Chanced upon the stunning buyback history of the company and couldn’t resist digging deeper into it.

Since the thread here doesn’t contain much recent information (except for Ranveer’s post above), adding some info for anyone interested to follow:

- Listed on both BSE and NSE

- ROE / ROCE are in the 10 to 12 % range but company sitting on lot of surplus cash. Return ratios ex of cash would be higher. About 20 % of PBT comes from Other Income

- Promoter holding is high

- Debt is almost nil

- LT OPM was always 20-25 % range but has declined in FY22 and thereafter to 14 to 17 % range. But Q1 FY24 has again shown a sharp improvement. Management says in H1 FY23 the RM prices were very high and more than offset the gains in the realisation and hence margins have dipped.

- LT sales growth is mediocre but has shown a sharp jump in recent times. Profit growth has also shown sharp improvement

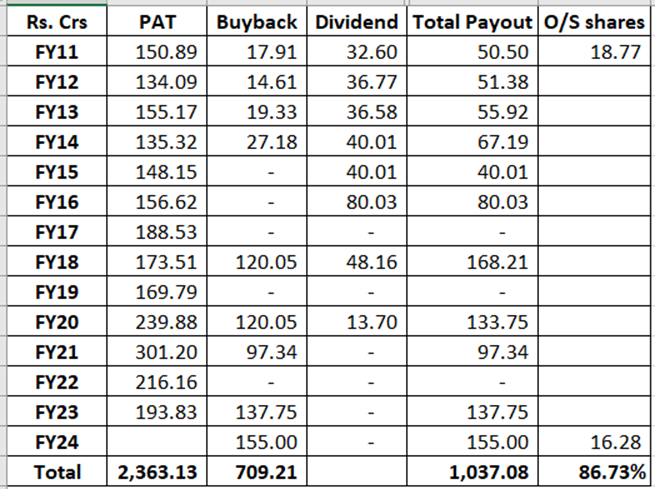

- Consistent buybacks through tender offer route by the company but no dividend payments post 2020

- CFO to PAT is around 85 % in the long term. Okay but not great

- Last major capex was done in FY16. Some capex done in FY22 and 23.

- Working capital requirement is not high, CCC is around 3 to 4 months and W/C days are less than 2 months

- Company’s business can be classified into three divisions – formulations, functional foods and API.

- Key brands are Electral, Zifi, Enerzal, Zocon and Vitcofol.

- ‘Electral’ dominates the Oral Rehydration Salt (ORS) market with a commanding 70% share

- In FY23, Electral earned more than Rs.400 crore, Zifi Rs.350+ crores and Enerzal Rs.150+ crores

- 82 % reveune is domestic and 18 % is from exports

- In FY 2022-23, the growth came from anti-infective, gastro-intestinal and vitamins / minerals / nutrients

- Highlights and key developments in all the three divisions are mentioned in the Annual Report

- There is a seasonality in the business, which is dominated by ORS and anti-biotics. ORS sale begins from Jan and peak in summer (Q1) while anti biotics peak in Q2. Hence H1 is always stronger than H2. Company is making efforts to reduce this seasonality. The new initiatives such as ophthalmology, diabetic – cardio and nutraceuticals will reduce the seasonality.

- The new portfolio is also outside the NLEM which is another advantage.

- Expansion in Waluj plant will commercialize in Nov 24 since it takes around 18 months to get the US FDA approval for the plant.

- Over the years, company has done several buybacks starting from August 2009. Since 2011 from where I calculated the numbers, total payout has been more than 40 % of PAT. This may not be great but the buybacks in the last 2 years have been even bigger, indicating payout distribution of almost 70 % of PAT. If this becomes the norm going ahead, it would be a big positive. Reduction in share capital is to the tune of 87 % in more than a decade.

- Cash balance as of Mar 2023 was Rs.800 crores with the company

- Promoter remuneration has been to the tune of 0.5 to 1 % of the sales, which is okay.

- In FY 2022-23, growth mainly came from anti-infective, gastro-intestinal and vitamins / minerals / nutrients

- The Company says in FY23, they completed the successful registration of I Lube Eye Drops – Polyvinyl Alcohol BP 1.4% w/v + Povidone BP 0.6% w/v in Malaysia. This marks a significant milestone for FDC as it takes its first step into the medical devices segment in Asia

- US FDA recently completed inspection of Roha plant with No Action Indicated report

On the flip side, sales and PAT growth however has been inconsistent over the years. June quarter domestic sales growth was 5.7 % vs. 21 % in March quarter and 28 % in June 22 quarter. Company did concalls in FY22 but seem to have stopped thereafter.

Overall the company is a slow-moving ship but seems to be on the right track. Management is projecting 15-18 % growth in sales and profits in the next 5 years. This forecast is significantly higher than the historical rates. If it materializes, it could be a significant trigger for the business. Need to wait and see.

(Disc.: No positions)

| Subscribe To Our Free Newsletter |