Been a while since the last update. Been an active few months with a lot of churn. The last month especially has seen a lot of sells as a lot of positions reached the <10% IRR tipping point or where stories played out and incremental risk-returns didnt seem great:

Sells:

-

Ujjivan: Story largely played out. Was contemplating whether I should hold till demerger given there is still a ~15% arbitrage available with the opco. However the SFB is at >2x P/B already and I feel re-rating is behind. We are clearly in the middle of an MFI upcycle. There were also risk management considerations here since I also hold Arman, and between the two MFI had become >25% of the PF at one point. Sale @ ~Rs 485

-

FDC, Indo Count : Reversion to mean stories largely played out with valuation catch up back to normals. FDC Sale Price ~360 & IC ~240

-

Krsnaa Diagnostics: Had sold prior to them losing the Rajasthan contract. Primarily business quality reasons. To some extent the B2G nature of the business is on show. Sale price ~580

-

Trimmed Faze Three above 400 & Chamanlal Setia sold @180: Not sure why I sold Chamanlal in hindsight. Its still so cheap and business is delivering.

Buys:

-

Coastal Corporation: Domestic shrimp industry has been reeling due to both cyclical and structural factors: Cyclical factor is the temporary build up in global inventory leading to massive fall in demand & related inventory price correction. Structural factor is relating to competition from Ecuador which has been making good headway into the USA market. In the meanwhile Coastal has done a good job developing new relationships with Japanese and Korean customers. Furthermore, they are also diversifying the business by adding an ethanol plant. It also seems from trade data that the bottom for shrimp cycle is also behind. In 18-24 months, once the ethanol plant is fully utilized as well, we could be looking at ~70 cr of PAT here and potentially upto a Rs 1000 cr M-Cap from 350 cr today.

-

Rupa/Dollar: largely reversion to mean story. Industry has struggled due to falling RM prices affecting margins and high inventory affecting demand. Historically fair value here should be 2-3x P/S (15-20x EV/EBITDA & 12-15% EBITDA%) and we are at the bottom end of the range. The sales figures are also lower than normal due to a poor demand environment. So there should be decent sales growth as well as P/S rerating in these companies.

-

Punjab Chemicals: Had bought post Q1 results, effectively saw this as a specialty chemical maker trading at commodity valuations. But post some more research have been disappointed with mgmt aggression and execution. Will probably exit and track a bit more.

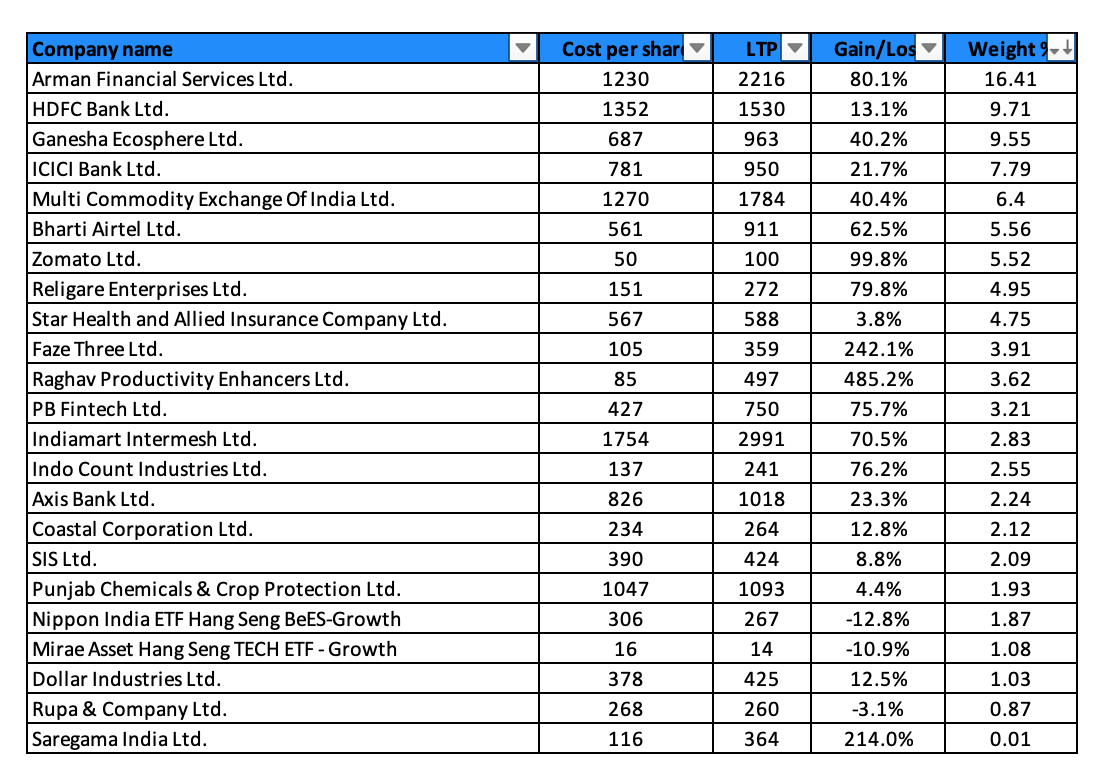

Portfolio now looks as follows:

At this point dont have many incremental deployment opportunities. Studying the chemical sector to see if I can find some opportunities.

| Subscribe To Our Free Newsletter |