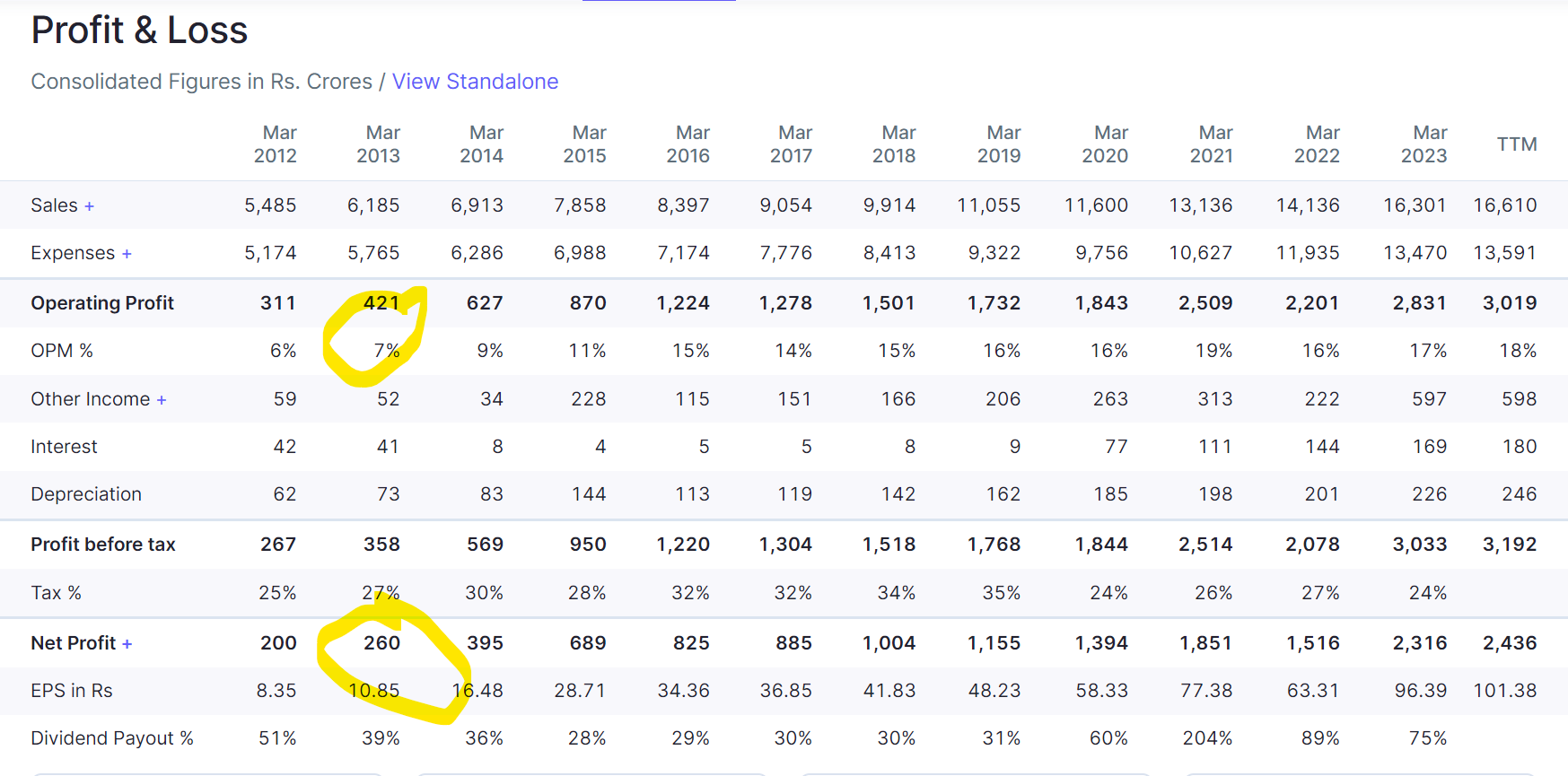

The opportunity in BSE.

