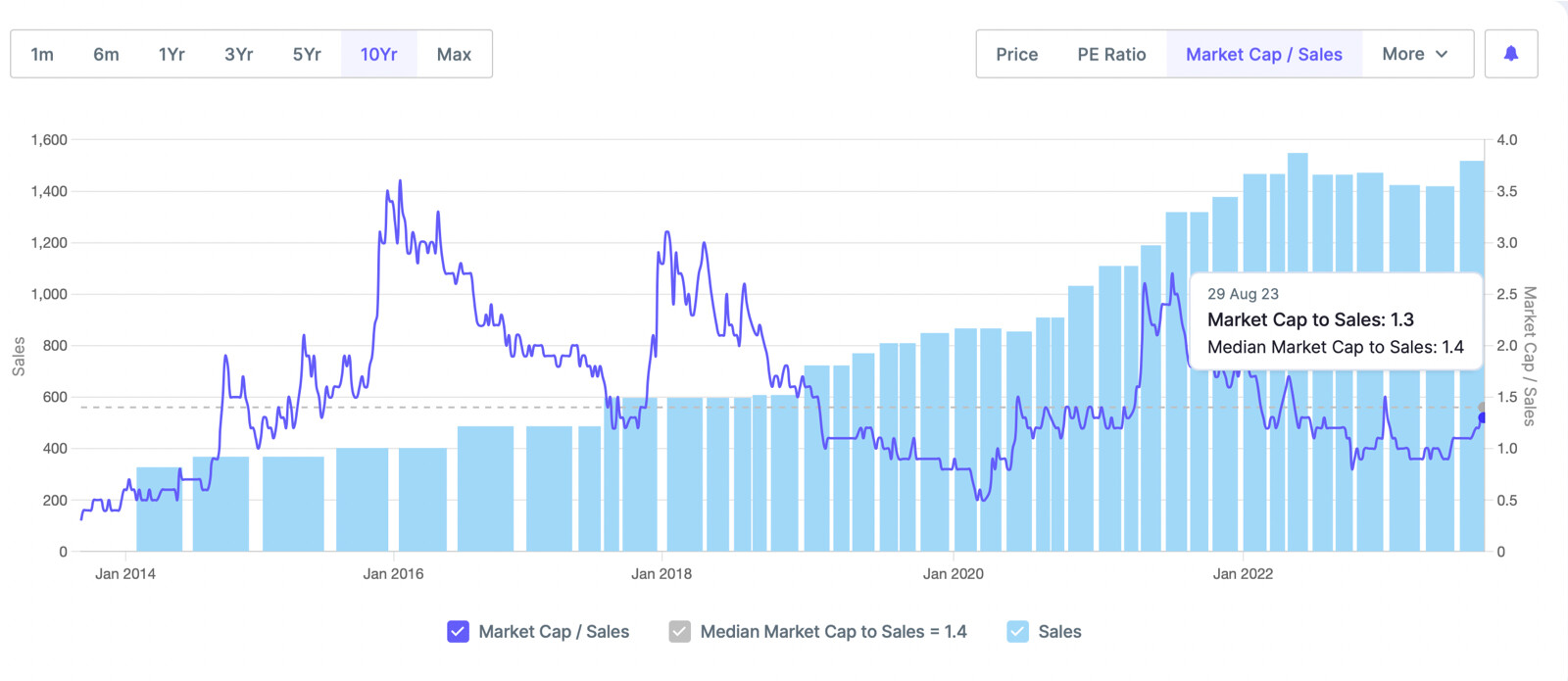

- Valuations not too demanding due to last year margin erosion, still at 1.3x sales, far below its favourable cycle multiples and much below peers

Risks:-

- Corp governance has had issues in the past – this is covered on the Morepen thread.

- They have seen debt/financial issues in the past and underwent corporate debt restructuring

- No concalls for the last 1 year, and hence not much details about growth drivers/margin scenario etc

- Thesis assumptions have been taken from industry trends in the absence of concalls

Disclosure : I am invested in self and family accounts with transactions in the last 30 days and hence am biased. I am still learning the industry and technicals so might be entirely wrong. I am not a SEBI registered advisor.

| Subscribe To Our Free Newsletter |