PEL published investor day PPT. It is very detailed and provide their aspiration for FY28.

Key Takeaways:

-

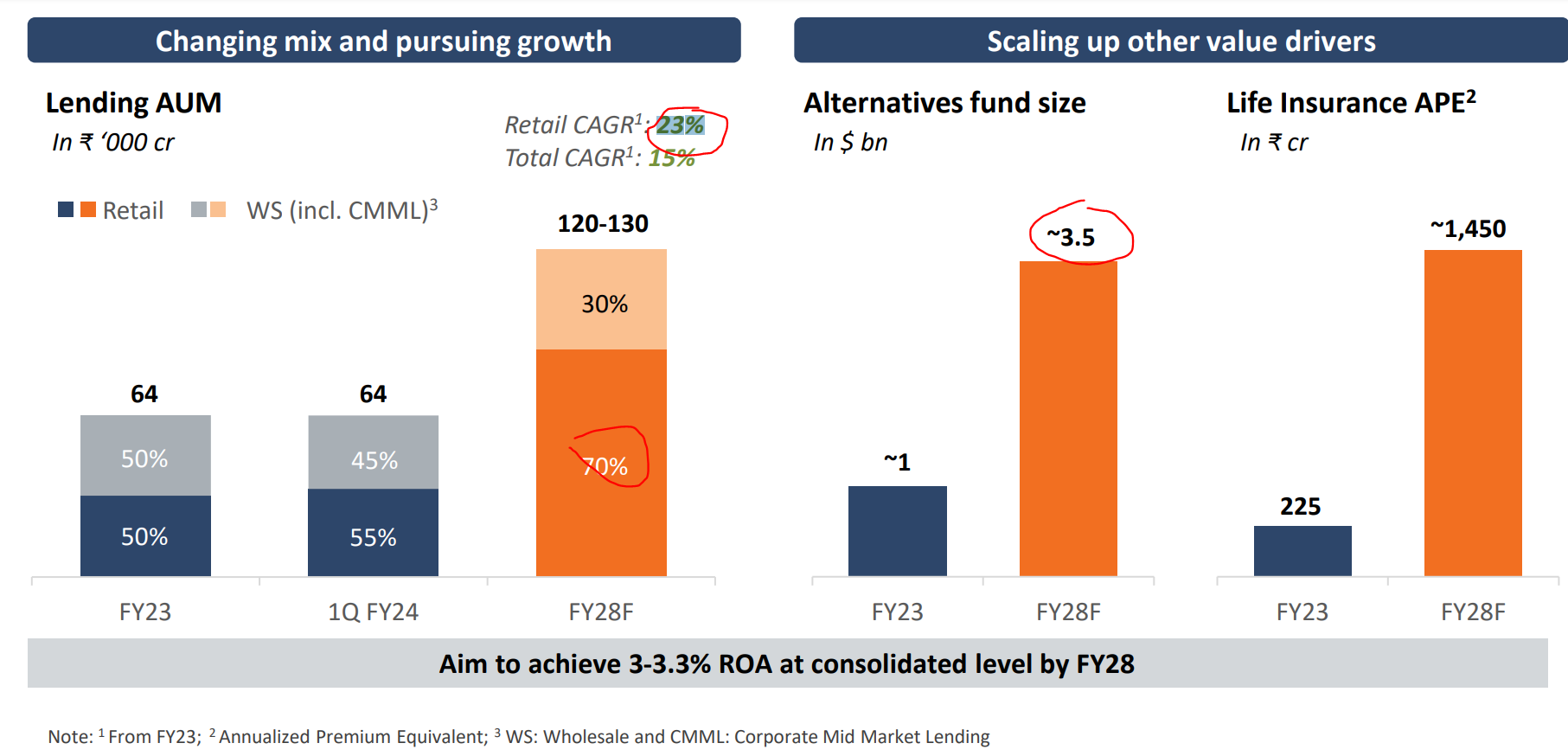

AUM growth outlook: Based on recent performance, they are cautious about retail growth. Although the base was small, now they have invested in technology and opened up many branches, which can be a positive surprise going forward.

-

More than tripling Alternative funds size. This shall increase the immediate fee income (in the next 3 years), but it will not have a meaningful impact on carry payment as the carry comes 3-5 years after investment as it is one of the most important parts of alternative returns (Chery on the cake). PEL generally do not say much about this segment. Once it reaches $3 billion, it will be interesting to see how it shapes up.