BSE is a special situation (Management change). Mr. Sundararaman Ramamurthy joined BSE on 4th Jan’23 and by 7th Feb, he started the first ever post Q3 result concall and handed most of it single handedly. He is an old seasoned hand at exchange business, having served 20 years in senior leadership role at NSE. Could his entry be similar to the Varun Berry episode for Britannia ? Let’s explore the possibilities !

Varun Berry joined Britannia in Feb 2013 as vice president & COO and was appointed as MD in April 2014. The rest, as they say is history.

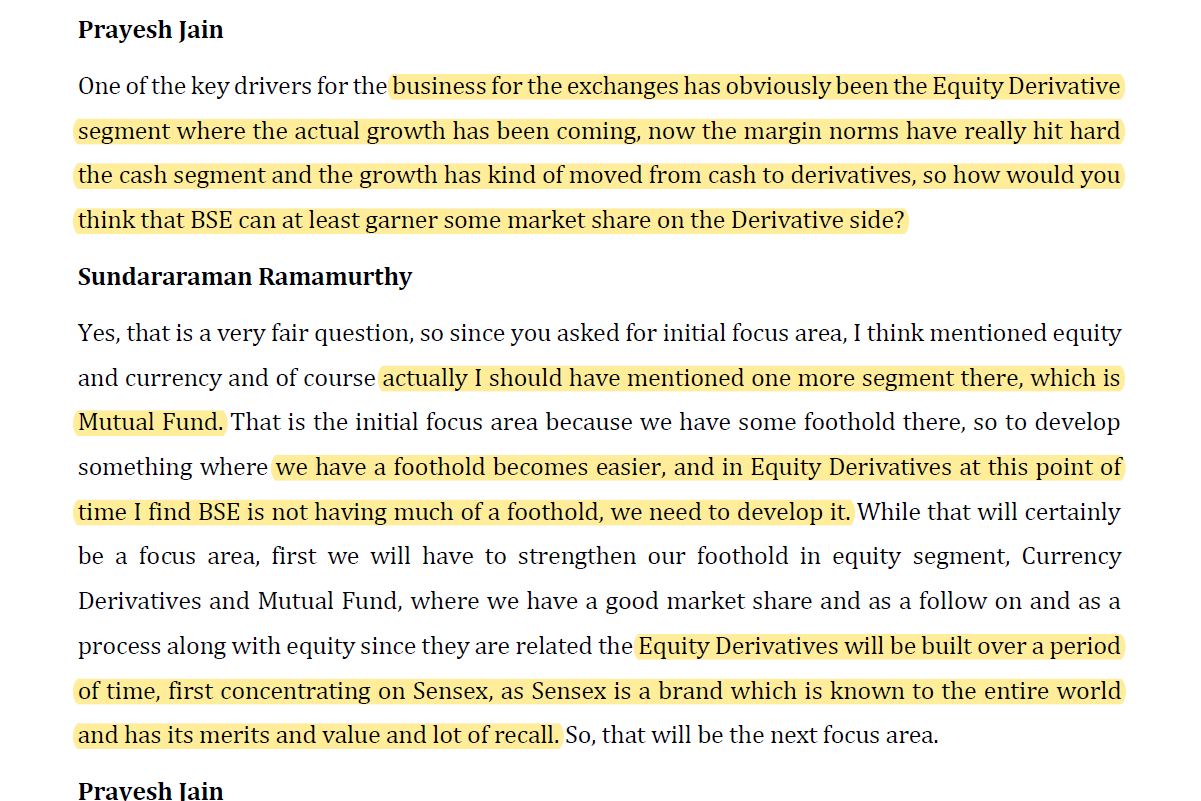

BSE has been losing market share in cash segment since years and held just 7% share at end of last year. It’s derivatives segment was a non-starter and never took off. It’s major saving grace or growth engine was it’s star-MF platform which held 50% market share. Trouble is, derivatives are the mainstay of income for exchange business and there was no mgmt. focus on this segment till that point. Even in the first call, when Mr. Sundar was asked for his 3-4 top priority, derivatives was not in the list and it seemed like an after thought as he referred to it later in the call.

