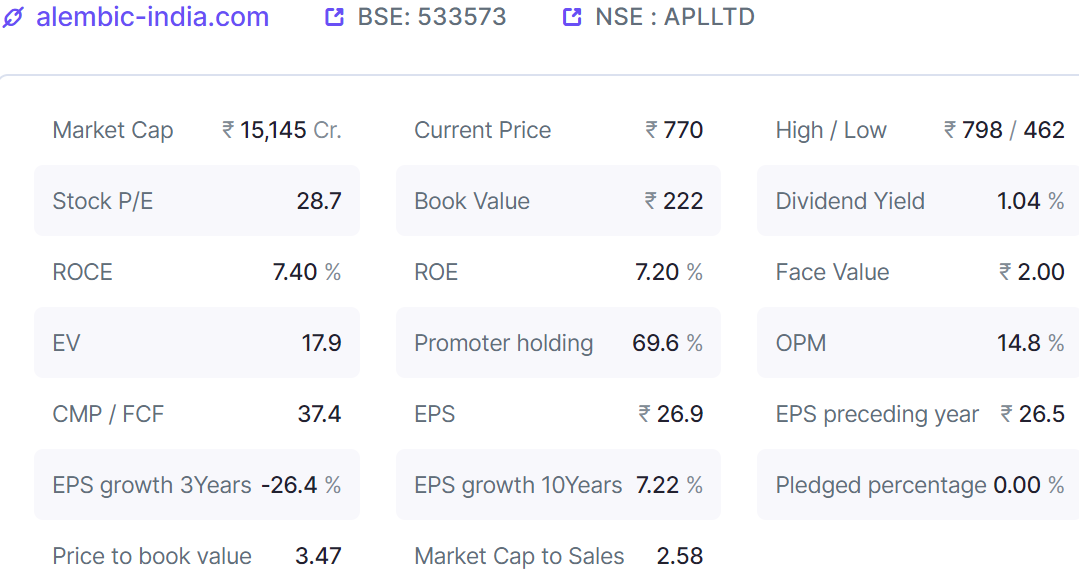

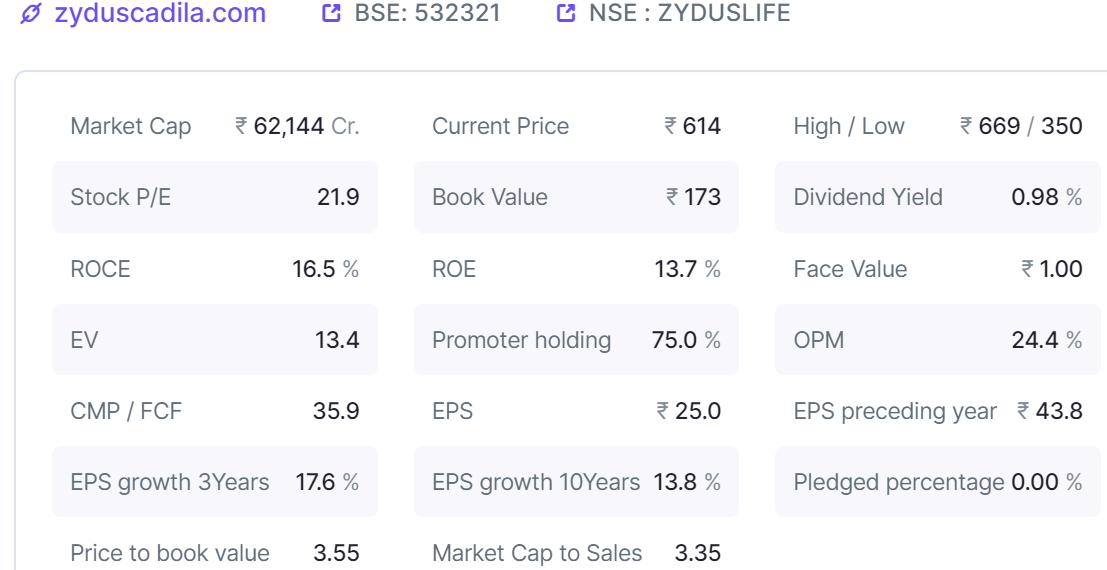

Hi Harsh, Why Alembic Pharma and not Zydus Lifesciences? Specially given that the promotor of Alembic Pharma does not seem to have the highest standards… Over 10Yrs EPS growth has been higher for Zydus, its OPM and ROCE are both higher. Promotor stake is also higher… Valuation wise also Zydus is not that expensive given its higher profitability ratios… Market cap to Sales of 3.35 over Alembic Pharma’s 2.58; and if one compares EV/EBIDTA its lower for Zydus at 13.4 over Alembic’s 17.9

Do you anticipate Alembic to do much better from now on? I frankly have not studied their launch pipelines which I agree may have a much bigger impact in the medium term; but still for a long term investor the above ratios should be more important or am I missing something…

| Subscribe To Our Free Newsletter |