-

There is a huge growth in Life insurance, but it may impact the balance sheet as Life insurance is growing much faster, and it may not be profitable yet due to the huge investment they are making in growth.

Productivity Metrics

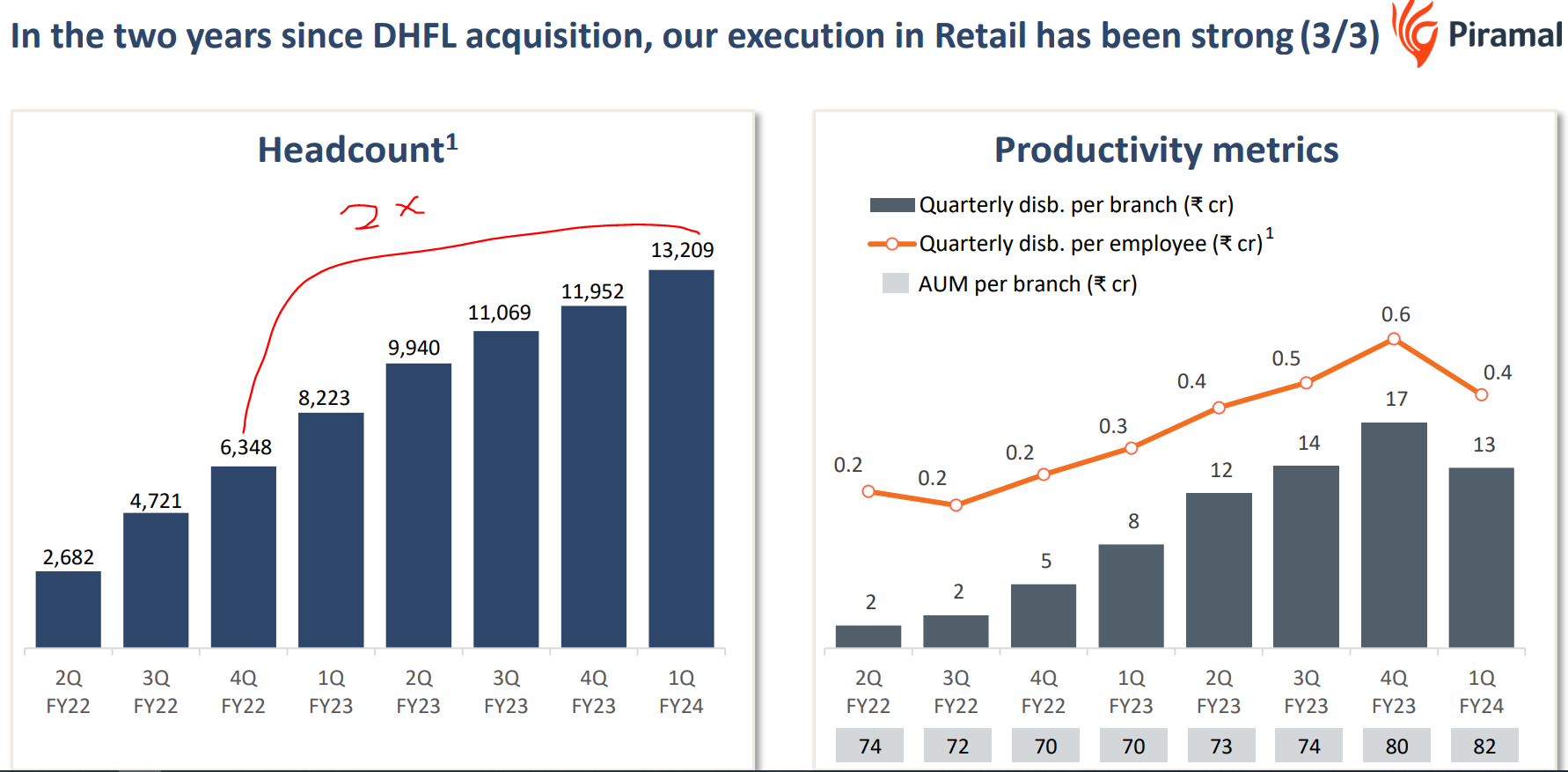

- More than double the number of employees in 5 quarters (well after DHFL acquisition). They have invested huge upfront in building and strengthening the retail front end. The current P&L shows the cost, but not all benefits are realised yet. As they increase the contribution from retail, I think the operating leverage will play out, helping their profitability.

