Some info from Lincoln Pharma Annual report, as well as from Screener.

●Growth in sales/ PAT every year

● Exports growth from 25.5% ( 2013 ) to 57.5% this year

Uploading: Screenshot_20230906_184801_Drive.jpg…

● Aim to expand network to 90+ countries from current 60.

Uploading: Screenshot_20230906_185522_Drive.jpg…

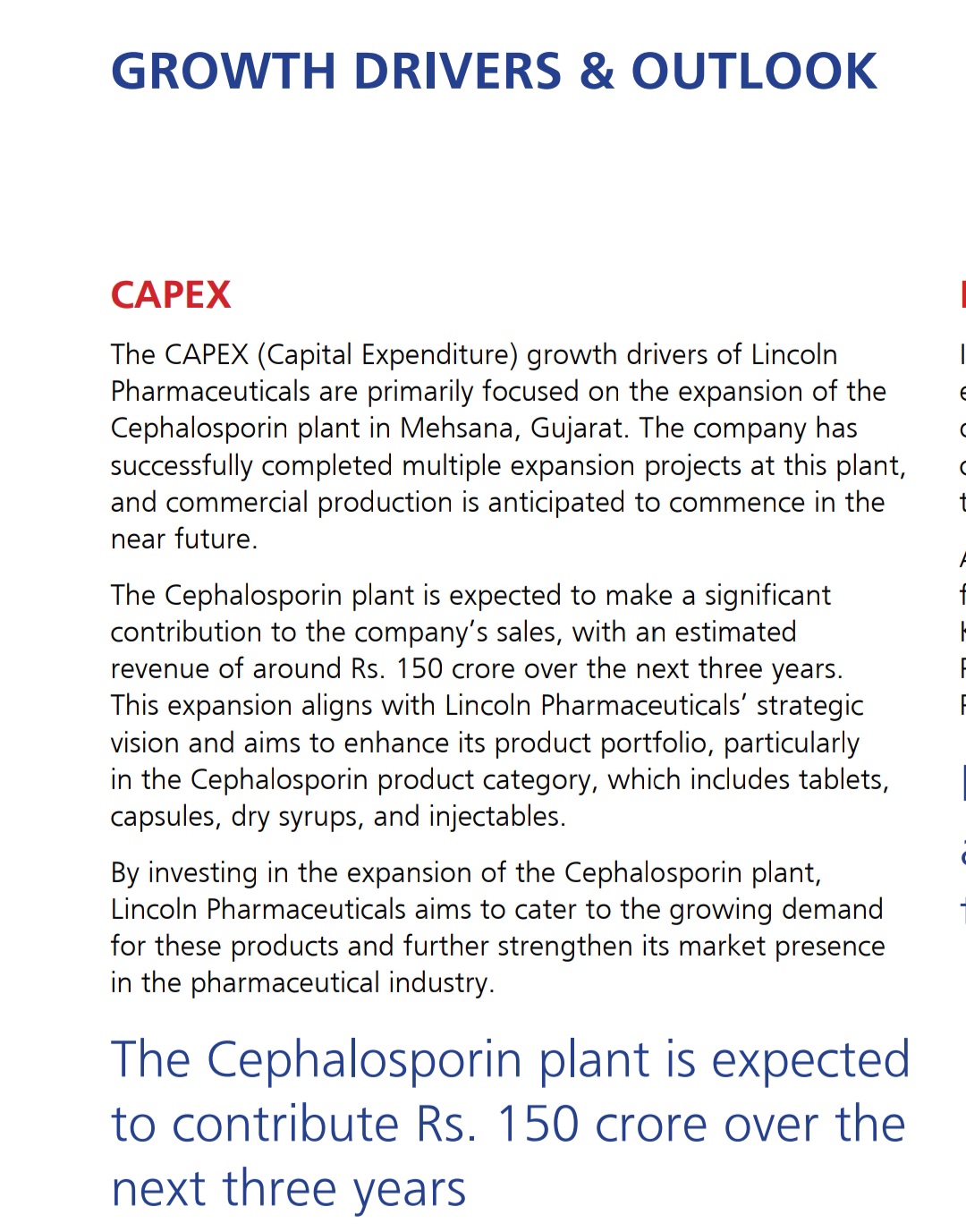

