Following this.

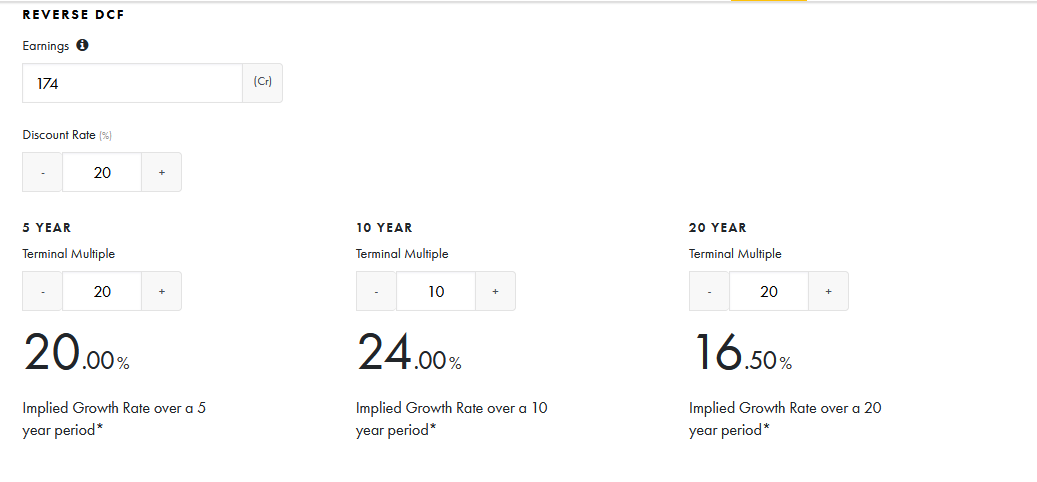

I just did the Reverse DCF for Gokaldas after the ~38% jump in share price over the past 2 days.

Used TTM PAT as the Earnings input (which is a conservative estimate only as net PAT over past 5 years divided by net CFO over the 5 years is 49%). Assuming that I wish to make 20% CAGR over the next 5 years, the implied growth rate still comes out to be 20%.

With the increased number of FTA agreements in discussion and likely to be concluded over the next few years, would it be fair to say that Gokex is still fairly valued?

Disc: Invested and Tracking. Noob alert.

| Subscribe To Our Free Newsletter |