It’s been over two years since this post and I have largely been a silent observer (apologies for that). In the meanwhile, my position size in Ugro has ballooned close to ~20% of my portfolio (~100% gains), which I guessed would be a good time to lay out the pointers behind my increased conviction on Ugro Capital and why I continue to hold.

An inaction is also an action and needs equal amount of hard work, conviction and persistence

First and foremost, the deal breaker – Management Quality. Historically, we have seen various concerns raised around the Religare issue (addressed this couple of years back), high fees paid to Board members (addressed beautifully by Mr.Nath in the annual AGM earlier this year) and some key personnel transitions (CEO,CFO transitions). However, despite these minor events, I believe the management of Ugro Cap has been fairly receptive and addressed most of the queries with valid reasoning.

Additionally, there have been good additions to the team, both to the board via:

-

Tabassum Inamdar (Ex-MD and Co-head of India Research team, Goldman Sachs)

and to the core team via:

-

Om Sharma (Ex-CDO, AU Small Finance Bank , ISB and BCG alum )

I have been a long proponent of the idea that in India, one of the key factors for Financial institution failures has been less to do with the underlying credit risk but more to do with the lack of adequate corporate governance. It was very interesting to see this commentary in the conference call.

Second, the bet on co-lending model and the execution capability has been on-point with a steady growth in off-book AUM

Yes, the risk around seasoning of the loans still exists as nicely articulated in the latest credit report and one needs to keep a close watch on the GNPA/NNPA levels and movement across the buckets, specifically in some of the sub-sectors.

This can be an interesting play, however needs to be monitored. As called out by Mr. Nath in an interview, they are still working on finalizing a few processes before opening the floodgates.

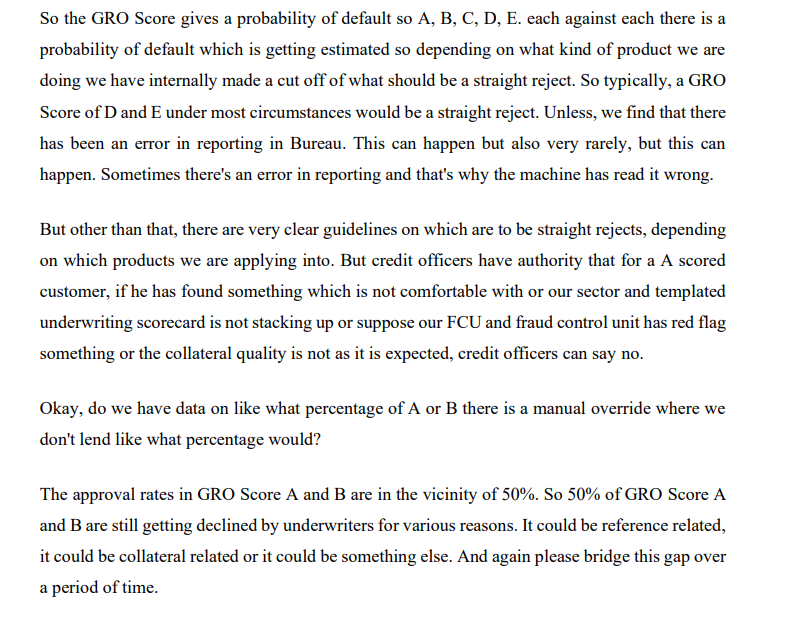

The recent concall also threw interesting light on the Gro Score 3.0 model and the process followed. (thanks @nirvana_laha and @Chins for asking a great set of questions)

Finally, we have seen some publicly-acclaimed investors join in on the journey as well which I guess can be taken as a positive.

Overall, I believe one needs to wait, watch and track the seasoning and impact on asset quality as the cycle turns which will be an interesting exercise in itself.

| Subscribe To Our Free Newsletter |