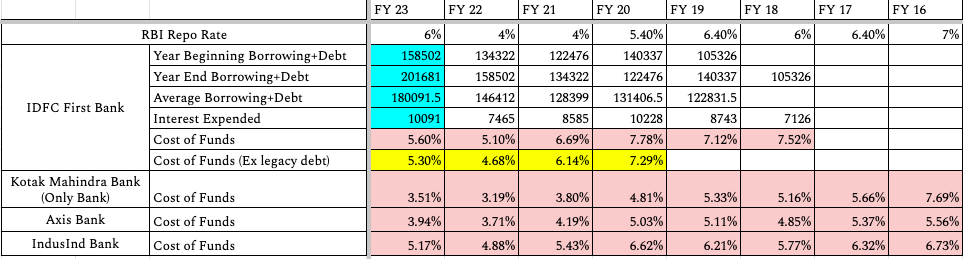

I was studying how the cost of funds at the balance sheet level for IDFCF has evolved since the merger and comparing it with other banks. I have also added the average repo rate prevailing in each FY.

Some conclusions jump out when you look at the last 5-7 years of data:

-

IDFCF has done a remarkable job of getting its CoF down from 7.8% in FY 20 to 5.6% in FY 23. It has been doing this mainly by initially offering a high SA rate to get customers in the door and then offer them good services to get them to stay.

- An underrated contributor to the reduction in CoF has been increase in current account (CA) deposits from 2363 Cr in FY 19 to 14286 Cr in FY 23 – 6x in 4 years.

-

Kotak Bank has been the pioneers of this model of liability building by offering high interest SA + good service + smooth onboarding with 811. We can see how well they have executed this strategy in the table above – ~400 bps drop in CoF in 5 yrs between FY 16 and FY 21. I believe Kotak can be a model of how the CoF can be expected to evolve further in IDFCF in the best case.

-

Kotak was offering 6% SA interest on balances between 1L & 1 Cr till FY 20.

-

Despite a ~400 bps drop in cost of funds between FY 16 and FY 21, Kotak Bank didn’t

expand its NIM. NIM stayed at ~4.4% between FY 16 and FY 21. Presumably, the bank

migrated to lower yielding but safer assets.

-

-

Axis Bank has also reduced its CoF in last 5-7 years but its drop in CoF has been less than that of Kotak. As a result, today Kotak has 40-50 bps lower CoF than Axis despite having 1/2 the balance sheet.

-

IndusInd however has managed only ~40-50 bps reduction in its CoF in the last 7 years when adjusted for repo rate.

I did not consider HDFC Bank and ICICI Bank because their liability franchises are much older and were built during a different era.

How can this evolve in the future in IDFCF – especially for medium term investors?

-

After the next 18-24 months, once the ongoing deposit wars cool down and bank has built a broad enough customer base, we can expect IDFCF to steadily lower its SA and term deposit rates. This should help the bank reach a sub 4% CoF in due course. A balance sheet level sub 4% CoF (ex-equity) should be considered a benchmark that says you have arrived in Indian Banking – Kotak achieved it in FY 21 and Axis only in FY 22.

-

I see the current marketing blitz by the bank (KBC, BCCI sponsorship, Partnership with cab drivers, increased ads on TV etc) as an attempt to get top of the mind awareness (TOMA). This TOMA should enable the bank to gather granular deposits where it would later be easier to drop the SA rates – similar to Kotak’s strategy.

-

On the asset side, I would expect IDFCF to not pass on this CoF reduction to consumers completely and hence increase NIMs moderately.

Source – Data taken from ARs of companies. I have used standalone statements for Kotak’s data.

Requesting members to kindly share your inputs/feedback.

Disclosure: Invested

| Subscribe To Our Free Newsletter |