Target to achieve 750 Cr. Topline with better margins by FY26

Uploading: Screenshot_20230906_185917_Drive.jpg…

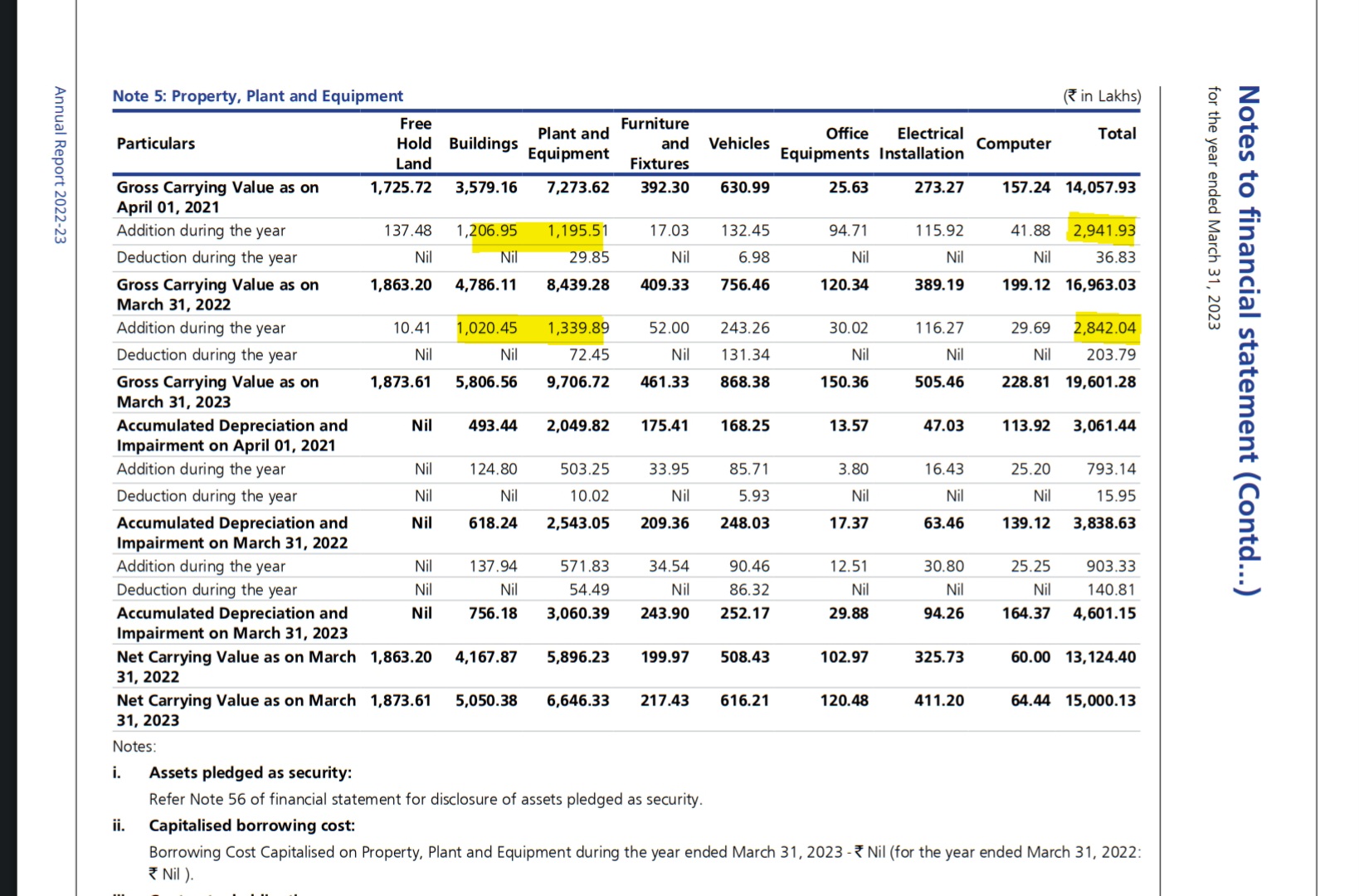

● About 60 Cr. Capex in last 2 year