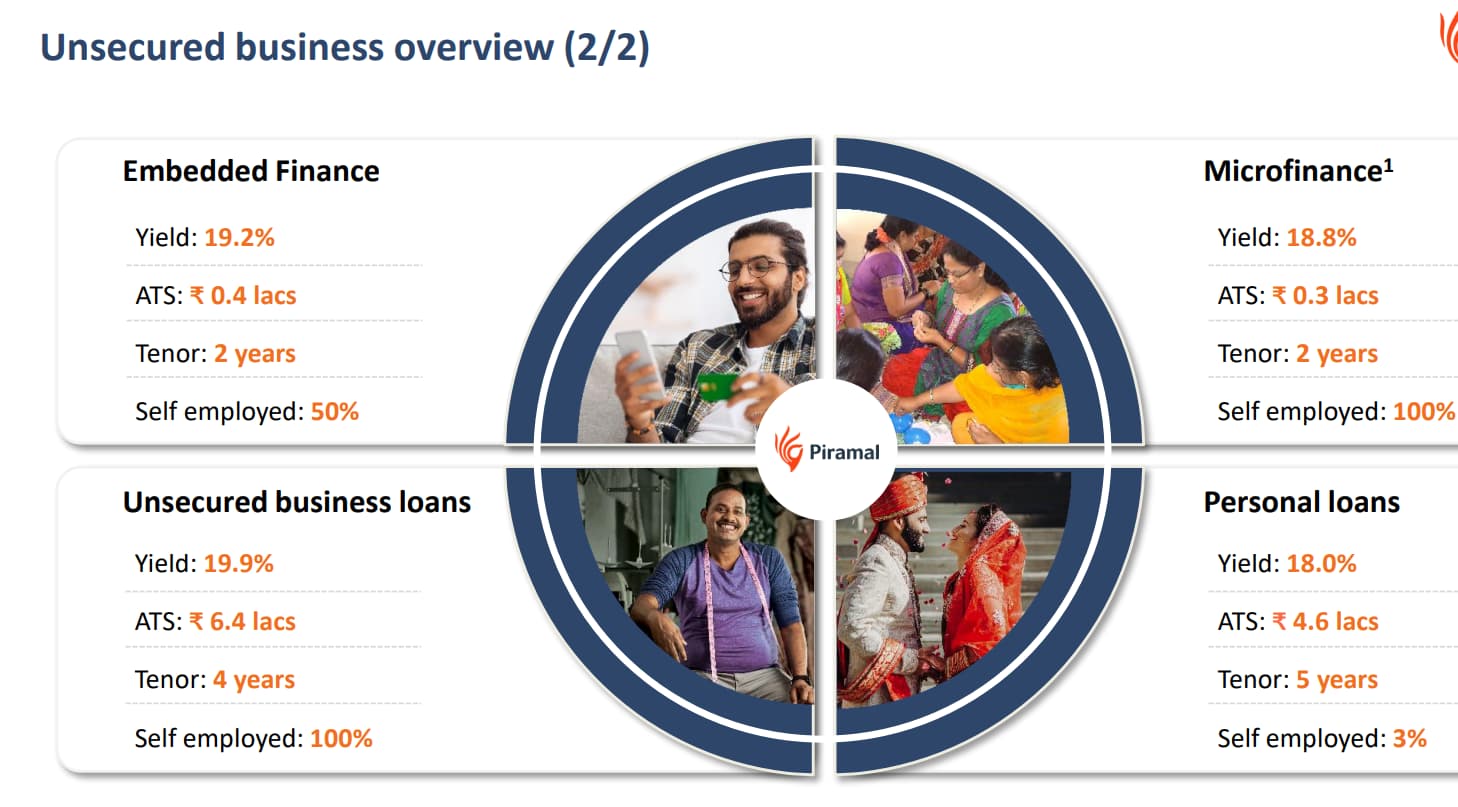

3- Unsecured

- I think this could be the bone of contention. They have ramped up disbursement massively- 40X in 7 quarters. Although the yields are much better, PEL’s records in managing the risk-adjusted return are bad.

-

During 2018/19, they were thumping their chest and saying a lot of things about the quality and how they monitor of their portfolio. They even said that RBI had applauded their portfolio tracking. Fast forward 4 years, they have lost all (or most of) profit due to bad loans.

