From the Q1 Concall, And Annual Report, Some of the growth drivers as per management are –

- Focus on marketing in Africa to tap the business from minerals mining customer’s

- Additional business from OEMs across the world, particularly from the 5 OEMs in Europe from whom they are seeing good opportunity.

- Continue to build on the turn-around that have happened in MHE division to improve margins

- New opportunities from Defense for gears required in marine engineering

- Benefit from the capex taking place in Power, Mining and Minerals, Steel and Cement sectors in domestic market. Govt of India have made good number of allotments for the mines over last couple of years. Subsidiaries of Coal India have plans to execute several new projects(which looks likely given surging power demand due to buoyant economic activity in country).

- Potential foray in manufacturing gears required for Metro as well as Looking out for opportunities in mechanical power transmission drive.

- Develop new products with investment in R&D for the existing customers

Being debt free and having about 250 Cr. cash in hands will help the company to take up new opportunities. Their capacity utilization being 76% percent and plans to improve sub-contracting percentage to deliver increased business to keep capex only in range of 10-20 Cr. will improve the return ratios and profitability.

Disc-No investment as of now.

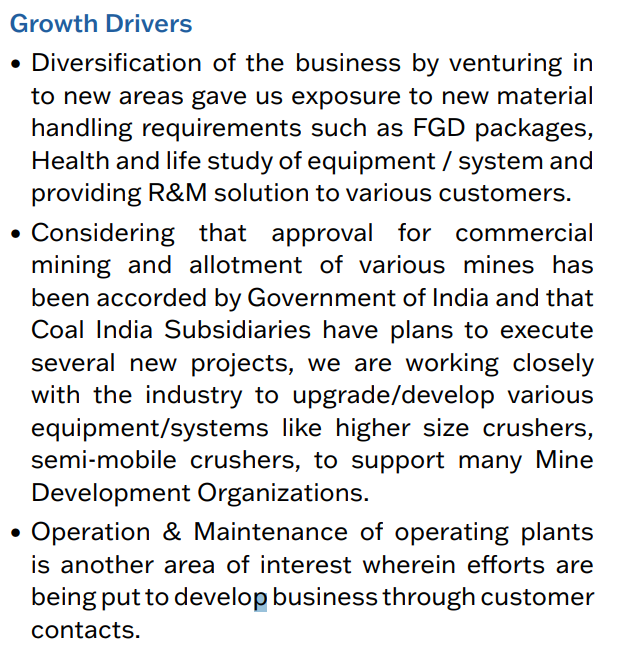

Snippet from Annual Report –

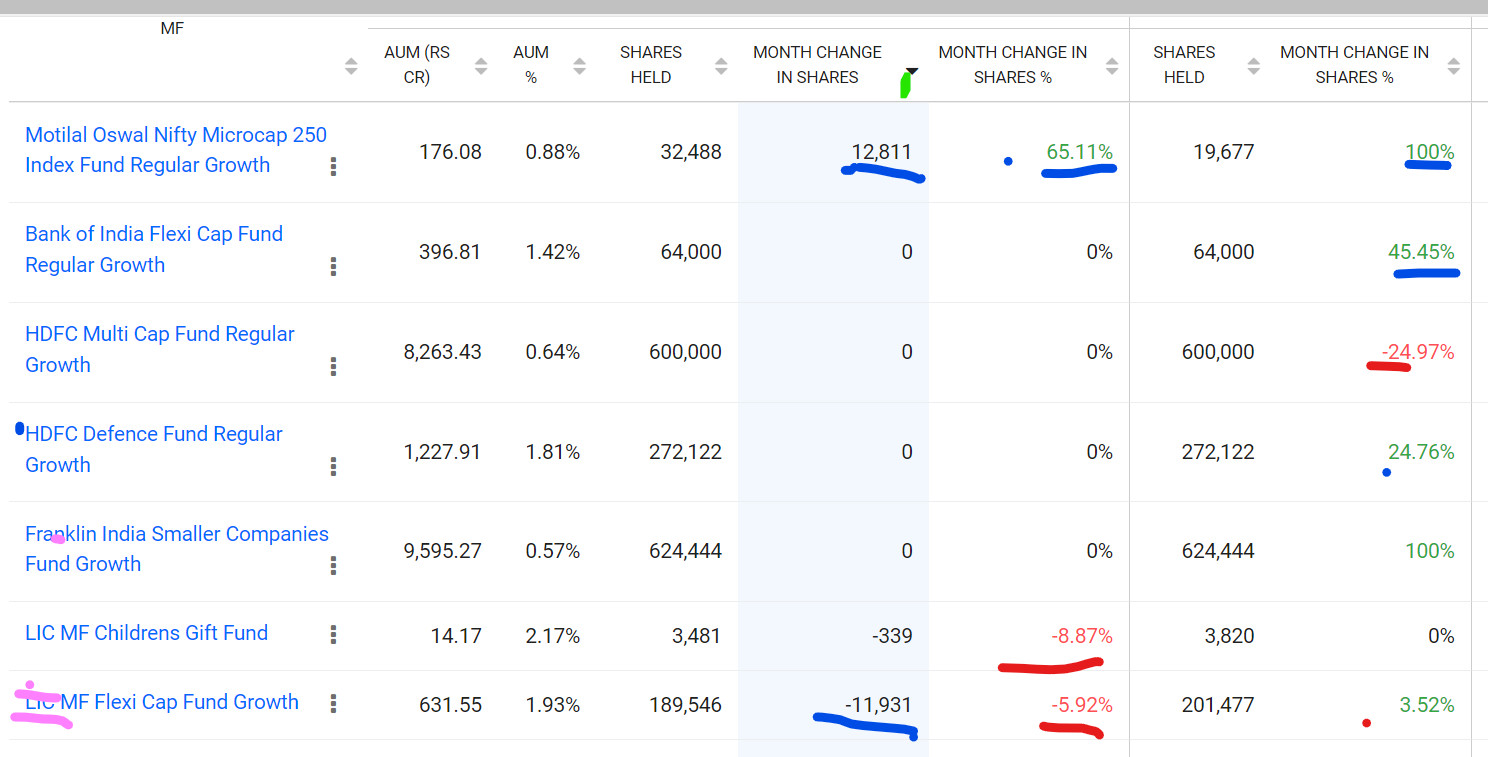

Decent amount of mutual fund buying during Jul’23

| Subscribe To Our Free Newsletter |