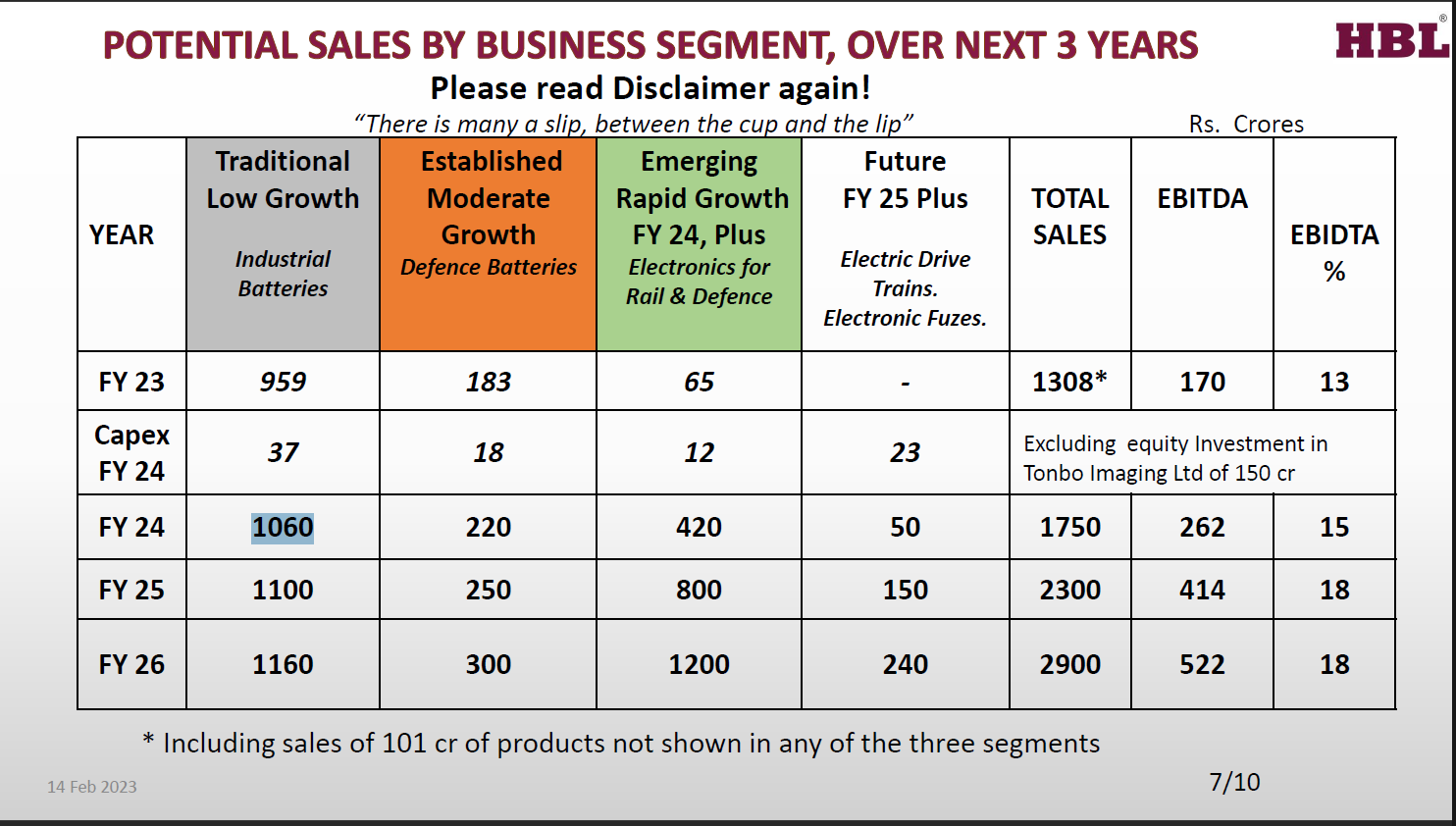

While Q1 numbers were good, the surprise element was in Industrial battery segment which mgmt. had categorized as slow growth traditional business. Mgmt. gave a guidance of 1060 cr. from this segment in FY24 with a growth rate of ~10% and then a growth of 4% for FY25.

However, Industrial battery segment did a 50% YoY and 9% QoQ growth. That’s super duper. Nearly 30% of annual target done in Q1. So is there a case for revising the guidance in industrial battery segment ?

At collaborator’s corner, VP team has already indicated this possibility

- Telecom batteries (Lead Acid) – This segment has seen many years of decline and is now making a comeback due to the improving demand in telecom space fuelled by 5G adoption and higher O&M replacement. Higher volumes in this segment can lead to better absorption of overheads and thereby higher margins from c. 8% to c. 10% – within the existing setup with no incremental investment.

October 2022 Credit report highlighted some of HBL’s top customers in the industrial battery segment, namely Indus Towers and Cummins India in the listed space.

Indus Towers Q1 call has some very positive insights on the telecom industry.

From Collaborators Corner: “The Company has been supplying its PLT batteries to Cummins for its DG sets under white label program – an association that has grown each year for over a decade.”

Snippet from Cummins India Q1 call confirms fabulous growth happening in this segment.

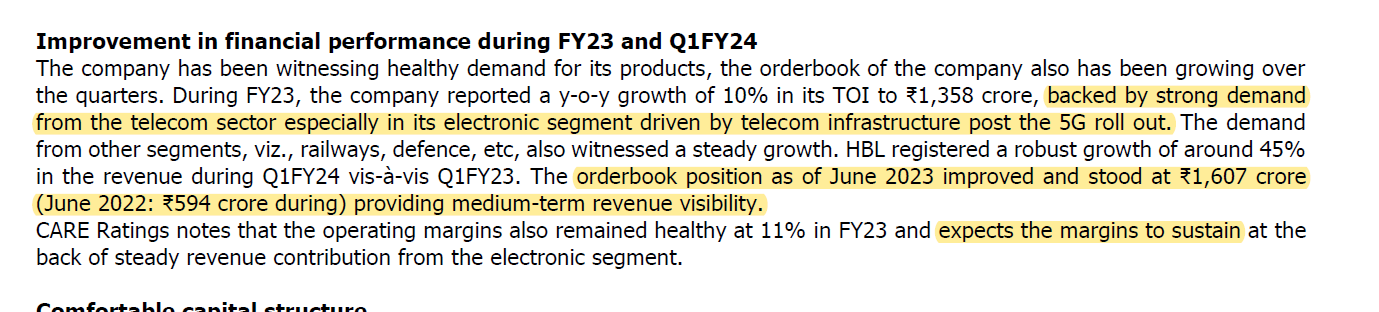

The new credit report released in Aug’23 also highlighted the growth in order book of nearly ~2.6x YoY basis, backed by demand from telecom sector.

There is a chance that HBL has got itself into lollapalooza kind of situation where not only it’s new growth segment is firing, but it’s supposedly “low growth” largest contributor, industrial battery segment is also doing superb. Company is now raising 150 cr. to meet it’s working capital needs, which is in line with what mgmt. has been guiding.

Disc: Hold from ~100 levels. Have added more after Q1 results.

| Subscribe To Our Free Newsletter |