My notes of 1st August 2023 concall

- Revenue Guidance:

- Revenue for the year is maintained between INR 5,500 crores and INR 5,600 crores.

- Margins are expected to be around 16%.

- Order inflow guidance is revised to INR 7,000 crores to INR 8,000 crores due to project award delays

- Approximately INR 2,000 crores are expected from sectors other than highways, such as railways and metros.and a reduced order guidance.

- The goal of achieving INR 10,000 crores revenue over the next 3 years.

- Revenue Breakdown:

- Ganga Expressway project contributed around INR 475 crores in Q1 FY ’24.

- Existing HAM projects contributed approximately INR 500 crores in the same period.

- Clear focus on contributions from the Ganga Expressway project, SPVs, and NHAI EPC projects.

- Revenue Composition for Future:

- Projected contributions from HAM projects and non-road sector projects remain largely the same.

- Monetized Asset Approvals and Inflow:

- Approvals for the monetized assets with KKR are in progress.

- Two projects with CODs are already with the finance department for in-principle approval, with the third project expected to follow soon.

- The finance department typically takes around 7 to 10 days for in-principle approval.

- Despite a recent delay due to NHAI organizational changes, the inflow is expected by October or November.

- Project Pipeline and Awards:

- The company aims to achieve around INR 4,000 crores to INR 5,000 crores of project awards from NHAI.

- Awards from MSRDC and other sectors will contribute to the remaining projects.

- Specific mention of participation in the Pune Ring Road tender and expectations of award by October or November.

- Railway Opportunities and Capabilities:

- The company is actively participating in railway projects, including permanent track linking works.

- Opportunities are seen in Maharashtra, Gujarat, and Uttar Pradesh.

- Collaborative ventures and MOUs are being explored for railway projects.

- Railway station redevelopment projects are also considered for bidding and participation.

- Equity Requirements and Bid Pipeline Overview:

- Equity requirement for next 3 years: FY ’24 – INR 407.4 crores, FY ’25 – INR 268 crores, FY ’26 – INR 158 crores.

- Bid pipeline: Strong pipeline for MSRDC projects (INR 30,000+ crores qualified), NHAI projects (INR 45,000+ crores active), railways, and metro.

- Working Capital:

- Working capital increased temporarily due to delayed payments from SPVs and clients, but expected to return to usual levels.

- Asset Monetization and Debt Reduction:

- Expected reduction in debt by INR 200-odd crores by year-end.

- New capex may add INR 60-70 crores to debt during the year.

- Projected debt range: INR 425 crores to INR 450 crores by year-end (excluding asset monetization).

- Order Inflow Guidance and Bid Pipeline

- The company aims for INR 7,000-8,000 crores order inflow this fiscal year.

- Limited order inflow received in H1 with challenging Q4 ahead.

- Around INR 5,500 crores outstanding bids expected to open soon.

- Estimated INR 1,000-2,000 crores potential from ongoing bids.

- Bid pipeline includes INR 1,50,000 crores projects.

- Targeting to bid for INR 90,000 crores projects.

- Historical bid strike ratio of 7-8% gives confidence in achieving target.

- Bids to be completed in Q2-Q4 for substantial future opportunities.

- Operational Efficiency and Equipment Utilization:

- The company has strategically invested in construction equipment, contributing to operational efficiency and margin improvement.

- The new equipment has led to reduced dependence on external vendors, translating into better control over operational costs.

- The equipment utilization rate has been decent, and the benefits of internal strategic investments are being realized.

- Margin Expectations and Revenue Breakup

- The company has guided for 20% to 25% revenue contribution from the non-road sector in the annual report.

- There is a cautious approach in bidding for projects outside the highway sector, with a gradual expansion plan over three years.

- The aim is to be selective and avoid desperate bidding, which is intended to help maintain similar margins.

- There is confidence that maintaining margins will not be a significant challenge even as the non-road order book increases.

- Competition Intensity and Project Mix

- The competitive landscape in the industry has seen a correction in recent months, with a decrease in the number of bidders for projects.

- The number of bidders in EPC projects is still high, ranging from 35 to 40, while in HAM projects, it’s around 7 to 8.

- There is a cautious approach to bidding, with an emphasis on avoiding margin shrinkage and compromising on profitability.

- Despite the competitive environment, there is confidence that the company can target the goal of adding around INR 5,000 crores worth of highway projects without compromising on margins.

- The target for road inflow is expected to be a mix of around INR 2,000 crores from EPC projects and the remaining from HAM projects.

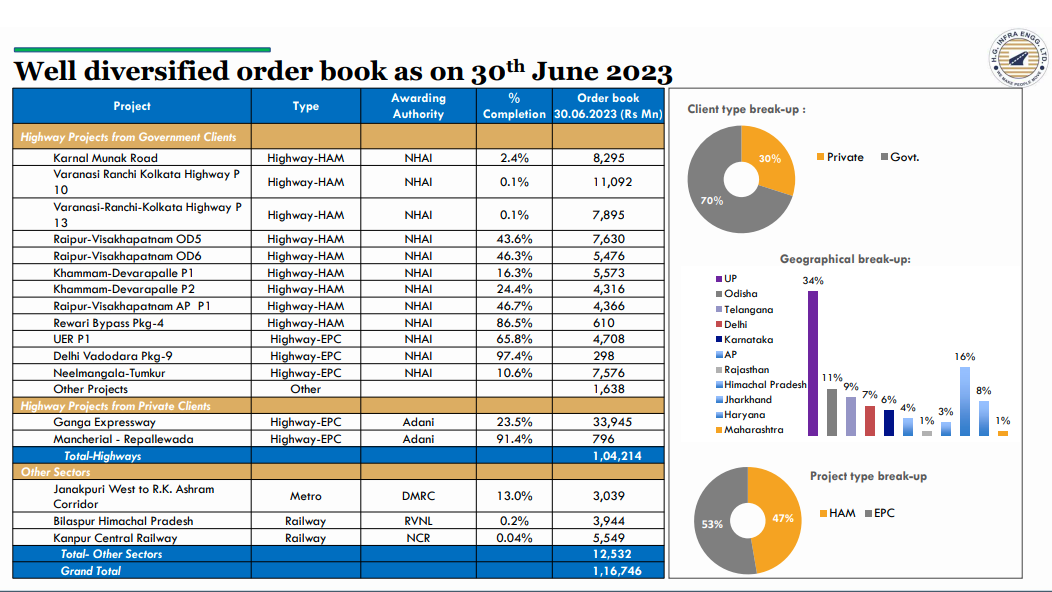

Project statuses:

| Subscribe To Our Free Newsletter |