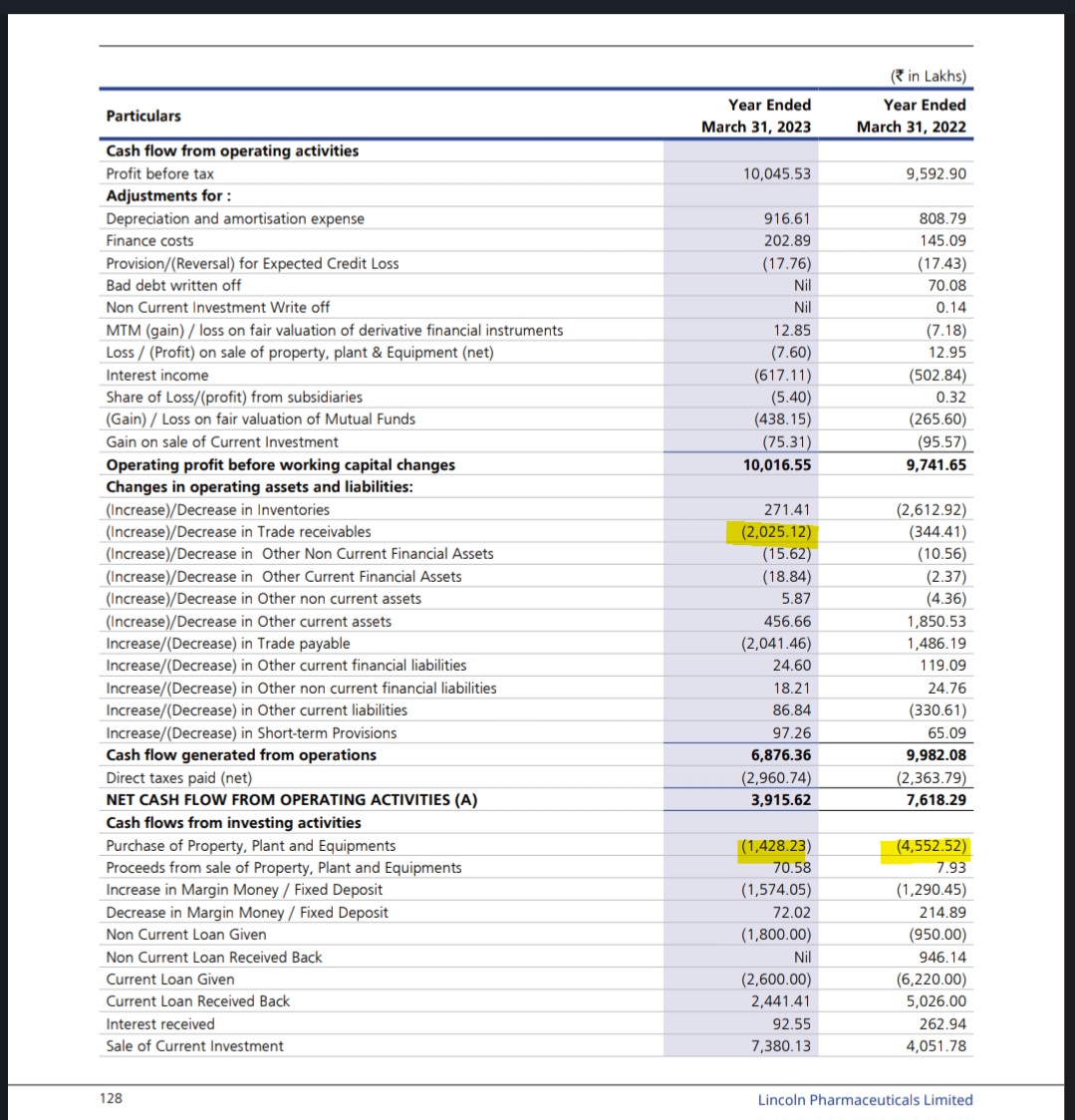

● CFO FY23: 68 Cr. Vs 99 Cr. last year – increase in receivables

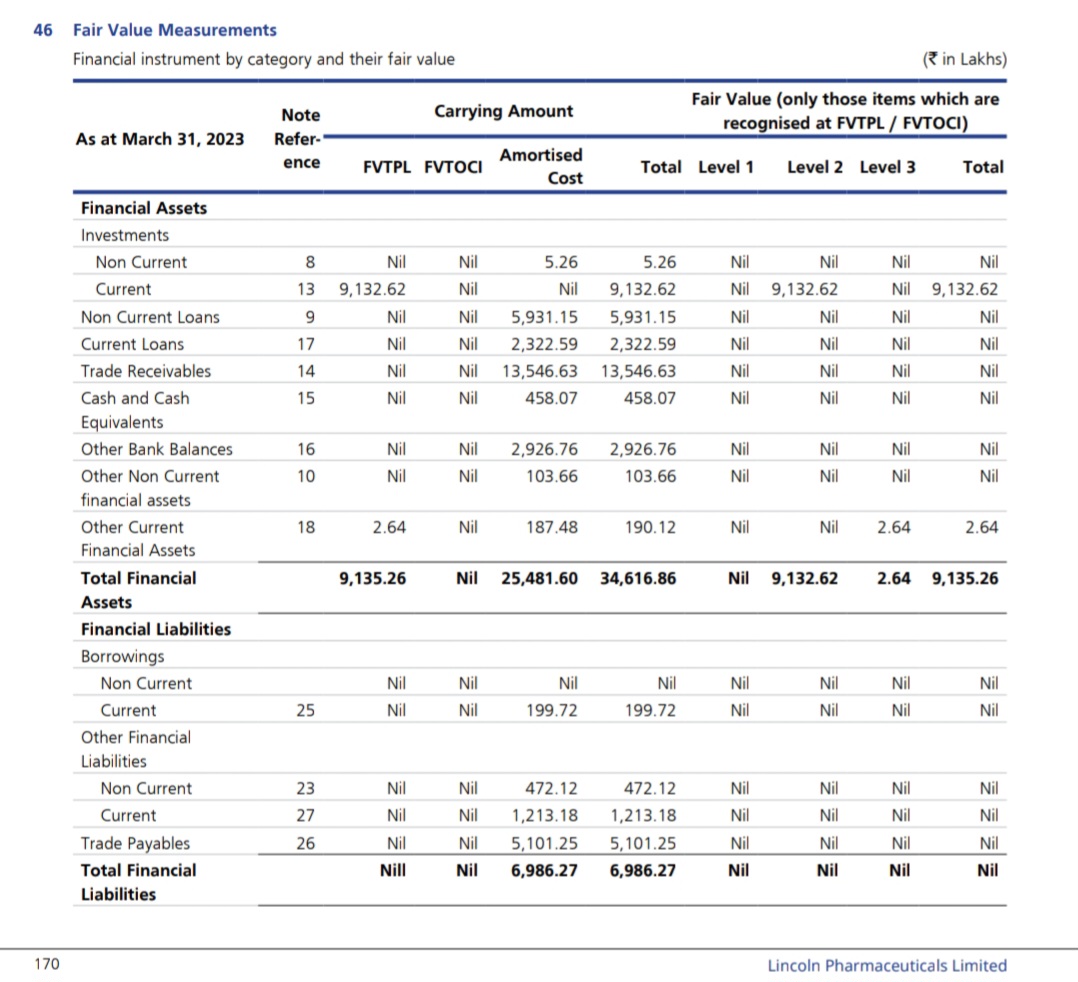

● Debt free,

Mutualfund/ cash/ Equivalents of about 200 Cr.

