MY TAKE ON RADIANT

INDUSTRY

-

The current internet penetration rate in India stands at 57% and this largely corresponds to the metro and semi-urban internet users. The majority of the population in rural areas lack basic network connectivity and hence do not have access to Digital banking/online payment systems. People in these areas rely predominantly on cash owing to a lack of network support for cashless transactions.

-

The top three players, of which Radiant is one, account for more than 75% of the total market share of the RCM market.

-

The RCM market was estimated at ₹ 6.8 billion in Fiscal 2021 and is projected to reach a market size of ₹ 20.4 Billion by Fiscal 2027, growing at a CAGR of 20.3%.

-

The growth in the organized retail sector as well as the corresponding outsourcing potential is expected to be prime factors for the development of the RCM market in India.

-

Cash utilization and circulation in tier 2 and tier 3+ towns and cities are expected to grow, on account of the government’s financial inclusion programs, including Pradhan Mantri Jan Dhan Yojana and other direct benefit transfers, provide direct benefits and subsidies to populations in semi-urban and rural areas.

-

The cash management services market has tremendous potential to be exploited in areas like retail cash management.

- The country has over 30 million retailers, and only 10% of them are members of the organized sector, and approximately 15% of retailers in the organized sector use retail cash management services. As the unorganized sector exempts itself from consuming RCM services, the market for retail cash management is significantly underpenetrated in India as compared to advanced economies.

-

the outsourcing of cash management services is expected to also be driven by public sector banks increasingly outsourcing their cash-in-transit services to increase their productivity and reduce costs.

-

Despite the rise of digital transactions in developed countries, cash usage continues to rise, which is more typical of the market scenario in an emerging economy like India

-

is present in approximately 60,000 outlets today. As per industry estimates, the entire industry is picking up from less than 1.5 lakh outlets. But the potential market is huge with over 30 lakh outlets eligible to use this service.

THESIS

-

Very low float, hence if there happens to be some institutional interest it could rush up

-

This year there will be capex, otherwise they lease vehicles to grow Also there is sufficient opt leverage still available, so money should be given out as dividends later, mgmt also said they will be a strong dividend-paying company

-

The retail touchpoints are growing rapidly in TIER 1 and 2 because e-com, e-com, and e-com logistics are growing pretty rapidly in tier 1 and 2 first, and also after capturing tier 1, should go for tier 3 and 4, when that happens revenues from NCM will increase, and NCM being high margin will increase the overall margins

In e-commerce logistics, even in Tier 1 locations, 50% of the transactions are cash on delivery, and that goes up to 90% in Tier 4 locations. So that’s one of the key drivers.

- In the cash logistics industry, a key marker of profitability is the ability to maximize the touch points per route, thereby maximizing the revenue derived from each trip while the overall costs for such routes remain largely constant. Thus, the ability to increase route density by adding more touchpoints will lead to operating leverage will lead to improved profitability from each route

As the % of direct clients increases, operating leverage should increase, as this will be like adding additional clients on the already developed road infrastructure, and so the fixed costs have already been incurred as volume increases margins flow to the bottom line.

- DBJ- They have calculated the Jewelers at about 135000 and currently, this service is being offered only to about 10,000 of them. So it is again a very large market opportunity

- are already doing cash management for 1000 of such outlets.

- The largest player in the segment is functional out of some 83 locations. While Radiant already has a presence in over 6,000 locations across the country

- The diamond, Bullion, and Jewelry, industry size is bigger than the RCMS segment.

- Almost 60% – 70% of this segment is unorganized.

- The DBJ touchpoints have not been added to the 1000-per-month touchpoint targets, which will further help increase the reach for the RCM segment too.

- DBJ revenue is expected to scale up from Q3 onwards.

- This quarter there was an increase in hiring for the above- vehicles, gunmen inc, and cash exec, so the overall cost increased,

That is why the margins were low, but should revert soon

-

Are adding direct clients every quarter, which should also help reduce client concentration a bit

-

An estimated 30 to 40 lakh outlets are eligible to use a service of this nature. But the entire industry is catering to 1.5 lakh outlets. So which means an extremely underpenetrated sector. As banks continue to offer this as a service to more and more end customers, they should continue to keep giving Radiant more points.

-

-

Network cash- NCM is high margin

Network cash management is more relevant where the banks do not have their branch presence.

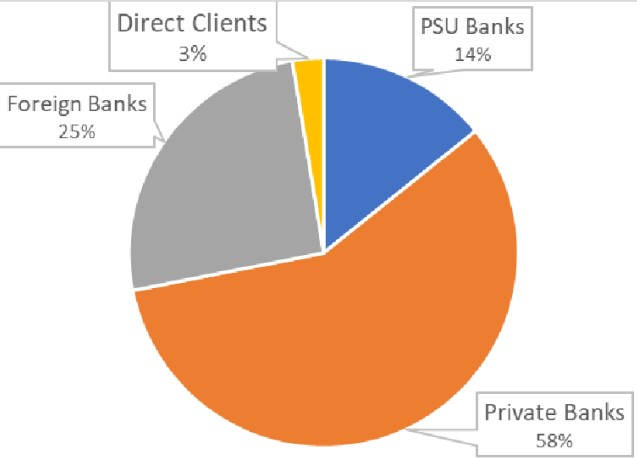

Foreign banks have limited branch presence, so almost a substantial portion of their revenues go through Radiant’s account. So Radiant gets to charge for network cash management.

The share of foreign banks will be one of the levers. Foreign banks as a % of total revenues was 25% in FEB 23

Second is the share of Tier 3-plus revenues because the branch presence is low, against 61 bank branches per lakh population in urban areas, India has only 6 branches per lakh population in rural areas.

And third, obviously is the volume of cash because that is priced volumetric. The amount of cash that they deposit in their account is directly correlated there.

- As a result of the increase in e-commerce penetration in tier 2 and tier 3+ towns and cities, e-commerce logistics companies are also expected to see resultant growth in volumes. In India, COD is the most popular way of payment for e-commerce retailers. COD accounted for more than 60 percent of all e-commerce payments in Fiscal 2022.

ANTITHESIS

-

The contracts they enter into with the customers do not contain price escalation clauses, and as a result, they are faced with risks concerning inflation.

-

As the capex and hiring for the DBJ segment has been done, if sales do not pick up Q3-4, opt leverage is a double-edged sword, radiant can be impacted

-

If cash volume reduces, ncm and cash processing directly take a hit, as here revenues are volume-based.

-

Payment options other than cash, including credit cards, debit cards, POS terminals, Stored value cards, UPI, and mobile payments have increased significantly in India in recent years, and a continued shift in consumer trends in India concerning the use of cashless payment methods could result in a significant reduction in the use of cash as a payment method.

-

The insurance claims below can also be rejected, or delayed, or the actual amount payable may be more than the insurance amount.

Future insurance premiums may increase significantly because of a high number of claims that they may make, or for any other reason such as increased risk perception of this industry by the insurers or re-insurers. Any such increase could harm their business.

-

-

Although this concentration is reducing every year

-

Since the overall cash management market is very lucrative and yielding, there is a risk of new players coming into the market, well-capitalized MNC players

| Subscribe To Our Free Newsletter |