-

So I would personally not read too much into it now. It is concerning that they are ramping up risky segments very fast, which his fraught with risk. They had difficulty managing secured lending to real estate developers (2X security for the loan), but still made massive provisions how this unsecured fear is a thing to watch. I hope they manage this well after learning a thing or two from Wholesale 1.0 debacle.

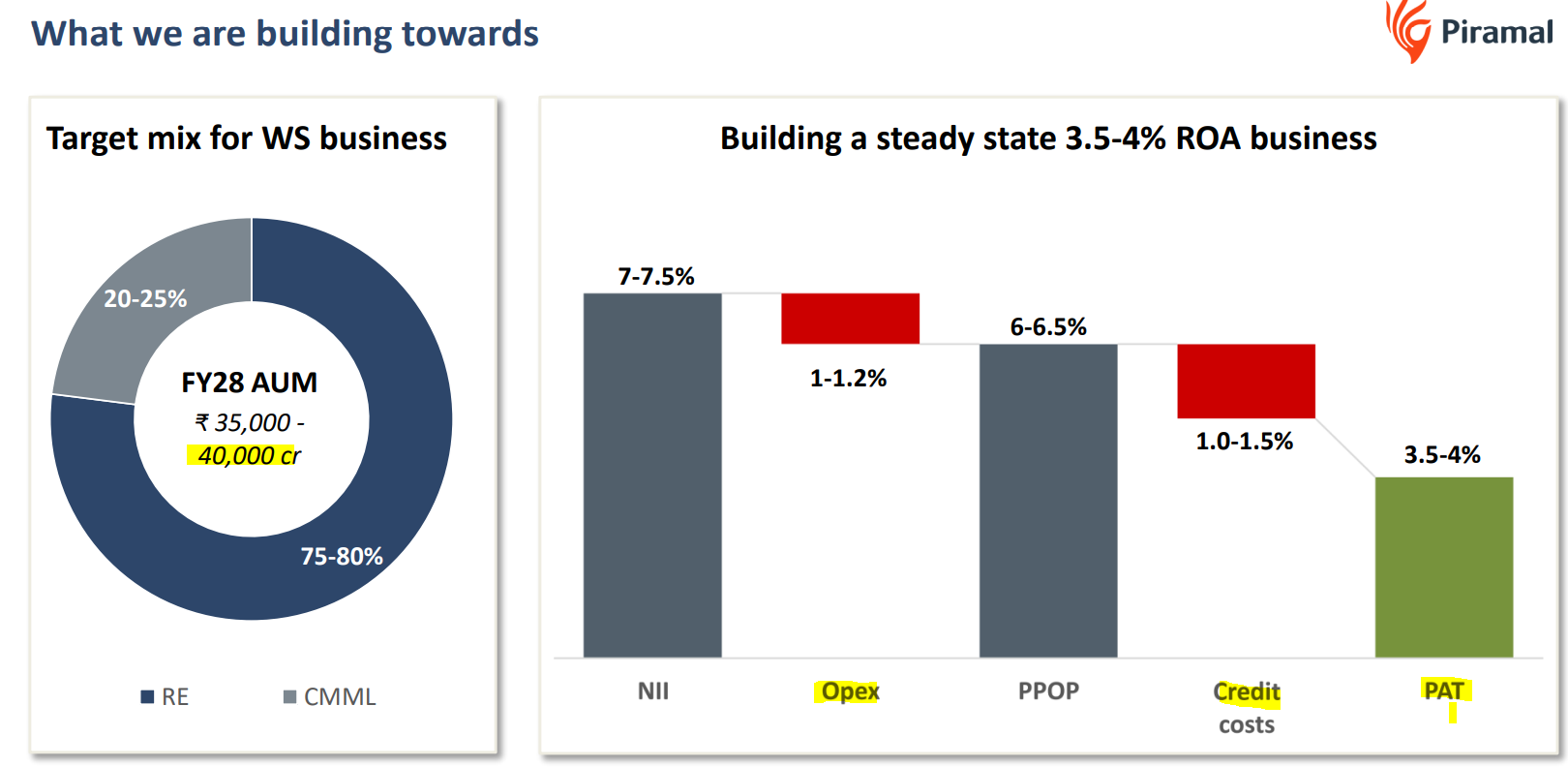

FY28 Aspiration breakdown

-

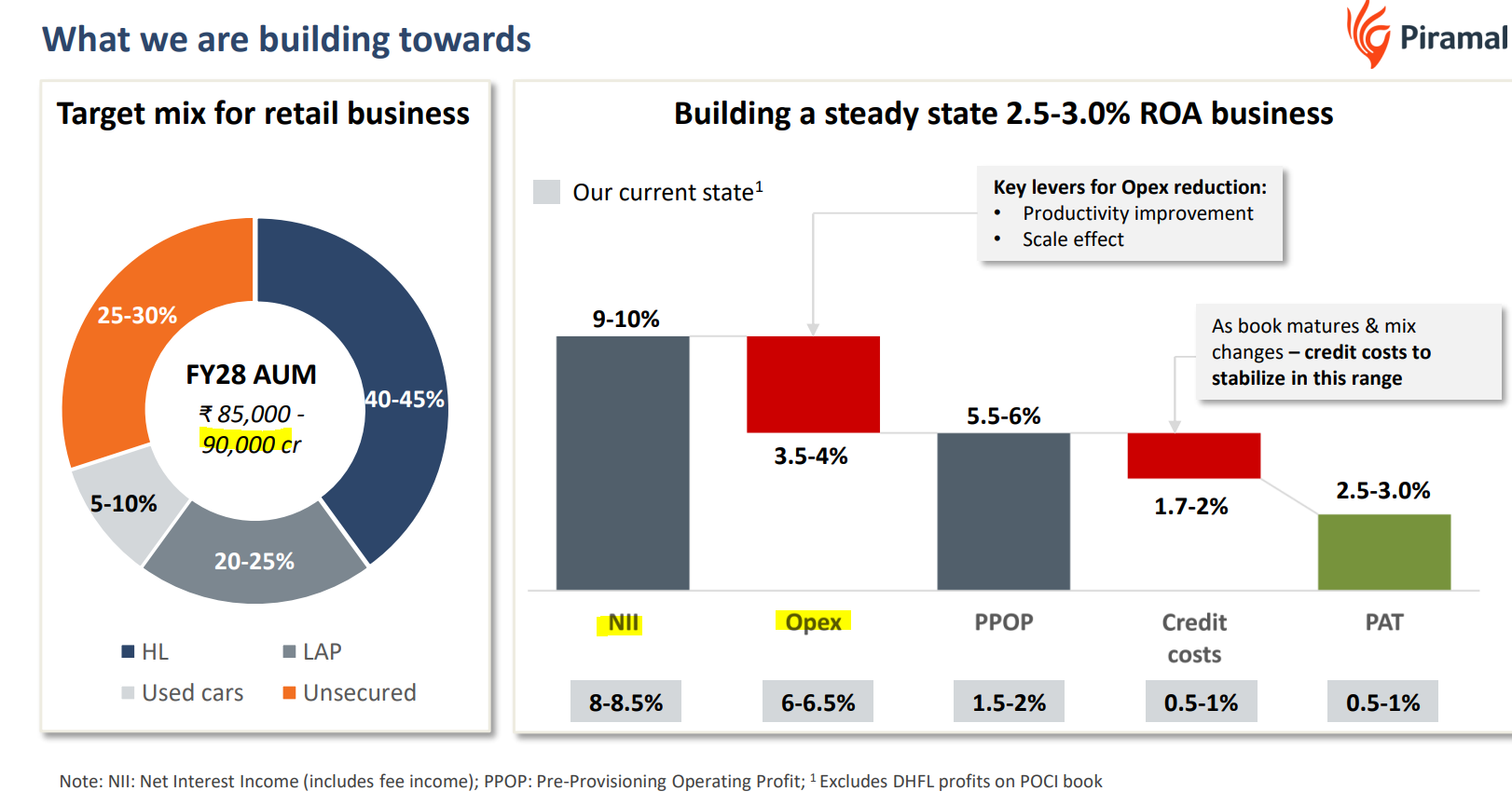

This is one of the most important slides and provides a glide path for the portfolio. Retail AUM target is 90,000cr (Fy23 is ???).