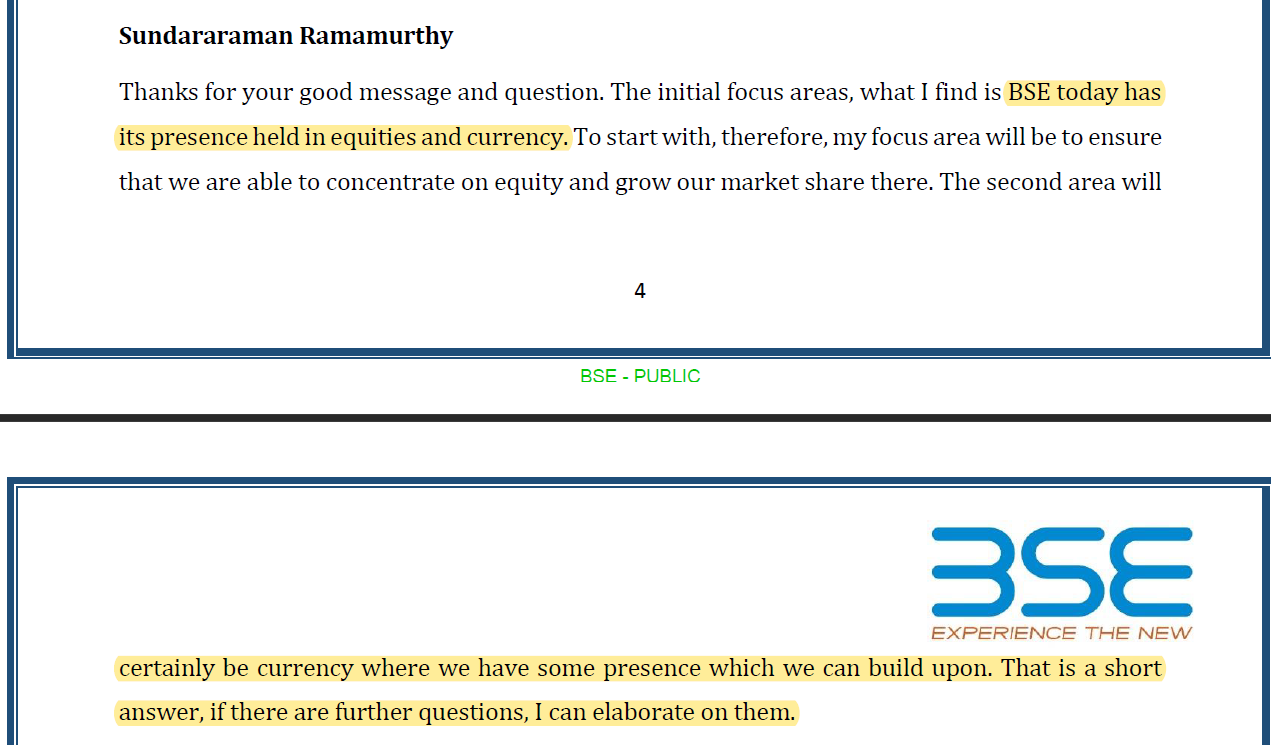

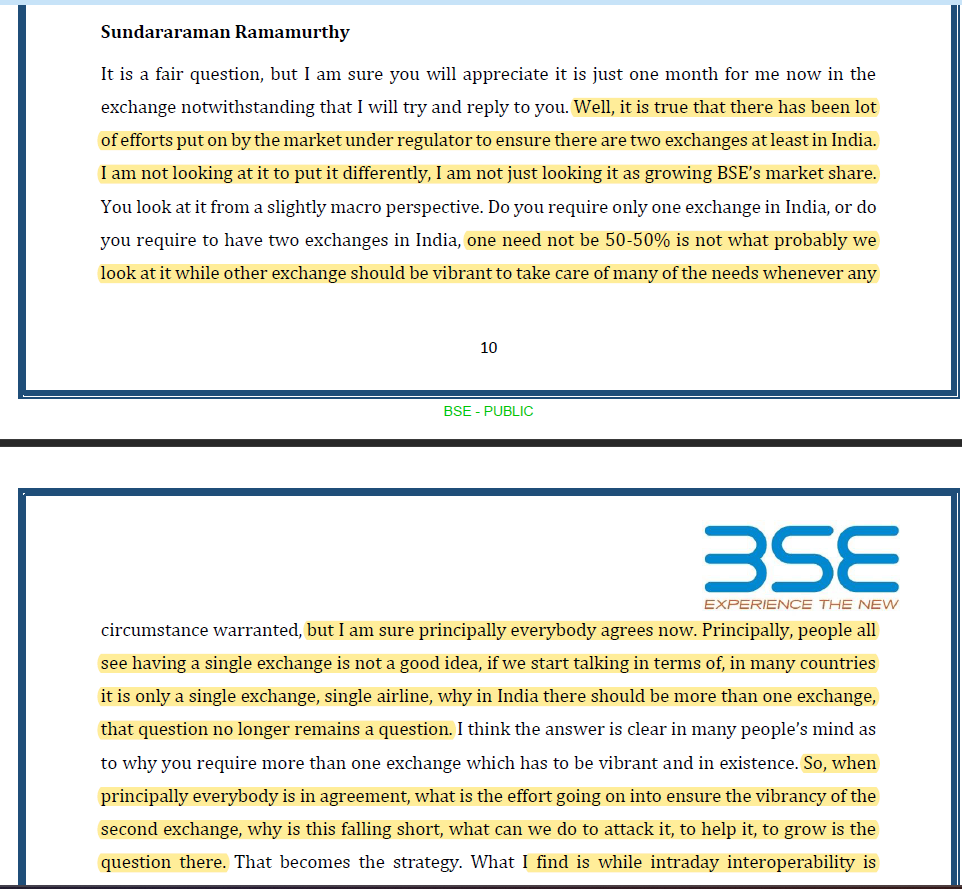

However, one thing came clearly even in that very first call, the power that be, don’t want India to be a single exchange country. 2 thriving exchanges is in best national interest

This point has been reiterated by Mr. Sundar as well as SEBI Chairman on different forums (as shared other posts in this thread).

Both of them also referred to multiple steps that will be taken during the course of time to improve the situation for BSE. Let’s explore the steps taken so far and what might be already cooking in the background.

Step No. 1

By the time of Q4’23 call Mr. Sundar had got his priorities refined. Not only equity derivatives featured in his top 3 list, but he had already re-launched a revamped derivatives segment having done all the background work on this in the last quarter.