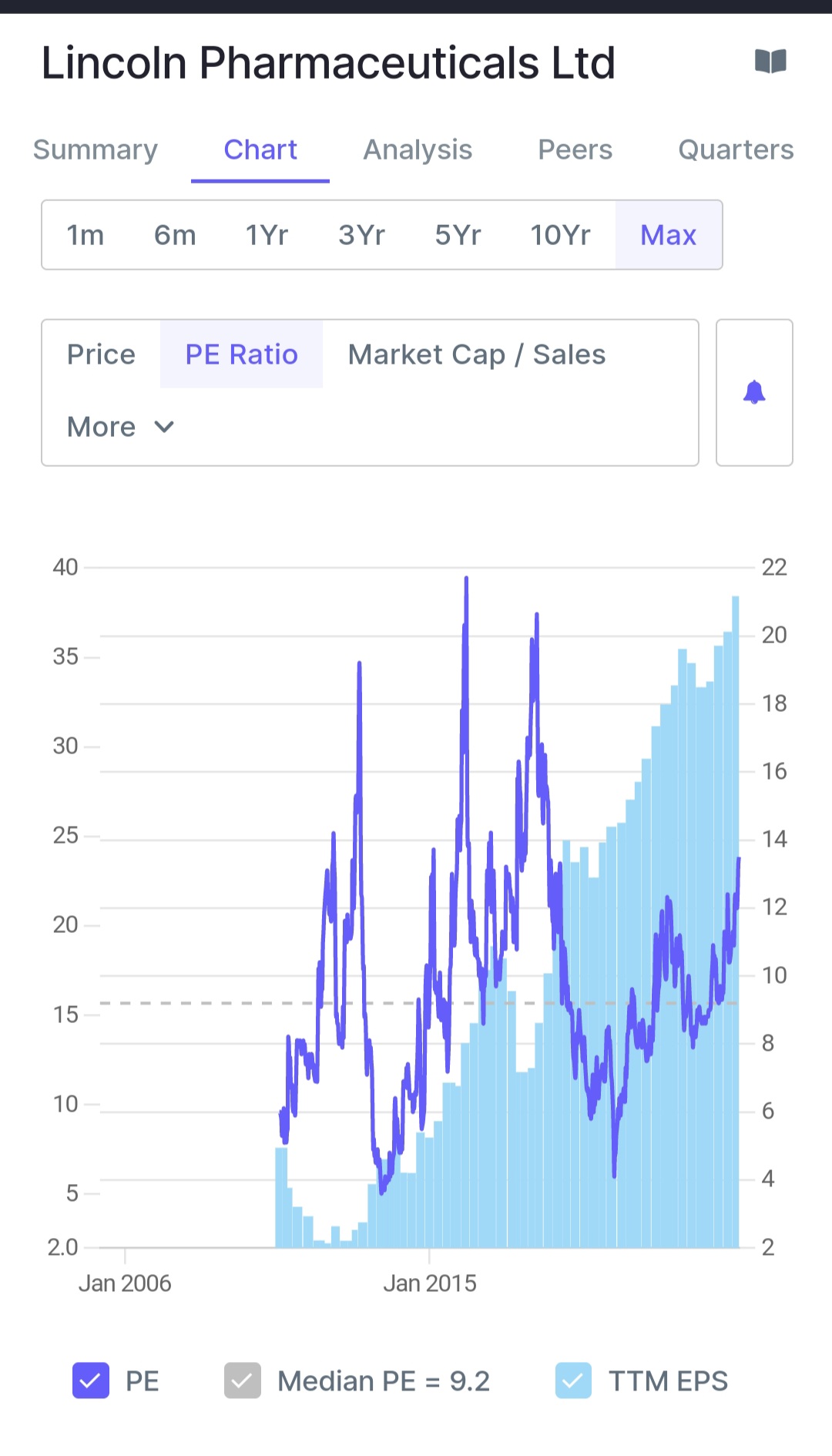

Screener data: Lincoln pharma traded at

PE of 20-22( FY ’12,’15 &’18 peak) Current PE=13

FY’26 guidance: 750 Cr sales.

with operating leverage, they may get to 125-150 Cr PAT

Current Mcap: 1000 Cr.

If it reaches to its peak valuation in PE terms? In that case, it may get to 2500-3000 Cr. Mcap. by that time ( FY 26 )

Possible?

Disc: Invested, biased view.

I am not sebi registered. Do your own research

| Subscribe To Our Free Newsletter |