-

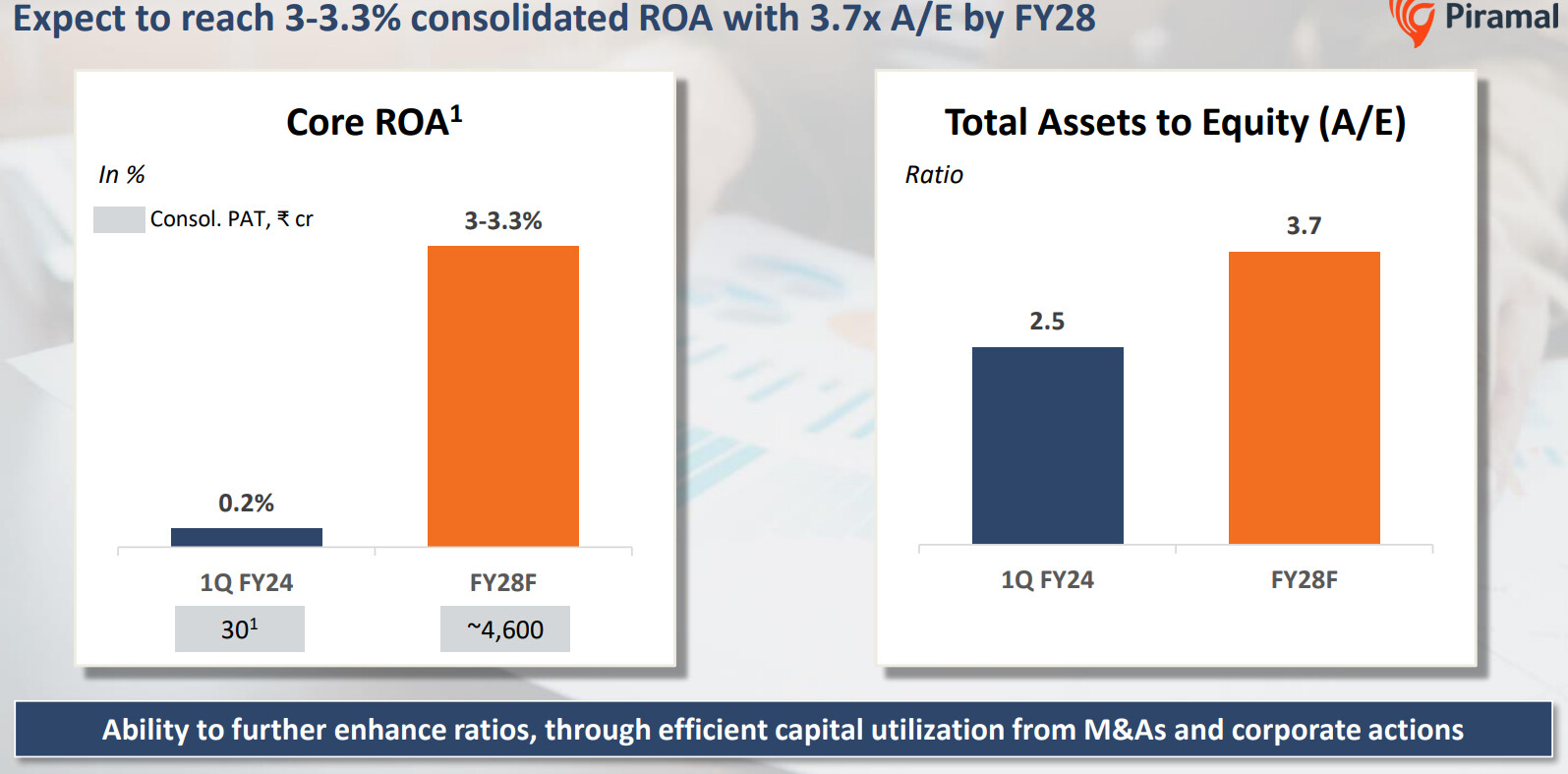

The improvement in ROA is likely to come from Opex reduction or operating leverage play along with NIM improvement.

New Wholesale

Large exposure to land purchase. Even if they manage it well, the market will not like it and is not likely to give a high valuation to this part. So even though it may be more profitable than retail, but if one goes by their own record, the wholesale profitability can disappear in a flash. Hopefully, PEL is lucky second time, and I hope that it fares better than the wholesale 1

Overall good read and they are providing PEL’s aspiration. I think PEL will need 2/3 quarters to clear the book before they start reporting better numbers.

Note- Long term invested

| Subscribe To Our Free Newsletter |