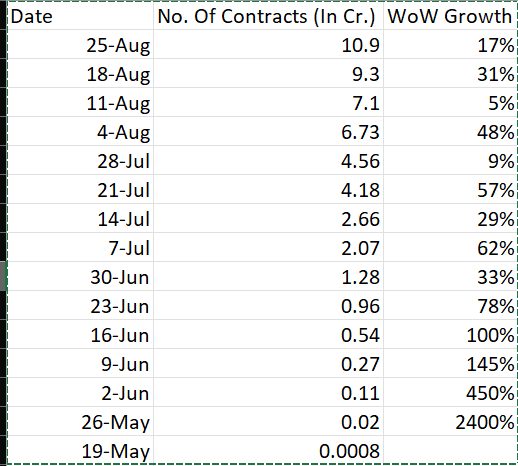

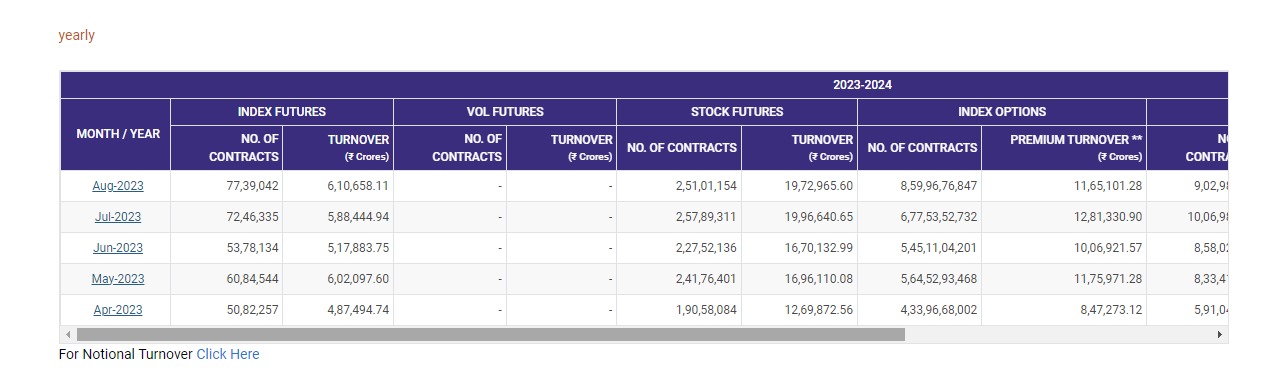

To his credit, it’s been showing result and how ? Just in 3.5 months since launch, BSE has done volumes which are 3.5% of NSE’s volume. That’s remarkable, specially, given how they are doing in cash segment.

Last column stands for Week On Week growth.

HDFC Sec report estimates that by FY24 end BSE could reach 10% market share. i,e, ~3x current volume in next 7 months. Even today, not all major brokers have enabled the BSE derivatives trading. There is backend work that is required to be done by software vendor and then brokers to enable the processes for the derivatives trading. For example, Kotak just started last week https://twitter.com/kotaksecurities/status/1695000451534696596?s=20

and then there is the most important part, where participants want to see the volume before they join the bandwagon. Then at some point the network effect takes over I guess and it’s more a hard sell. Given all this background i think the results so far are nothing short of outstanding. Management deserves kudos for it.

In Q1’24 call, BSE said that they did a revenue of about 26 lacs for the week of 4th Aug in which they did 6.73 cr. contracts. This is while they are charging 1/7th the price of NSE (as per HDFC Sec report). NSE gets nearly 10,000 cr. revenue from this derivatives segment, with option derivatives accounting for nearly 99% of the derivatives volume.

So one can imagine the possibilities.

Step 2:

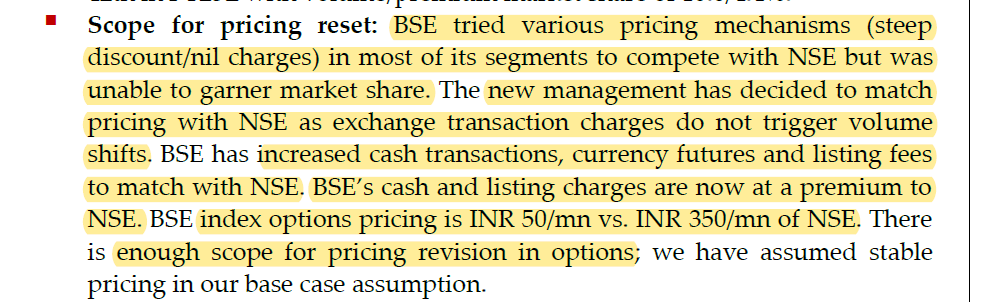

There is a new found aggression on the pricing front. BSE no longer wants to be the poor cousin of NSE and charge less for everything.

Example ? This is from HDFC Sec report.

Also, see this,

In fact I got this clarified in the Q1 call, and this was the response. They have about 70k AP’s on their system and this straight away adds about ~15% of current bottom line. IMHO there isn’t any commensurate additional expenses for this. It’s just a toll which both exchanges decided to extract and the AP’s are just price takers. Some of them drop off, but others will swallow it as cost of doing business.

So at some point that will charge appropriately for the derivatives too

Step 3:

Having tasted success with this Sensex options, now the aggression is visible even in bankex

Best part, the mgmt. suddenly seem to be listening to participants voice and doing changes as a market player should do.

What could be future steps ?

Step 4

He has been batting for intraday interoperability for sometime now. My understanding is this could give a boost to volumes in cash segment for BSE.

All this for a price of ~14k cr Mcap. Of course they also hold nearly 15% of CDSL which is valued at ~12k cr. Mcap and some cash on books. NSE did an EBITDA of 10,426 cr. for a revenue of 12,765 cr. in FY23. The derivatives volumes in FY24 are just going through the roof for NSE too. nearly doubled since beginning of the year.

Step 5

Focus on SME listing ?

Disc: Invested from 550 levels and have added more along the way .

| Subscribe To Our Free Newsletter |