Update:

Entered Cadsys (India) again.

Earlier exited at 189 due to some cash constraints and now entering at 210 (expensive mistake).

Current Exposure 5.85%.

Cadsys (India)

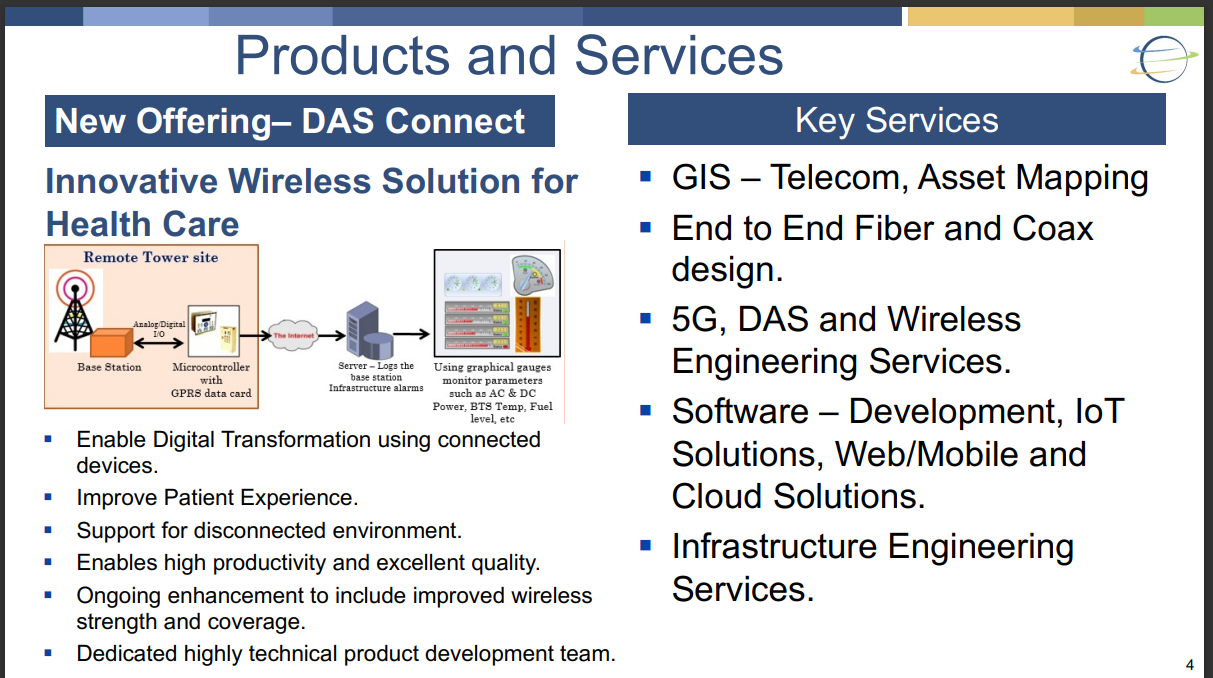

Into GIS and mapping services, Engineering Design services in telecom, Oil & Gas, Electric sectors.

(Company has provided Investor Presentation after every march result till date after listing)

Company listed back in 2017. Company did poorly in 2019-20 and since was loss making on consolidated basis. Posted turnaround result after 3 years.

As per AR company has 63 Million $ orders still pending to complete.

Company started serving orders in its subsidiary a year ago and now has impressive sales with the order book expected to be completed within 2 years.

On consolidated level almost all of their revenues arrive from One subsidiary with 63.5% stake. Apex Advanced Technology LLC. Through this subsidiary they have also acquired Irish Towers LLC. (Good thing is that PE funding arrived for the pending 36%)

Company did a preferential at 50 Rs. per share (a red flag compared to CMP but it arrived when they were loss making).

Company has huge debts (YoY more than doubled, majority of them long term and unsecured from US. Current maturity is only 9% of debt indicating recently acquired debt/moratorium period or 8-10 years tenure loans. With credit situation worsening in USA, not a good sign).

Trade Receivable Ratio is 0.83 vis-a-vis 0.57 a year ago. At the same time 95% of receivables are outstanding for less than 6 months.

Crisil on the contrary has updated the ratings but on standalone basis.

Working capital of the company is very bad in the immediate FY with increase in Trade Receivables and Unbilled Revenues as the main reason.

Promoters holding is 47.7% which is far below the general average of 60% in SMEs. Related party transaction only consists of Remunerations.

All in all Profit and Loss and immediate future outlook is positive but with situation worsening on the balance sheet. I will review it on every half yearly result as there is no indication of migration.

Company’s valuations are expensive at this point because any profit earned is first adjusted in minority interest and then to the parent company, but this dilution is what survived them in the first place.

My initial acquisition, selling and subsequent buying has led my average to the 130s. Though this is a wrongful comparison as initial selling is done and shouldn’t be clubbed but I am willing to give away earlier profits and treat it as a margin of safety. I knew it was a mistake to sell and so bought it as soon as I can.

Note: I don’t have sound knowledge of the field and investing on purely financials basis.

| Subscribe To Our Free Newsletter |