The company has done exceedingly well – way beyond what I expected them to do.

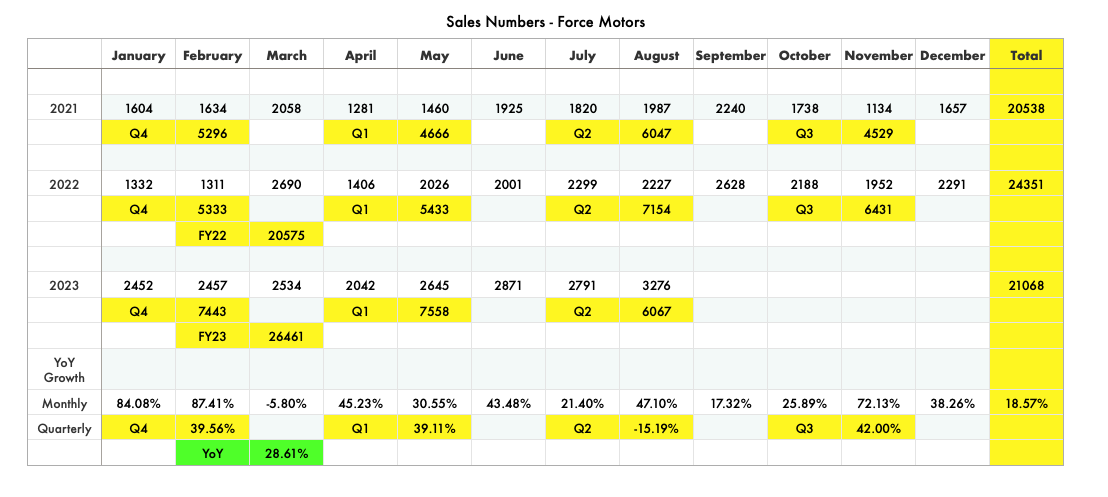

Still operating leverage is yet to play out – in last quarter, ebitda margins improved because of expansion in gross margins. As the capacity utilisation has improved in current quarter and fixed costs remain the same, margins can improve further.

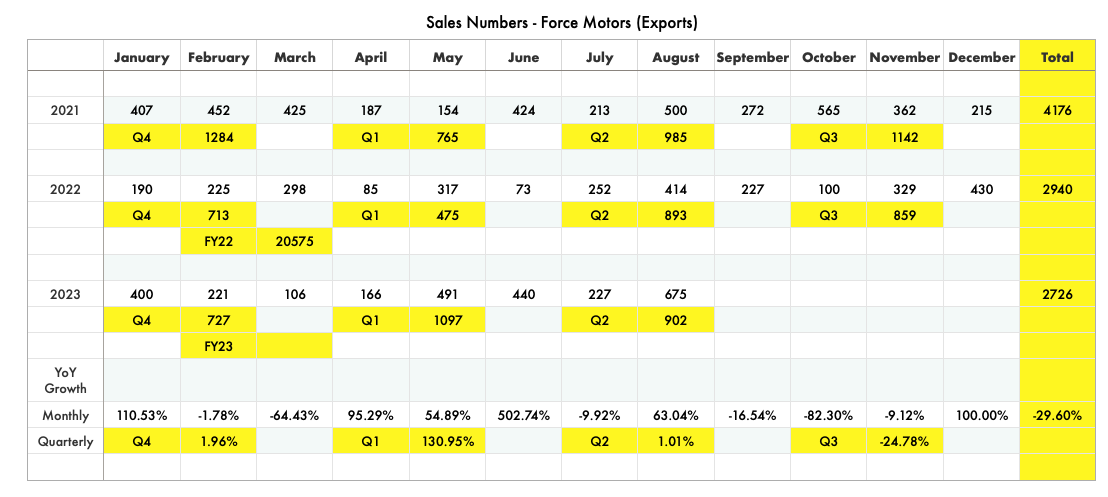

Note – these numbers are ex-Gurkha as they are yet to launch BS-VI Phase 2.0 variant of Gurkha, by september end it will be in their dealership stores most likely.

Their export sales are at highest level since Jan-2021.

Q2 can be bumper as they are only 1500 short of their Q1 sales figure in just 2 months.

I won’t be surprised if the stock gets rerated again as commentary is bullish in the annual report also.

D – Invested from 1100-1200 levels, no reco.

| Subscribe To Our Free Newsletter |